The UK runs significant trade deficits with politically important EU countries. Ruth Lea shows that it is hence an important market for the EU’s key exporters and rather than being a supplicant, the UK would, after a vote to leave the union, have a very strong hand of cards to play.

The UK runs significant trade deficits with politically important EU countries. Ruth Lea shows that it is hence an important market for the EU’s key exporters and rather than being a supplicant, the UK would, after a vote to leave the union, have a very strong hand of cards to play.

It is sometimes claimed that UK markets matter comparatively little to other EU Member States because the ratio of their exports (goods and services) to the UK as a % of EU GDP is only around 3% whilst UK exports to the EU accounts for around 12-13% of UK GDP. This factor, so it is said, would weaken the UK’s position in any trade negotiations with the EU after a Brexit vote. The UK would, in effect, be a supplicant if it wished to negotiate a free trade agreement (FTA) with the EU. But this is to ignore the significance of the UK’s sizeable deficits with the EU, in general, and the political significance of EU countries with which the UK runs deficits, in particular.

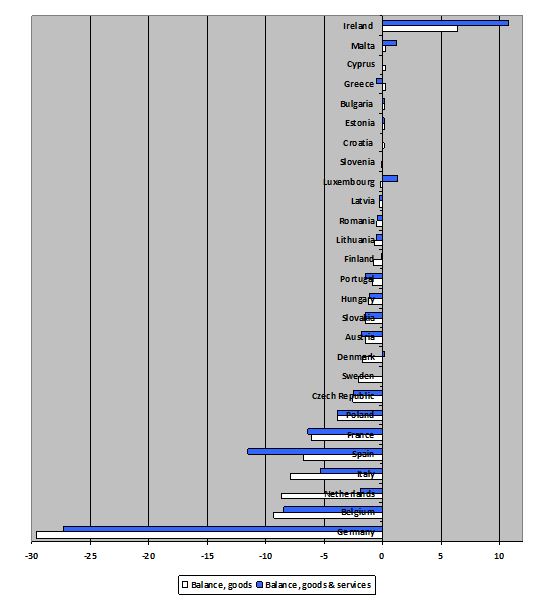

The UK had a goods deficit with the EU of around £80bn in 2014.1 Even allowing for the surplus on services, the deficit on goods and services was around a substantial £60bn. Moreover, the UK had individual deficits with most EU countries (chart 1). Crucially, these countries included Germany (first and foremost), Belgium, the Netherlands, Italy, Spain (especially when services are included) and France.2 (Note, however, that Dutch and Belgian trade data are distorted by the Rotterdam-Antwerp Effect, which exaggerates the importance of the trade flows with these countries.3) The UK’s only EU trading partner with which it had a reasonable surplus was Ireland.

In the case of vote for Brexit, the UK’s new trade arrangement would, of course, have to be agreed by all the other EU Member States. But Germany, as the EU’s hegemon, would almost certainly be highly influential in any negotiations. No German exporter would wish to see any disruption to their lucrative trade with the UK. And, on the reasonable assumption that the German government would support its exporters, it would favour a trade agreement with the UK. Moreover, assuming economic rationality, so would the other key EU Member States as it would also be in their commercial interests. An agreement would surely be successfully negotiated.

So rather than being a supplicant, the UK would, in effect, have a very strong hand of cards to play. And the fact that total EU exports to the UK as a % of EU GDP is relatively modest, or that several EU countries have relatively little trade with the UK, is irrelevant.

Chart 1 UK trade balances in goods and goods & services with EU countries (£bn), 2014

Source: ONS, UK Balance of Payments, Pink Book, 2015 edition, ranked in order of goods trade.

EU exports to the UK are important for EU employment

It is often claimed that 3 million or 4 million jobs in the UK are “dependent on EU membership”. But these figures, whatever their statistical soundness, should, in any case, be described as jobs “associated” with the UK’s exports to the EU, not as jobs dependent on EU membership. The implicit assumption that all UK-EU trade, and associated jobs, would collapse if Brexit is, of course, nonsense.

If we take the ratio of UK exports (goods and services) to the EU as a % of GDP (12.7% in 2014) and multiply by total employment (30.6 million in 2014, see annex table 4) we obtain a figure of around 3.9 million jobs which may be “associated” with EU trade.4,5 It is a very crude calculation and makes the very bold assumption that the pattern of employment in the export industries closely mirrors the pattern of employment in the general economy. This is unlikely to be true. It is likely that exporting businesses are, on average, less labour intensive than in the general economy (they are more weighted to the manufacturing sector) and so fewer than 3.9 million jobs are likely to be genuinely “associated” with the UK’s EU trade.

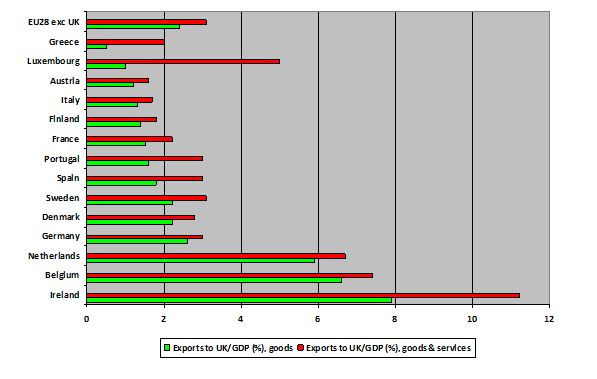

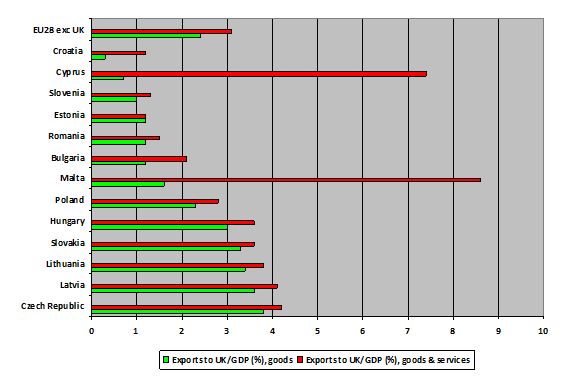

But whatever the “crudity” of the calculations, it is nevertheless a useful exercise because, using the same methodology, direct comparisons can be made between UK jobs associated with EU trade and EU jobs associated with UK trade. In order to analyse the number of EU jobs associated with their exports to the UK, it is first necessary look at the degree of “dependency” of EU countries on their exports with the UK. Charts 2a and 2b show that such “dependency” varies widely. Over 11% of Ireland’s exports went to the UK in 2014, whilst 3% of German exports came here (but a very important 3%). The overall ratio for the EU28 was 3.1% (goods and services).

Chart 2a Exports to UK/GDP (%), goods and goods & services: EU15 (excluding UK) and EU total, 2014

Chart 2b Exports to UK/GDP (%), goods and goods & services: post 2004-EU and EU total, 2014

Source: derived data from (i) ONS, UK Balance of Payments, Pink Book, 2015 edition and (ii) IMF, World Economic Outlook, October 2015 database for the GDP data (converted by the author to sterling).

Chart 3 comprises data for EU jobs associated with UK trade using the crude method of calculation quoted above. As can be seen from the chart the jobs calculated vary hugely between countries, reflecting the wide disparity in trading links with the UK as well as the relative sizes of their economies (and jobs markets). But the overall numbers are substantial. There could be over 1 million German jobs associated with their exports to the UK, over ½ million in France, the Netherlands and Spain and nearly ½ million in Poland. All in all, there could have been a total of 5.8 million jobs in the EU in 2014, on these crude calculations, substantially higher than the number of UK jobs associated with EU exports. Noting the caveat above that exporting sectors are likely to be less labour intensive than for the general economy even if the 5.8 million jobs were reduced by, say, 25% to 4.4 million, the numbers are clearly significant.

Chart 3 EU jobs associated with exports to the UK (1,000s), 2014

Sources: (i) Eurostat database for employment data (resident population concept, LFS), (ii) derived data, using ONS and IMF sources.

Conclusion

In conclusion, it is inconceivable that any EU exporter would wish for any disruption in their trade with the UK on Brexit. And it is almost certain that the key EU governments, not least of all the German government, would act in their economic interests. The UK has a strong hand in any trade negotiations in the interim period between a Brexit vote, the triggering of Article 50 and Brexit itself. Not merely would our major EU trading partners wish for a trade agreement, but they would also be likely to push for such an agreement to be finalised expeditiously, prior to the UK’s departure. It would simply not be in their commercial interests to prolong the negotiations. And, given that the UK would be negotiating as a fully harmonised EU member, this should not be impossible.

The article gives the views of the author, and not the position of BrexitVote, nor of the London School of Economics. Image: Creative Commons Attribution-ShareAlike 3.0

Ruth Lea CBE is Economic Adviser at the Arbuthnot Banking Group.

References

- 2014 is the latest year for which there are country data for goods and services.

- Taken together the EU’s “big 5, excluding the UK” (Germany, France, Italy, Spain and the Netherlands) comprise over 70% of total EU GDP (excluding the UK). Source: IMF, World Economic Outlook, October 2015 database.

- Dutch and Belgian trade are distorted by the Rotterdam-Antwerp Effect reflecting UK exports routed through these ports for other destinations.

- Exports to the EU as % of GDP, taken from ONS sources.

- Employment data taken from Eurostat sources.

{kind=link}

Ruth Lea may well be correct in stating that there will be a strong desire among other European businesses for an expeditious trade agreement with a post-Brexit UK. However, she conveniently ignores two key points.

First, the politics. We will be seeking agreement with 27 other member states, any one of whom may reject the deal which must be reached by unanimity within the European Council, and any one of whom might change their calculus of the value of the trading relationship with the UK. (The deal must also win the approval of European Parliament.)

Second, who is going to negotiate this new trade deal from the UK side, given that we no longer have trade deal negotiating capacity within BIS?

Sir Simon Fraser, former head of the FCO and someone who has been directly involved in a number of trade negotiations at EU level, highlighted the challenge of reaching such highly complex agreements and suggested that anyone who thinks otherwise probably has not had direct experience of conducting them.

I fear Ms Lea is being disingenuous: there may very well be a strong rationale and desire for a swift agreement – but that is another thing entirely from the practicalities of actually achieving it.

Reasonable analysis supports a stronger position for negotiation of trade deals after Bexit. We need to stand our ground defending our own country’s interests and not be intimidated into accepting dictates that put us at a disadvantage.

On the surface a very cogent, seemingly rational explanation of the trade side. It may indeed be right, but personally I don’t think the vote is going to pivot on this point. Broadly, I think the relatively slim majority – but still a majority – of of the UK voting public, particularly the younger generation, is in favour of pan-European cooperation, and indeed greater pan-global cooperation between nations, where this can be beneficial – and attaches more importance and value to this than sovereign independence. The perception seems to be that the world is a better place with people viewing themselves as citizens of the world, not citizens of one nation, randomly allocated based on where their parents gave birth to them. This is particularly so with scurry around the likes of Putin, Trump, and goodness knows which other nationalistic people look like they will have positions of power in years ahead. It may be an LSE blog, but I don’t think this vote will hinge on the economics.

Ruth Lea simply seems to be saying she believes that were we to leave the EU it would be possible to arrive at a workable trading arrangement. In this article she does not say she believes we ought to leave nor does she say that we would have a better trading arrangements outside the EU than in it.