As the banking crisis of 2008 erupted, policymakers and economists alike asked: How different is this crisis from previous ones? The United States — perhaps the epicenter of the 2008 crisis — had not been afflicted with a major banking crisis since the Great Depression of the 1930’s, rendering the post-crisis outlook particularly uncertain.

Yet, prior to the 1930’s, banking panics were common in US history. As such, the pre-Depression era may serve as a valuable laboratory to better understand the effects of banking disturbances on the US economy. Moreover, while comparisons between the financial panics of the Great Depression and the 2008 crisis were widespread at the time the crisis erupted, comparisons with these earlier panics were much more muted.

In new research, I investigate the macroeconomic effects of the major banking panics of the pre-Great Depression era. In the process, I shed new light on a series of questions: By how much does national output fall in the aftermath of major banking panics? Are recessions with major banking panics more severe than recessions without them? Are recoveries following major banking panics fast and robust or are they more likely to be protracted and slow? More generally, what are the effects of banking panics on the macroeconomy? I find that such downturns with major banking panics are linked to large and longer declines in output, which in turn lead to slower growth during the subsequent recovery.

To begin, because prior panic series — lists of panics — present contradictory accounts of when and where banking panics occurred, I needed to carefully recreate a detailed history of banking panics in the United States. To do this, I systematically searched through more than 100 years of historical financial newspapers by reading newspaper articles that reported bank failures, suspensions and runs. Then, using a set of criteria that grouped clusters of bank runs, suspensions and failures as distinct banking panics, I reconstructed a detailed account of when and where banking panics occurred from 1825 to 1929 — that is, in the century before the Great Depression.

My new panic series identifies seven major banking panics that were nationwide in scope — 1833, 1837, 1839, 1857, 1873, 1893, and 1907 — along with many other regional, more localized banking panics. The new series reveals several interesting historical trends: Major banking panics coincided with large declines in stock prices, occurred at a rate of roughly one every 14 to 20 years (except for an elevated rate in the 1830s), and were more likely to occur during the fall and spring, those seasons characterized by stringent monetary conditions due to heightened demand for money and credit from the agricultural sector.

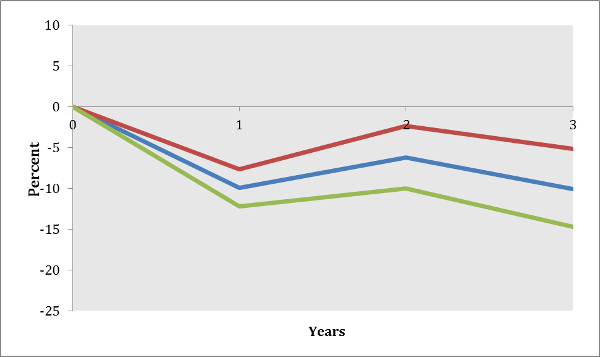

Most notably, the new series allows me to conduct statistical tests to determine how macroeconomic variables such as output and the price level behave in the aftermath of major banking panics. The evidence indicates that major banking panics have a causal and strongly negative effect on both output and prices. According to my baseline results, which are based on yearly industrial production data — the most reliable national output series that spans the pre-WWI US economy, the estimated effect of a major banking panic on output is a decline of 10 percent in the year following the panic, as shown in Figure 1.

Figure 1 – The Impact of a Banking Panic on Output

Note: Estimated impact shown in blue , along with the upper (red) and lower (green) standard error bands

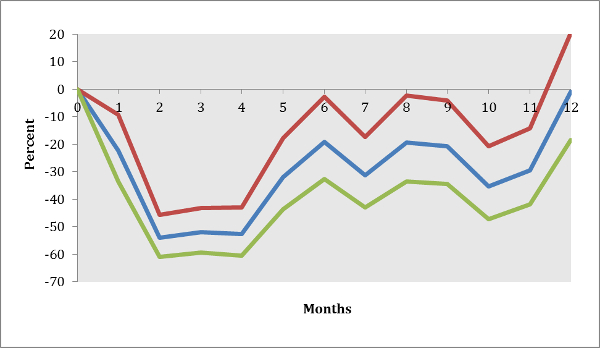

Furthermore, monthly construction data show that output falls rapidly, plummeting in the immediate months after the outbreak of the crisis (Figure 2).

Figure 2- The Impact of a Banking Panic on Construction

Note: Estimated impact shown in blue , along with the upper (red) and lower (green) standard error bands

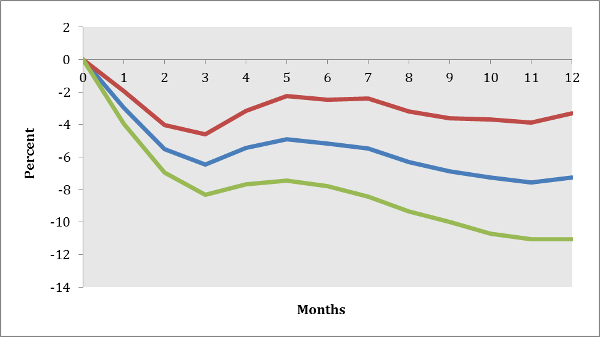

Prices also fall quickly as Figure 3 shows, declining by roughly 7 percent over the course of a year.

Figure 3 – The Impact of a Banking Panic on the Price Level

Note: Estimated impact shown in blue , along with the upper (red) and lower (green) standard error bands

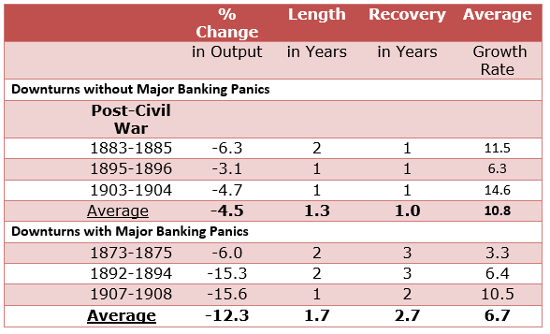

In addition, equipped with a reliable listing of when banking panics occurred, I am able to examine how downturns with major banking panics differed from downturns without them. Table 1 presents the six recessions that occurred between the Civil War and World War I. For each recession, the chart reports four key macroeconomic indicators: the percentage decline in output from peak to trough, the length of the recession in years (the length of time from peak to trough), the length of the recovery in years (the length of time output took to return to its pre-recession peak), and the average annual growth rate of output during the years of recovery.

Table 1- Recessions with and without Major Banking Panics

Note: Output is measured using the Davix Index of Industrial Production. Source: Davis (2004, 2006)

The chart reveals a number of key findings. First, downturns with major banking panics are associated with dramatically larger declines in output (12.3 versus 4.7 percent). Second, downturns with major banking panics were longer than downturns without them, on average (1.7 years versus 1.3 years). Third, recoveries were longer for downturns with major banking panics (2.7 years versus 1 year). Fourth, output growth was slower during recoveries for downturns with major banking panics (6.7 versus 10.8 percent).

Together, these results indicate that banking panics were a major source of economic instability in the century before the Great Depression. Banking panics caused dramatic declines in output and were followed by comparatively slow recoveries. Also, recessions with major banking panics were more severe, on average, than recessions without them. Thus, the behavior of the US macroeconomy during the recent banking crisis — a peak-to-trough decline in output that exceeded all other postwar US recessions, followed by a sluggish recovery — appears to parallel the experience of the US macroeconomy during the major banking panics of the 19th and early 20th centuries.

♣♣♣

Notes:

- This article was originally published in the LSE USAPP blog and is based on the author’s paper A New History of Banking Panics in the United States, 1825-1929: Construction and Implications in the American Economic Journal: Macroeconomics.

- This post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image: pingnews.com, under a CC-BY-SA-2.0 licence

Andrew Jalil is Assistant Professor of Economics at Occidental College, California. His research focuses on the causes and effects of financial crises, macroeconomic policy during the Great Depression, and the effects of monetary and fiscal policy.

Andrew Jalil is Assistant Professor of Economics at Occidental College, California. His research focuses on the causes and effects of financial crises, macroeconomic policy during the Great Depression, and the effects of monetary and fiscal policy.