More and more firms seek to set long-term incentives for their managers. One way to do so is to restrict executives from selling stock and options for a certain period, typically three years. When such stock and options finally become available (“vesting”), many executives are eager to sell.

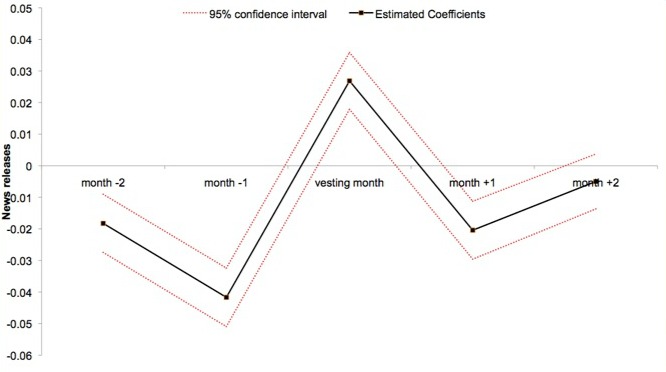

One easy way to boost short-term stock prices is to release news. Even neutral news catch investor attention, which increases the stock price for about two weeks before reverting back. To see whether executives change their news releases strategically, we collect data on 24,668 scheduled vesting events of CEOs in Russell 3000 firms from 2003 to 2011 for our recent paper.

First, we show that CEOs are 23 per cent more likely to sell shares in those months when their restricted compensation becomes available. That means that many of them have an incentive to release more news in such months. And indeed, firms release significantly more news in such CEO vesting months, about one piece of news in every 12 vesting months. These news are more likely to be positive than in other months too. This behaviour makes sense because (even) after such news releases the stock price increases. The executives take advantage of the stock price increase: half of them sell in the two weeks while it lasts.

While we focus on news in this paper, our results can have much broader implications. The increases in news releases during vesting months suggest that executives care about restrictions in their compensation. This is not easy to show as firms with the most long-term projects typically give more grants. That makes it hard to pin down which way the causality goes if we find a positive relationship between long-term behaviour and long-term compensation. In the news setting, the causal direction is more obvious as the vesting events are scheduled several years prior. Back then, it was not so clear yet what will happen three years later, especially not on the monthly granularity of our data.

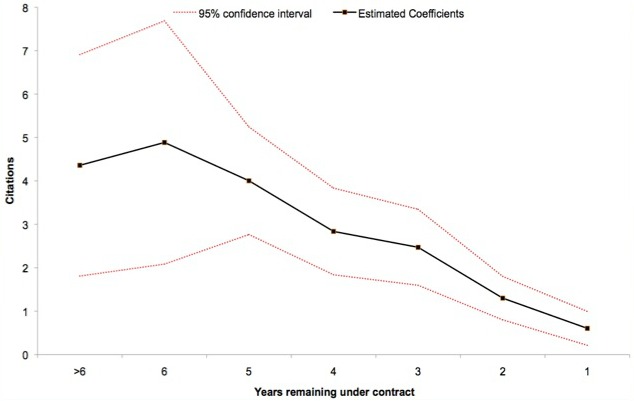

Does long-term compensation also have desired effects or does it only work in the short-term, with news releases? It seems so: Edmans et al. show that firms cut investment in years when more compensation is due to vest. Ladika & Sautner show that firms decrease investment when an accounting reform made it lucrative to accelerate vesting. And short-term incentives are not necessarily bad. In this paper we look at what kinds of patents firms produce. Here we follow the firms throughout the contracts of CEOs, from when they have a long time left until they are up for renewal (or termination).

When CEOs have a lot of time left, firms invest in new technologies and produce a mix of bad and good patents. That is, they take risks that can take a long time to pull off. On average, these patents eventually turn out to be worth more and be more important.

When CEOs are approaching the end of their contract, they consolidate, focus on their best technologies and produce more functional follow-up research towards the marketing of innovation. So: the bad news is that all long-term incentives eventually become short-term incentives. The good news is that you may need a mix of long- and short-term incentives anyway, which means you are able to set optimal incentives after all.

♣♣♣

Notes:

- This post is based on the authors‘ paper Strategic News Releases in Equity Vesting Months, co-authored with Alex Edmans, Luis Gonçalves-Pinto and Yanbo Wang, NBER Working Paper No. w20476 and European Corporate Governance Institute (ECGI) – Finance Working Paper No. 440/2014.

- This post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Newspapers B&S, Jon S CC-BY-2.0

Moqi Groen-Xu is an assistant professor at the Finance Department of the London School of Economics. Her research focuses on CEO contracts, compensation, shareholder activism, proxy voting, and investor relations. Moqi tweets under @moqixu and blogs at www.moqixu.com.

Moqi Groen-Xu is an assistant professor at the Finance Department of the London School of Economics. Her research focuses on CEO contracts, compensation, shareholder activism, proxy voting, and investor relations. Moqi tweets under @moqixu and blogs at www.moqixu.com.