The pharmaceutical industry is at risk from Brexit. Border delays, R&D disruption and regulatory divergence pose hazards to this important industry, writes Jianwei Xu.

The pharmaceutical industry is at risk from Brexit. Border delays, R&D disruption and regulatory divergence pose hazards to this important industry, writes Jianwei Xu.

Despite numerous debates about the impact of Brexit, the pharmaceutical industry seems to be less eye-catching than other sectors like the manufacturing supply chain and financial services. However, pharmaceuticals are one of the EU’s most important and fastest-growing industries, and they benefit greatly from EU integration.

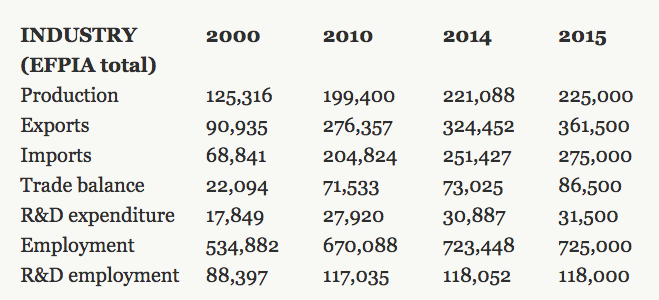

The pharmaceutical sector in the EU has increased from €125 billion to €225 billion over the past 15 years. Employment in the sector also grew dramatically from 535.000 to 725.000. Pharmaceuticals have also become very advantageous for the EU. Exports of pharmacy products have more than tripled over the past 15 years, with most of these gains obtained from extra-EU transactions. This is also the third largest industry in the UK, contributing 10 per cent of the country’s GDP, with an employment of 73.000 people and a trade surplus of €3.3 billion.

Table 1. The rapid growth of the European pharmaceutical industry

Source: “The pharmaceutical industry in figures”, 2016, European federation of pharmaceutical industries and associations.

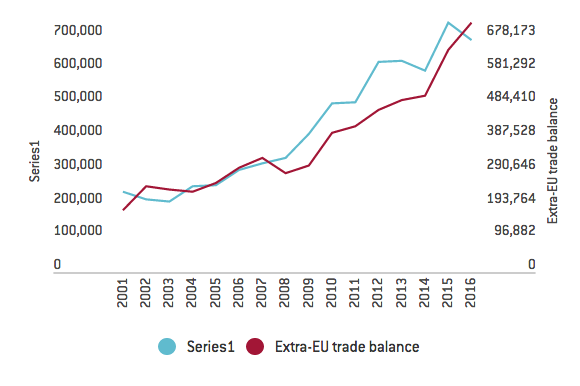

Figure 1. Trade balance for the pharmaceutical industry (unit: €million)

Source: data collected from tradesmap.org for HS30 “Pharmaceutical products”

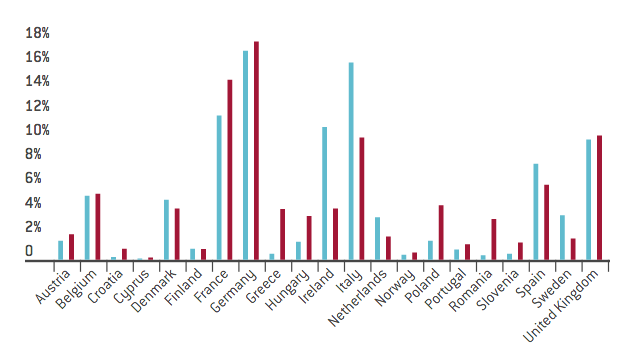

The rapid advance of the pharmaceutical sector over the past decade can be closely associated with the integration of the EU trade chain. In 2016, around 67 per cent of the EU’s exports of its products were intra-EU exports; 52 per cent of the EU’s imports of its products were intra-EU imports. According to EFPIA figures, among the EU member states the UK is undoubtedly a key player, constituting 10 per cent of the EU’s total production and employment. Moreover, the UK runs a trade deficit of €114 billion against the other EU27 countries, implying that it is a major destination for EU pharmaceutical products.

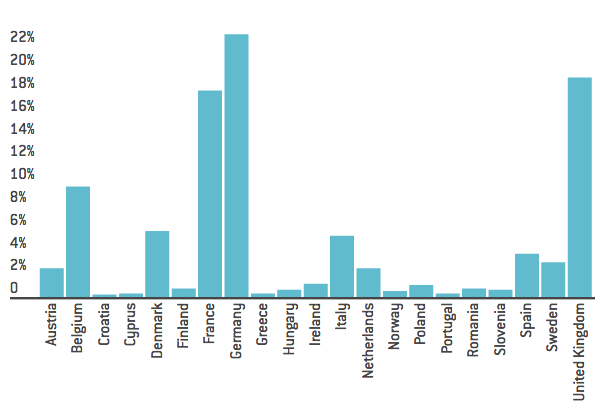

Figure 2. Development of the pharmaceutical sector across EU member states

Source: “The pharmaceutical industry in figures”, 2016, European Federation of Pharmaceutical Industries and Associations.

Non-tariff barriers such as the possible establishment of physical border could have negative effects on pharmaceutical trade

Fortunately, the EU has long adopted zero most-favored-nation tariffs even for international extra-EU transactions for pharmaceutical products. So the worst scenario, even in a hard Brexit where the EU and UK treat each other in the WTO multilateral framework manner, would not add a specific tariff burden on pharmaceutical trade.

However, tariffs are not the only barrier to trade. There is also a possibility that other types of non-tariff barriers could be created to hamper pharmaceutical trade. In particular, with the strengthening of immigration control, border checks might be resumed which could create delays in transferring pharmaceutical products to/from the UK. Longer lead times and increased paperwork caused by these customs bottlenecks could affect service levels and margins – especially for pharmaceutical products, which have a short shelf life. Evidence has shown that, for time-sensitive industries, every 1 hour of customs delay adds 0.8 percentage points to the ad valorem trade-cost rate and leads to 5 per cent less trade. This means that perishable pharmaceutical products are likely to cost more for UK residents, especially in the case of emergency.

The establishment of a physical border also matters particularly for Ireland. Ireland is the only country that shares a land border with the UK. Although it is hard to say what will eventually happen in the event of Brexit until the final post-Brexit model is determined, the risk has been mounting since Theresa May’s report signaling a hard Brexit. Establishing an Irish-Irish border would mean that Irish pharmaceutical products need to go across the UK border twice before entering the rest of the EU. One solution to avoid this additional processing cost is to construct a common border for two countries, which was already the case for passengers from 16 countries such as China and India to enter the region. But that undoubtedly means additional costs for Irish pharmaceutical consumers.

Disruption of research and development (R&D) activities

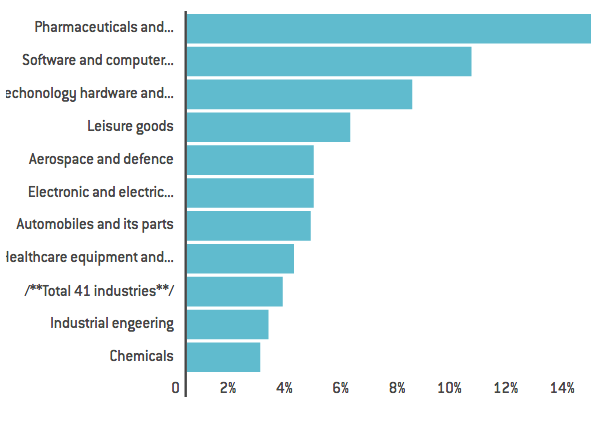

One of the key characteristics of the pharmaceutical industry is its high intensity in research and development. Figure 3 shows that the pharmaceutical and biotechnology sector accounts for the highest R&D intensity in the EU, even higher than the software and computer services sector. Eurostat data also indicates that the pharmaceutical industry has the highest added-value per person employed.

Figure 3. Comparisons of R&D intensity across sectors

Source: The 2015 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG RTD

Within the pharmaceutical industry, the UK has long been a centre for research and development (R&D) activities. In 2015, it contributed approximately 20 per cent of the EU’s total R&D, only slightly lower than Germany and France. As Maria Demertzis and Enrico Nano highlight, these research and development activities rely on two key factors: skilled labour supply and research funding. Both factors could be at risk in the post-Brexit era. For the former, the UK has attracted a large number of skilled workers from abroad, most of which are EU citizens. For the latter, the UK gains more research funding in the current system than any other country. Therefore, Brexit could undoubtedly have a negative impact for both factors in the pharmacy industry.

Figure 4: R&D contributions in pharmacy industry

Source: “The Pharmaceutical Industry in Figures”, 2016, European Federation of Pharmaceutical Industries and Associations

In addition, research and development in the pharmaceutical industry rely on protections on trademarks and associated rights, which are currently covered by EU laws. The future of these activities after Brexit depends on the intellectual protection coordination arrangement between the EU and UK. The further the arrangement goes away from the current system, the more challenging the future will be.

Regulatory segmentation

The unification of the regulatory framework on product standards has eased entry barriers for pharmaceutical companies in the EU. For example, the current product standard in the European Economic Area (EEA) is authorised by the London-based European Medicines Agency (EMA), meaning that all drugs approved by EMA are automatically granted access to the UK’s market. If the UK’s post-Brexit relationship with the EU does not include a shared regulatory framework, access to both markets would be subject to additional process. Any disruption is likely to lead to a geographic reallocation of the pharmaceutical industry. This can be detrimental for the UK but could be an opportunity for substitutive countries taking on this business.

The EMA being in London is also the reason why a number of influential pharmacy companies choose to locate their European headquarters in the UK. Ironically, even the European Medicine Agency (EMA) may find itself in an awkward situation after Brexit, because it is currently located in Canary Wharf, London. It is highly unlikely that the UK can keep the medical authority, and the long-term benefits to the UK from proximity to the EMA will also be lost.

Conclusions

The impact of Brexit on the European and British pharmaceutical industry will go far beyond the simple trade analysis based on tariffs but to more non-tariff aspects. The establishment of a physical border will cause delay in transportation not only for the UK but also Ireland. This may increase the cost of pharmaceutical products especially those with short expiration date.

Moreover, a UK outside of the EU might find it difficult to attract skilled experts for the industry, lose research funding supported by the EU, and face barriers accessing the EU27 market. For the rest of the EU, Brexit could also cause similar additional costs on the whole, but given its larger economic size than the UK, the loss would also be smaller. For some EU countries, if they can seize the opportunity to take on UK business, or become the new location for the EMA, there is a chance to benefit despite the general loss in the EU.

Nonetheless, the best strategy to reserve benefits for both the EU and UK is still to maintain the existing relationship between the two parties on all the related aspects. But this seems to be an increasingly challenging task in the likely scenario of a hard Brexit.

This blog post was originally published by Bruegel and LSE Business Review. The post gives the views of its author, not the position of LSE Brexit or the London School of Economics. Featured image credit: Lab, by jdn2001cn0, under a CC0 licence.

Jianwei Xu is a visiting scholar at Bruegel. He is an associate professor at Beijing Normal University, and also works as an affiliate fellow at China Academy of Social Science and a youth member of the China Finance Forum 40.

2 Comments