The exceptional economic success of many European countries in the post-war period was characterised by the dominant presence of family firms across the continent. In countries like Germany and Italy, family ownership came to be seen as the best guarantee of economic and social development. But the consensus that family firms are good for growth has come under scrutiny in recent years.

Indeed, an emerging body of evidence indicates that family management may actually be detrimental for performance. One study estimates a 4% profitability loss for Danish firms due to having a family manager rather than a professional manager. Another finds that family firms have worse executive selection because they prefer to hire a less qualified family manager rather than an external professional manager: this accounts for a 6% productivity loss for family CEO firms relative to firms owned by dispersed shareholders.

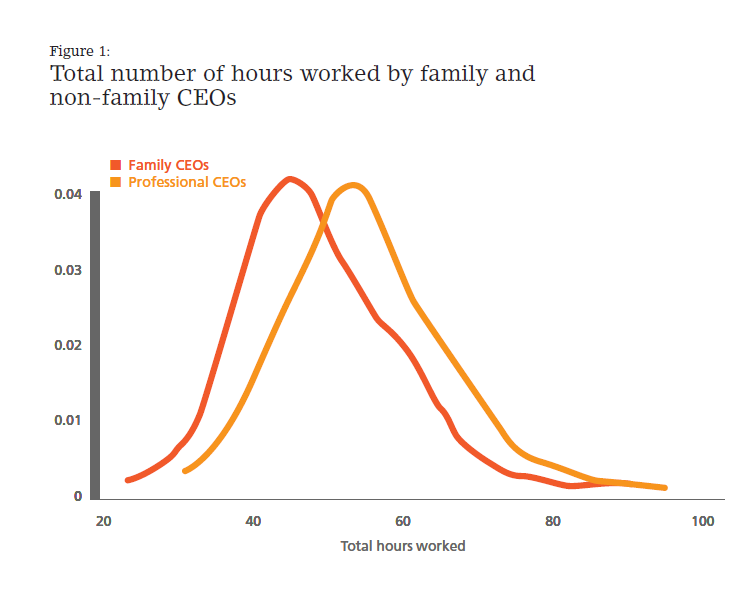

We conducted a time-use analysis of around 1,100 CEOs in six developed and developing economies: Brazil, France, Germany, India, the UK and the US.

So what does economic theory say about whether firms should be led by their owners or by professional managers? The argument in favour of owners is that they have more ‘skin in the game’: as the residual claimants of income generated by the business, they should be highly motivated to succeed, other things being equal. The argument against is that other things are not equal. In particular, owners are typically wealthier because they own the firm, and might therefore demand or reward themselves more leisure than professional managers.

Given the ubiquity of family firms, understanding which of these effects prevails has important implications for aggregate income and growth. Our research investigated this issue by conducting a time-use analysis of around 1,100 chief executive officers (CEOs) in six developed and developing economies: Brazil, France, Germany, India, the UK and the United States. We found that family CEOs dedicate systematically fewer hours to work activities compared with professional CEOs (Figure 1). The difference – at least 9% of total hours worked – is due to two factors: family CEOs start work later in the day; and they are more likely to interrupt their day to devote time to personal activities.

Our results suggest that the fewer hours of work put in by family CEOs are consistent with the presence of differences in their taste for leisure versus work, rather than by systematic ‘technological’ differences between family- and non-family-owned firms. This conclusion is supported by two sets of findings.

First, observable differences in the characteristics of individuals and organisations explain very little of the difference in hours worked between family and professional CEOs. For example, it might be argued that the former can afford to work fewer hours because they can delegate their responsibilities to other family members more easily. But differences in the number of family members in management explain only a small part of the difference in hours worked. What’s more, professional CEOs in family-owned firms work just as hard as their colleagues in non-family-owned organisations, which rules out any suggestion that family firms simply require less work.

Second, we show that the difference between family and professional CEOs depends on the ‘opportunity cost’ of leisure. For example, family CEOs working in larger firms and more competitive industries – where the opportunity cost of CEO leisure is higher because slacking off would presumably have serious negative implications for the firm – work as many hours as professional managers.

Symmetrically, family CEOs respond more strongly to exogenous ‘shocks’ that increase the marginal cost of their work effort. For instance, in India, we use two proxies for shocks: extreme monsoon rainfall and the broadcasting of Indian Premier League (IPL) cricket matches. During the monsoon season, severe rains and floods often cause traffic jams and make it particularly costly to go to work; while the IPL is a popular sporting event that draws superstar players and the eyes of an enthusiastic nation. The difference in hours worked between family and professional CEOs is significantly larger on days when torrential rains hit the region in which the CEO is located. It is also larger on days when IPL matches are broadcast.

Family CEOs seem to value leisure more than professional managers.

The fact that family CEOs seem to value leisure more than professional managers is consistent with the idea that the former are typically wealthier. The difference between family and professional CEOs is larger in countries where more permissive hereditary laws favour a concentration of wealth in the hands of the individuals due to inherit control of the family business. But the difference between family and professional managers is unaffected by other country characteristics, such as the level of development, rule of law and trust, which may inhibit firms’ ability to nominate a non-family manager.

Longer hours worked by CEOs correlate strongly with firm performance, across a wide range of metrics: productivity, profitability and sales growth. This implies that systematic differences in hours worked between family and non-family CEOs may well have large economic implications (though unfortunately, the nature of our analysis does not allow us to estimate the causal effect of CEO hours worked on performance). For example, the difference in hours worked corresponds to a 2.6% productivity difference between family and professional CEOs. Given the ubiquity of family-run firms, differences in CEO hours worked may add up to a lot – in reduced profits, slower growth and lagging wages, all of which flow into the wider economy.

This blog post is a shorter version of the article published in Centrepiece, the magazine of LSE’s Centre for Economic Performance (CEP).

Oriana Bandiera is a Professor of Economics at the LSE and the Director of STICERD. She is a member of IZA, CEPR, BREAD, EUDN and JPAL-Europe. Her primary research interests are in labour economics, development economics, and the economics of organisations. In 2007 she was jointly awarded the IZA Young Labor Economist Prize. She is an editor of the BE Journal of Economic Analysis and Policy and is on the board of the Journal of Economic Literature.

Oriana Bandiera is a Professor of Economics at the LSE and the Director of STICERD. She is a member of IZA, CEPR, BREAD, EUDN and JPAL-Europe. Her primary research interests are in labour economics, development economics, and the economics of organisations. In 2007 she was jointly awarded the IZA Young Labor Economist Prize. She is an editor of the BE Journal of Economic Analysis and Policy and is on the board of the Journal of Economic Literature.

Andrea Prat is the Richard Paul Richman Professor of Business at Columbia Business School and Professor of Economics at the Department of Economics, Columbia University. After receiving his PhD in Economics from Stanford University in 1997, he taught at Tilburg University and the London School of Economics. Professor Prat’s work focuses on organizational economics and political economy. His current research explores – through theoretical modelling, field experiments, and data analysis – issues related to incentive provision, firm structure, and communication modes. Professor Prat is a principal investigator of the Executive Time Use Project.

Andrea Prat is the Richard Paul Richman Professor of Business at Columbia Business School and Professor of Economics at the Department of Economics, Columbia University. After receiving his PhD in Economics from Stanford University in 1997, he taught at Tilburg University and the London School of Economics. Professor Prat’s work focuses on organizational economics and political economy. His current research explores – through theoretical modelling, field experiments, and data analysis – issues related to incentive provision, firm structure, and communication modes. Professor Prat is a principal investigator of the Executive Time Use Project.

Raffaella Sadun is the Thomas S. Murphy Associate Professor of Business Administration in the Strategy Unit at Harvard Business School and a research associate in CEP’s productivity and innovation programme. Professor Sadun’s research focuses on the economics of productivity, management and organizational change. Her research documents the economic and cultural determinants of managerial choices, as well as their implications for organizational performance in both the private and public sector, including healthcare and education. She is among the founders of the World Management Survey and the Executive Time Use Project. She tweets at @raffasadun