It is well known that the release of new information about a firm affects its stock price, as investors update their expectations about the firm’s fundamentals and future profitability. For example, unexpectedly good earnings news cause price increases, while negative surprises cause drops in prices. However, little is known about the impact of news on the co-variance structure of stock returns. Do information flows affect the way in which a stock’s returns co-move with the returns of other firms? And why would this matter?

The degree to which the returns of a given stock co-vary with the returns of the rest of the market gives us a measure of the stock’s systematic, undiversifiable risk. This risk is typically measured by beta (the co-variance between the stock’s returns and the market returns, scaled by the variance of market returns). While there is a lot of evidence on low-frequency variations in betas associated with the business cycle, so far we have not been able to estimate higher-frequency betas for individual stocks, due to the lack of reliable data and of suitable econometric techniques.

Yet detecting variations in individual betas at higher frequencies, and in particular during the release of new information, is crucially important: not only does it help us understand how investors incorporate information into prices, but it also helps investors in general, and portfolio managers in particular, make decisions on trading strategies that involve tracking portfolios or hedging systematic risk.

In this study we draw on recent advances in econometric theory to investigate whether the release of firm-specific information affects the systematic risk of a stock. We find that it does. We estimate daily variations in betas for almost 18,000 earnings announcements across all stocks that are constituents of the S&P 500 index during the period 1996-2006. We uncover statistically significant and economically important variations in betas around news announcements. These variations are short-lived, and thus difficult to detect using lower frequency methods.

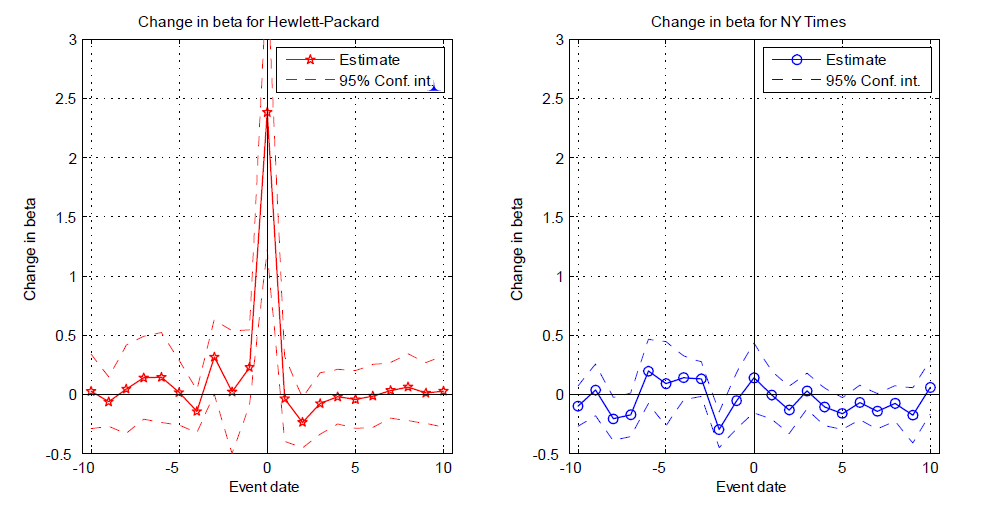

We find a lot of heterogeneity in the behaviour of betas around earnings announcements. Consider, for example, two stocks in our sample: Hewlett-Packard (HP) and New York Times (NYT). Figure 1 shows the evolution of their betas over a window of 20 days around earnings announcements (day 0 is the earnings announcement day), compared to their normal levels of betas measured outside the announcement window. The beta of HP spikes considerably on announcement days, increasing by almost 2.5 from its non-announcement level; in contrast, the beta of NYT remains basically constant.

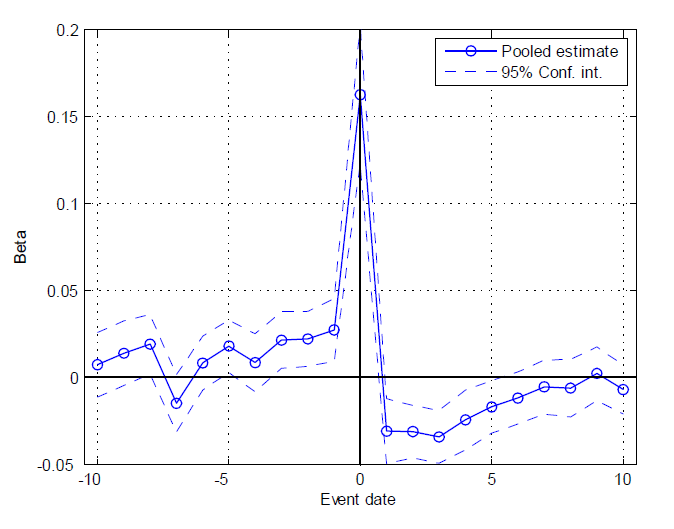

If we look at the average behaviour of betas across all firms in our sample, we find that betas increase by 0.16 on earnings announcement days, drop to 0.03 below their normal level on the following day, and finally revert to non-announcement levels about five days later (Figure 2).

These results are intriguing: without conditioning on whether the earnings news is good or bad, we find that betas spike upward. What might drive this pattern in betas, and the differences we see across stocks? To answer this question we test whether these differences are associated with specific stock characteristics, or with the information environment in which earnings are released. We propose a simple rational model of learning across stocks.

The intuition for our model is as follows. Since firms only announce their earnings once per quarter, on the intervening days investors must infer their profitability from other available information. If the earnings processes of different firms contain a common component, and if different firms announce on different days, then investors can use the earnings announcement of a given firm to revise their expectations about the profitability of non-announcing firms and of the entire economy in general. This process of learning across firms drives up the covariance of the returns of the announcing stock with other stocks, regardless of whether the announcing firm reveals good or bad news: investors interpret good (bad) news from the announcing firm as partial good (bad) news for other firms, which drives up covariances on announcement days, leading to an increase in beta for the announcing stock.

We run simulations and find that this stylized model can reproduce our evidence of an increase in average betas on earnings announcement days. The model also generates interesting cross-sectional predictions. For example, it predicts that the increase in beta is greater for larger earnings surprises (positive or negative), firms whose announcements allow investors to extract more market-wide information, and announcements that entail greater resolution of uncertainty.

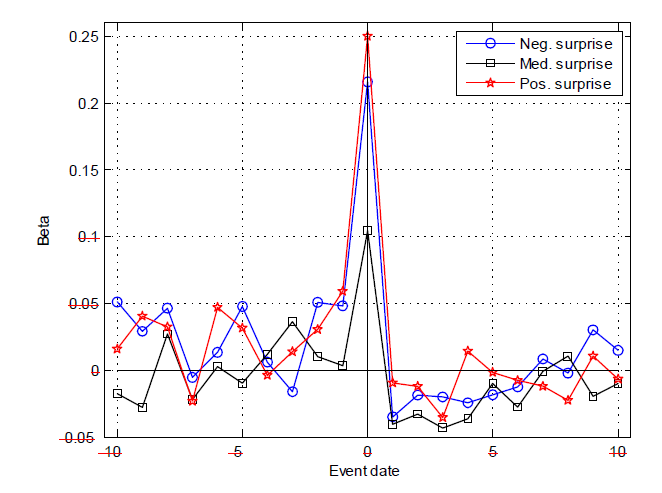

Guided by the testable implications of our model, we first examine the behaviour of betas around earnings announcements with different information content – measured by the earnings surprise relative to the consensus forecast. We find that betas increase significantly regardless of whether the news is good or bad, with spikes of 0.25 and 0.22 for good and bad news, respectively; betas increase only moderately for announcements with little information content (Figure 3).

This result is consistent with an information spillover effect caused by learning: if news about a stock represents partial news for the remaining stocks in the market, then the covariance between the returns of the announcing stock and the market returns increases, regardless of whether the news is positive or negative, as investors incorporate the new information into the price of non-announcing stocks.

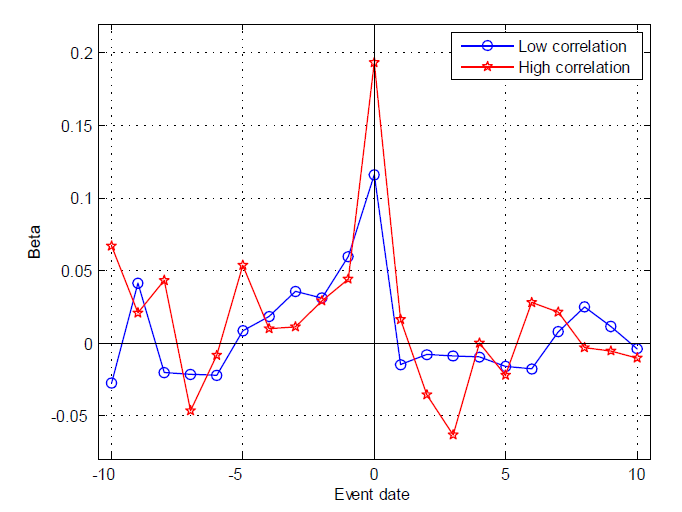

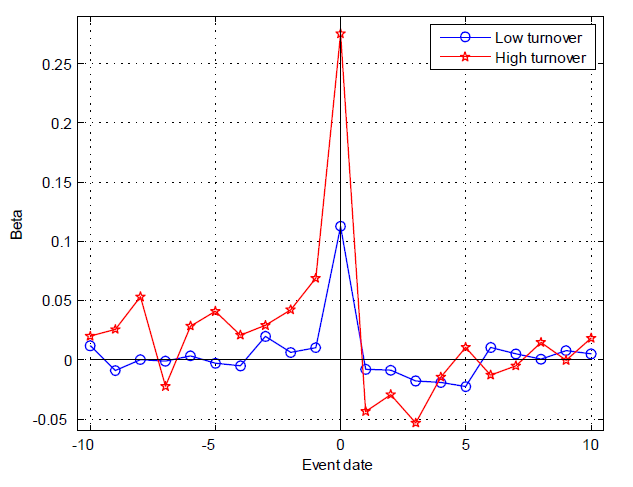

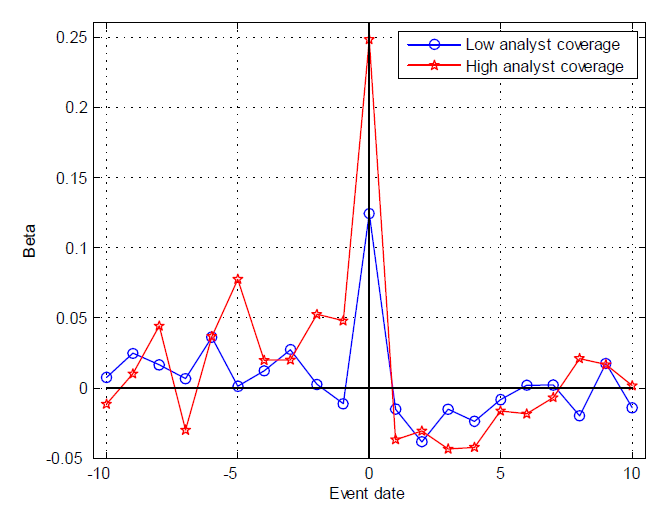

We next investigate whether announcing firms that offer greater potential for learning about the rest of the economy are associated with greater changes in betas. In line with this prediction, we find that the upward spikes in betas are larger for companies whose fundamentals are more highly correlated with aggregate fundamentals (Figure 4). Furthermore, we find that changes in beta on announcement days are larger for stocks with higher volume of trade (Figure 5) and broader analyst coverage (Figure 6).

These findings suggest that investors learn more when the information comes from “bellwether” stocks, i.e., from stocks that are closely followed by traders and analysts, whose earnings are taken to represent information on the prospects of other firms in the market.

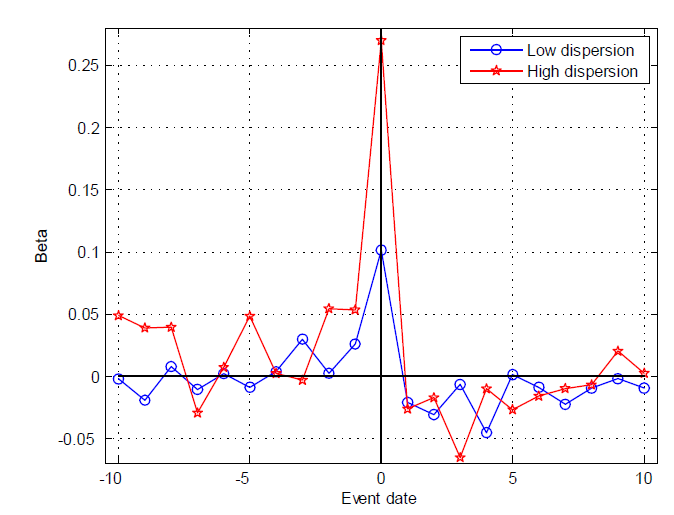

Also consistent with our stylized model, the increase in beta on announcement days is larger for announcements that resolve more uncertainty. We find that stocks with higher dispersion of analyst forecasts of earnings experience a larger increase in beta (Figure 7).

Finally, we illustrate the economic importance of our findings through a portfolio management application. We consider randomly selected portfolios as well as popular long-short strategies such as size, value, and momentum. We then attempt to make these portfolios market-neutral by taking a position in the market index to offset their systematic risk. We find that a model that uses information on changes in betas around earnings announcements is better able to yield market-neutral portfolios, i.e., portfolios with betas that are closer to zero in absolute value.

♣♣♣

Notes:

- This article is based on the authors’ paper Does Beta Move with News? Firm-Specific Information Flows and Learning about Profitability, 2012, Review of Financial Studies 25, 2789-2839.

- This post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Christine Puccio CC-BY-SA-2.0

Michela Verardo is Associate Professor of Finance at the London School of Economics. Her main research interests are in empirical asset pricing, market efficiency, behavioural finance, and mutual and hedge funds.

Michela Verardo is Associate Professor of Finance at the London School of Economics. Her main research interests are in empirical asset pricing, market efficiency, behavioural finance, and mutual and hedge funds.

Andrew Patton is Professor of Economics and Finance at Duke University. His research interests are in econometrics, financial economics, forecasting, volatility and hedge funds.

Andrew Patton is Professor of Economics and Finance at Duke University. His research interests are in econometrics, financial economics, forecasting, volatility and hedge funds.