The global economy has witnessed the emergence of a new set of key actors over the last two decades. Sovereign wealth funds (SWFs) and pension funds (PFs) – or sovereign investors – have become pivotal players in global financial markets thanks to their liquidity, and continue to grow rapidly in number and in size. This group of highly heterogeneous state-owned funds has different backgrounds, structures, and missions, but shares an ultimate goal: to preserve capital and maximize the return on investments.

Most of the wealth sitting on the books of these investors has its origins in countries’ public budgetary surpluses fuelled by commodities exports, foreign exchange reserves, or pension contributions. The location of the fund is therefore not necessarily correlated with the GDP or purchasing power of its country in the global context. In fact, the majority of these players are located in the so-called emerging markets. Currently, 70 percent of the funds in terms of both number and size are headquartered in the Middle East, North Africa, and Asia-Pacific regions. This is unlikely to change in the near future, as most governments having conversations to set up new investment vehicles are from Africa and Latin America.

Sovereign investors have generated an unprecedented flow of capital from emerging economies to developed markets and subsequently heated up numerous policy debates in Europe. On the one hand, some of these funds come from non-democratic states and the recipient countries may consider the inward investment an issue of national security if there are objectives beyond the economic and financial goals. On the other hand, it is argued that the presumption of innocence should apply, and that these equity investments are just an issue of economic governance, which, if well managed, can ultimately be beneficial to Western countries.

Since the start of the decline of oil prices in June 2014, analysts and journalists alike have been asking the same question: what is going to happen to sovereign wealth and investment funds? There is no doubt that for some of the crude-rich states, low oil prices will translate into a lack of budgetary surplus to be transferred to their investment vehicles, but this is unlikely to be a game changer in the short term. Most sovereign investors have accumulated large stocks of capital on their balance sheets that still need to be deployed, and they will keep investing in opportunities in all asset classes.

There are, however, a number of other challenges that may condition the strategy of these investors going forward:

- Achieving superior returns in an environment of low interest rates and a “new normal”: asset allocation is moving towards alternative options — including real estate, infrastructure, and private equities — and most funds are now trying to rely less on external asset managers and have started to act on their own in seeking alpha (earning a return in excess of the benchmark index, while maintaining a similar risk profile). That delivers a great deal of implications and challenges.

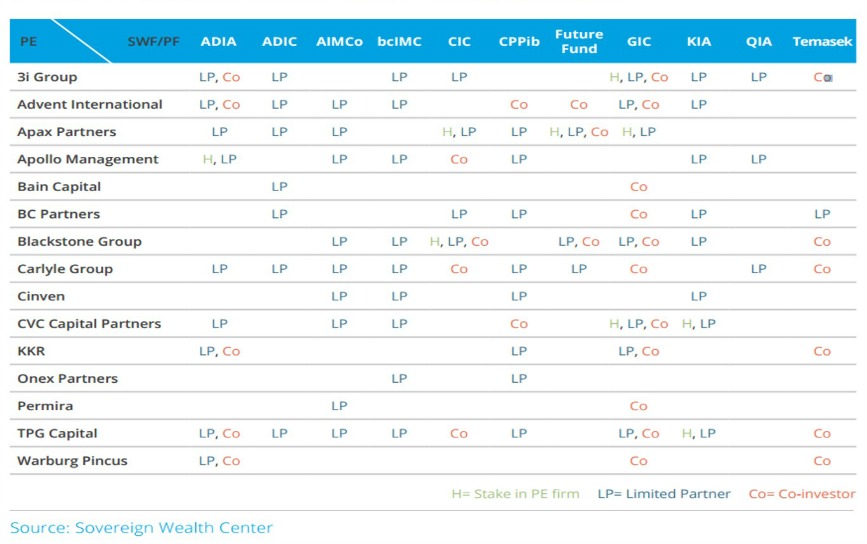

Table 1: Sovereign Investors and Private Equity Funds Matrix. The relationship matrix between sovereign investors and private equities is growing in size and complexity. A sample of these interactions is included in the table.

- Lack of familiarity with new investment grounds: competition for prime assets is fierce and funds have no choice but to start looking at new options, such as emerging markets and greenfield investments — associated to assets yet to be constructed, and that are usually not yet generating any cash flow or return to the investors. These are new grounds for them that may require revisiting the risk-return profile.

- Corporate governance, transparency, and commitment to open markets: sovereign investors have come a long way with steps like the Santiago Principles and they should make sure to continue down this path, especially when markets recover and the need for selling assets becomes less pressing in developed economies.

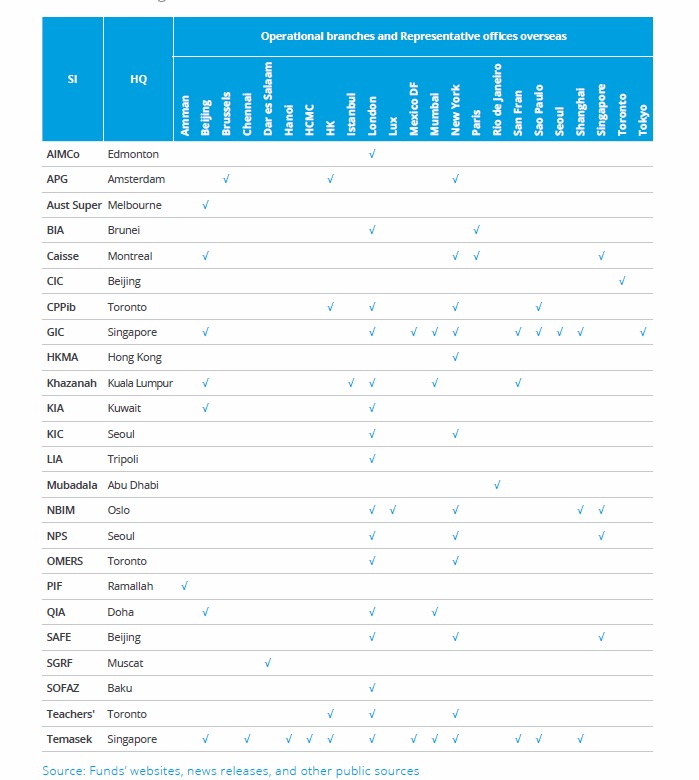

- Talent attraction and retention: human capital is crucial for investment businesses and sovereign investors, especially when they are transitioning into a model with fewer external asset managers and more in-house experts. Offices overseas at international financial centres or generous packages may be their only competitive advantage when financial markets pick up again.

Table 2: Sovereign investors’ offices overseas

For Europe, it is important to understand the role of these new players in the global economy. Policymakers have placed a lot of attention on their investment strategy or focus, i.e. where and especially why they are going to invest next. But fundamentally, sovereign wealth funds are a highly heterogeneous group of institutional investors, and no two funds are the same. While corporate governance and transparency are treated as the main issues, a step back must be taken to fully appreciate the funds’ mission, vision and values.

♣♣♣

Notes:

- This article is based on the author’s The Major Role of Sovereign Investors in the Global Economy: A European Perspective, part of the book The Global Context: How Politics, Investment, and Institutions Impact European Businesses, edited by Javier Solana and Angel Saz-Carranza.

- The post gives the views of the author, and not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Doha skyline by Francisco Anzola CC-BY-2.0

Diego López is an expert in sovereign wealth funds and the Director of PwC’s Global SWF Team. He is based in Abu Dhabi and works closely with most Middle Eastern SWFs. Diego is a fellow of Tufts University – SovereigNet and Bocconi University – Sovereign Investment Lab, as well as a prominent alumnus of the London School of Economics (LSE), where he serves as President of the UAE group and Ambassador to the Middle East. The author bears full and sole responsibility for any views expressed, errors and omissions, of which he would be grateful to be informed at dlopez@alumni.lse.ac.uk

Diego López is an expert in sovereign wealth funds and the Director of PwC’s Global SWF Team. He is based in Abu Dhabi and works closely with most Middle Eastern SWFs. Diego is a fellow of Tufts University – SovereigNet and Bocconi University – Sovereign Investment Lab, as well as a prominent alumnus of the London School of Economics (LSE), where he serves as President of the UAE group and Ambassador to the Middle East. The author bears full and sole responsibility for any views expressed, errors and omissions, of which he would be grateful to be informed at dlopez@alumni.lse.ac.uk