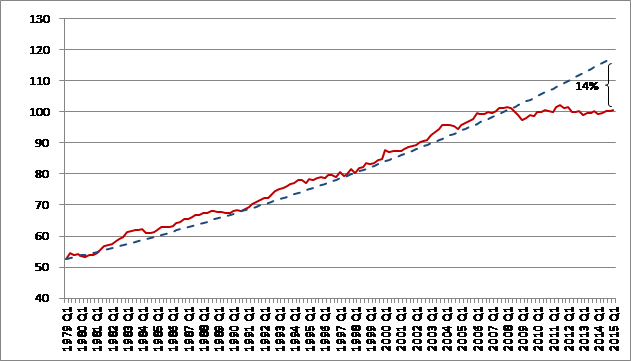

Productivity growth is the only way to achieve sustainable improvements in living standards. Yet since the financial crisis in 2008, UK productivity growth has been stagnant. We are now 14 percent below the level that would have been achieved if pre-crisis trends had continued (Figure 1).

Figure 1: UK productivity growth – GDP per hour worked

Source: Whole Economy GDP per hour worked, seasonally adjusted. ONS Statistical bulletin, Labour Productivity, Q1 2015, Date of publication 1 July 2015. (Q2 2010=100). Note: predicted value after Q2 2008 is the dashed line calculated assuming a historical average growth rate of 2.2%.

Understanding this poor performance since the financial crisis has been labelled the “productivity puzzle” because so far economists have not been able to fully explain it. It is generally agreed that a combination of demand and supply side forces are at work, which implies that some growth should return as demand picks up, but that there are other structural issues such as reduced investment or capital misallocation which could have more permanent effects.

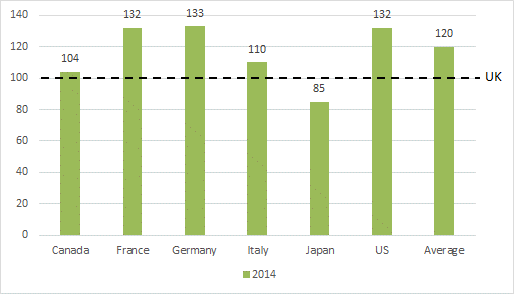

The productivity puzzle has exacerbated our long-standing gap with our main international peers. The latest data show that we are 20 percentage points below the other G7 countries, and over 30 percentage points behind our main peers (France, Germany and the US) in terms of output per hour. This persistent gap has been driven by chronic under-investment, particularly in skills, infrastructure and innovation, as set out in the LSE Growth Commission.

Figure 2: International Comparison of Productivity (UK=100)

Source: International Comparisons of Productivity – First Estimates 2014, ONS. Table 1, Current price GDP per hour worked. UK=100. Date of publication 18 September 2015.

There is much that government can do to address supply-side bottlenecks that hold back growth. In the run up to the 2015 general election, the productivity challenge was largely ignored in economic debate – mainly for political reasons. Since May, however, attention has rightly been focused on the issue. The government launched a productivity taskforce which published its Productivity Plan (the “Plan”) in July which was followed by a BIS inquiry. More recently, the government announced the creation of a new National Infrastructure Commission (NIC), an independent body that will seek to develop a long-term infrastructure strategy for the UK.

The Plan provides a good starting point for thinking about the challenge and sets out numerous policies to boost growth. However, given the scale of the challenge, much more needs to be done. Here, I outline some issues in skills, infrastructure and innovation and some ways they can be addressed.

Skills

The UK’s performance on higher education has improved over recent decades, but skills shortages are widely reported by business.

A long-standing issue is the “long tail” of inadequately educated young people emerging into the world of work. As recognised in the Plan, we need more focus on raising the basic skills of school-leavers, and developing a coherent post-16 technical education offer, with the brand and clarity of A-levels, consisting of both general and specific skills. The apprenticeship levy announced in the Plan is an effective way to get firms to contribute to the costs of vocational training, it is important that the money raised is spent effectively and that it is not only the large firms that benefit.

We need to ensure that young people from all backgrounds are able to meet their full productive potential. The Plan announced the conversion of university maintenance grants to loans. This is a regressive policy since it implies that poorer students will graduate with more debt and there is evidence to suggest it could harm university admissions from this group.

The role of international talent cannot be ignored when addressing skills shortages – particularly in STEM subjects. Our high quality universities attract top students from around the world. But obstacles in visa requirements and how they are administered prevent them from contributing to our economy.

Infrastructure (long term policy, lower cost of capital)

There are persistent inadequacies in UK infrastructure and large-scale investments are required in all areas. Key problems include high levels of policy instability, difficulties making informed decisions based on sound evaluation, and problems overcoming opposition to development. High levels of policy risk have also led to a high cost of capital and problems raising finance from the private sector.

The announcement of the infrastructure commission presents an excellent opportunity to achieve a more consensual and long-term strategy, rising above the pressures of the political cycle. Given the interconnectedness of different types of infrastructure, it is important that the NIC bases its evaluations on system-wide analysis – involving key stakeholders in the development of ideas. There should also be more focus on creative mechanisms to share the gains of development with those who stand to lose. A long term framework and reduced uncertainty around the direction of policy should help lower the cost of capital, implying easier access to finance with less need for costly government guarantees. There is also a potential role for a “national infrastructure bank” to help “crowd in” private sector investment.

Innovation

Innovation is a crucial ingredient for productivity growth, yet our investment in R&D, both public and private, is lower than that of our main international peers. Moreover, government spending on R&D (the science budget) has been falling in real terms. This is a concern because research has shown that public R&D “spills over” to the private sector, and leverages in further private sector investment.

For the private sector, difficulties financing innovation have been a key obstacle. The Plan outlines further measures to increase competition in the banking sector, and highlights the importance of long-termism in investment horizons, but there is more that could be done in this area (particularly in corporate governance). Policies to promote the collateralisation of intangible assets would help small innovative firms to access finance.

Conclusion

The government is focusing on the right area: how to get productivity growing again. While there are currently many individually sensible policies, there are areas where more needs to be done, and it must all be woven into a clear growth strategy. Without such a vision, it is likely that shorter term considerations will come to dominate, especially as the Parliamentary term wears on.

♣♣♣

Notes:

- This post gives the views of the author, and not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Gavin Houtheusen/Department for International Development CC-BY-2.0

Anna Valero is an Economics PhD candidate at the LSE, and Research Economist at the Centre for Economic Performance, on the growth programme. Her work is focused on firm organisation and workforce skills, and their effects on productivity and innovation. More generally, Anna is interested in understanding UK economic performance, the drivers of growth and implications for policy. Before resuming her studies, Anna was at Deloitte for a number of years where she was a Manager in the Economic Consulting practice and qualified as a Chartered Accountant.

Anna Valero is an Economics PhD candidate at the LSE, and Research Economist at the Centre for Economic Performance, on the growth programme. Her work is focused on firm organisation and workforce skills, and their effects on productivity and innovation. More generally, Anna is interested in understanding UK economic performance, the drivers of growth and implications for policy. Before resuming her studies, Anna was at Deloitte for a number of years where she was a Manager in the Economic Consulting practice and qualified as a Chartered Accountant.