Leaving the European Union with no deal in place for future trading arrangements would be the worst-case Brexit scenario for the UK economy. What’s more, just because GDP growth has not declined since last year’s referendum, it would be wrong to think that Brexit is yet to have any economic effects: it has already lowered UK living standards by causing the value of the pound to decline, which has led to higher inflation and lower real wage growth. These are among the conclusions of a new report from the Centre for Economic Performance (CEP) authored by Swati Dhingra and Thomas Sampson.

In the long run, Brexit is expected to reduce UK living standards through reductions in trade and foreign direct investment, but these effects will take many years to materialise. It is harder to forecast the short-run economic effects of Brexit in the period before the UK leaves the EU. How the economy responds will depend on what businesses and consumers expect to happen in the future and on whether they change their behaviour in advance of Brexit.

In the past year, there has been no obvious effect of the referendum outcome on UK GDP, which has continued to increase at a similar rate to before the vote. Figure 1 shows quarterly real GDP growth since the start of 2015. Growth has averaged 0.47% in the three quarters since the referendum compared to 0.43% in the previous six quarters.

The Brexit vote has increased uncertainty about the future of the UK’s economic relations with the EU. When uncertainty is high, businesses often adopt a wait-and-see approach and delay or cut investment projects and hiring (Baker et al, 2015). Such uncertainty also makes the UK a less attractive investment destination for multinational firms that want to produce and sell in the Single Market.

It is too soon to say whether anticipation of Brexit will cause an investment slowdown. But there is increasing evidence of firms planning to move jobs out of the UK because of Brexit, particularly in the finance industry, where banks such as JPMorgan and Deutsche Bank have already warned that they plan to move staff away from London (Financial Times, 2017).

Figure 1: Quarterly UK GDP growth, 2015 to 2017

Notes: Quarter on quarter growth, seasonally adjusted. Source: ONS.

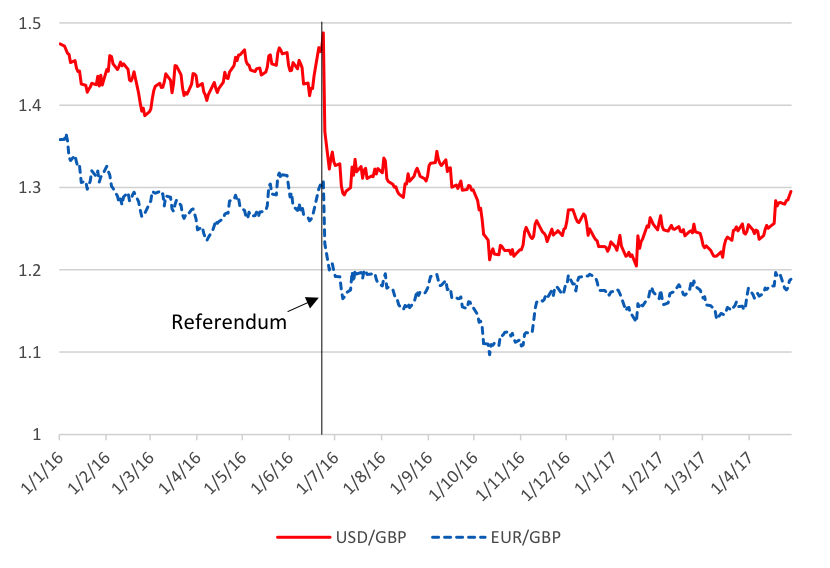

Because GDP growth has not declined since the referendum, it is tempting to conclude that Brexit is yet to have an economic impact. But this would be wrong. Brexit has already lowered UK living standards through its effect on the value of the pound. At the end of April 2017, sterling was 13% lower against the US dollar and 9% lower against the euro than on the day of the referendum (see Figure 2).

The depreciation of sterling is bad news both because of what it tells us and because of its impact on the UK. The depreciation is a signal that investors’ expectations about the UK’s economic performance have deteriorated. Many factors determine exchange rate movements, but one of them is economic growth. Fast growth leads to exchange rate appreciation, while countries that grow slower than the rest of the world see their currency become less valuable. The pound depreciated because markets anticipate that the UK’s future economic growth will be lower than it would have been if the UK remained in the EU.

The effect of the depreciation has been to reduce the UK’s terms of trade – that is, the price of the UK’s exports relative to its imports. The terms of trade are a measure of how much the UK can buy from the rest of the world in return for what it produces. Crucially, a reduction in the terms of trade makes the UK worse off even if GDP is unchanged because it means the UK can afford to buy less in return for its exports.

Consider the following simple example, which illustrates the impact of a reduction in the terms of trade. Suppose the UK only produces apples and that it grows 30 apples per year. UK consumers demand both apples and oranges in equal numbers, so the UK exports apples in order to pay for orange imports. If one apple can be exchanged for one orange, the UK will export half its apples and UK consumers will eat 15 apples and 15 oranges.

Figure 2: Sterling exchange rate, 2016 to 2017

Notes: End of day exchange rates. Source: Bloomberg.

Notes: End of day exchange rates. Source: Bloomberg.

But now suppose the UK’s terms of trade deteriorate so that one apple is only worth half an orange. Then the UK will end up exporting 20 apples to buy only 10 oranges. UK GDP (apple production) has not changed, but because of the terms of trade shock, UK consumers are worse off as they now only eat 10 apples and 10 oranges. To keep consumption constant following this shock, UK production would need to increase to 45 apples per year.

Image by Pete (Flick), licenced under CC BY 2.0

Image by Pete (Flick), licenced under CC BY 2.0

The depreciation of sterling may provide a boost to UK GDP due to increased demand for cheap UK exports. But even if this happens, it is not likely to offset fully the costs from lower terms of trade.

To date, the impact of the depreciation on UK living standards has operated through higher prices. Rising import costs have led to a sharp rise in inflation from 0.5% in June 2016 to 2.7% in April 2017, as shown in Figure 3. Since nominal wages have continued to grow at around 2% per year this has led to dramatic fall in real wage growth. In the year to March 2017, real wages actually declined by 0.5%. (See the CEP Election Analysis on Real Wages and Living Standards for more detailed analysis.) This shows how Brexit has already started to make UK citizens poorer.

This post represents the views of the authors and not those of the Brexit blog. It is an extract from the LSE’s Centre for Economic Performance report Brexit and the UK Economy.

Swati Dhingra is a Lecturer in Economics at the LSE.

Thomas Sampson is an Assistant Professor in Economics at the LSE.

I don’t understand why the the sudden GBP vs EUR immediately after the referendum is so often highlighted. It and the preceding rise seem deviations away from then back to an underlying steady fall starting around December 2015, possibly because the likelihood of a loseable referendum then heightened. That trend has levelled off, albeit rather unstably, since around October 2016.