The modern economy is a complex entity, subject to a continual process of change and development. The challenge is to ensure that economic statistics — and the methodologies used to construct them — evolve so as to capture these changes such that they remain relevant, accurate, and timely.

The national accounts provide the basic framework for monitoring the evolution of economic activity, incomes, and expenditure at the national and sectoral levels. As Diane Coyle points out in her 2014 book, GDP: A Brief but Affectionate History, these were first developed in the 1930s and 1940s to systematically measure economic activity during the Great Depression and wartime economic planning. Today, the national accounts are central to the decisions of policymakers and businesses.

Evolving measurement methods

The way we measure the economy has evolved since then in the attempt to keep pace with the changes, but this has also become increasingly difficult. Recent technological advancements have radically altered the way people conduct their lives today, both at work and play. The digital revolution has not only led to rapid quality improvements and product innovation as a result of advances in computing power, but also to new ways of exchanging and providing services as a result of increased connectivity. These developments pose a serious challenge to the way we currently measure economic activity. In this context, eight months ago I was tasked by the UK Chancellor of the Exchequer to assess the UK’s current and future statistical needs. The result has been recently published (Bean 2016).

One particular challenge for economic measurement stems from the fact that an increasing share of consumption is made up of digital products delivered at a zero price or funded through alternative means such as advertising or selling information about customers to third parties. While representing a clear value to consumers, digital products available at a zero price are entirely excluded from GDP, in accordance with the internationally-agreed statistical standards.

Music industry and internet service examples

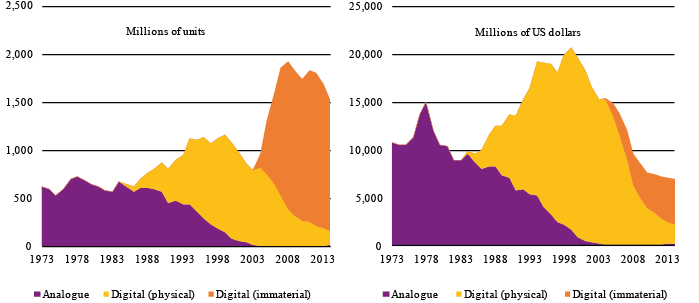

Take, for instance, the music industry. CDs, the dominant medium in the 1990s, have now largely been superseded by a swell in online downloads and streaming services – many of which are available for free or at a flat rate subscription. So the switch to the downloaded format is not reflected in a similar surge in revenues, but instead a sharp fall in both revenues and margins (see Figure 1). In the UK, while the number of streamed tracks has roughly doubled each year since 2012, the revenues from subscriptions have been rising by only 60 per cent each year.

Figure 1. Comparison of units and value of US music sales

In the face of this evolution, record labels have become more involved with licensing live music and associated merchandise. For example, by 2011 less than half of the revenues of the UK records industry came from physical product sales (Page and Carey 2011). But estimates of GDP are hardly invariant to a different choice of business model. Business-to-business transactions count as intermediate inputs rather than value added. Consequently, a large fraction of the production and consumption of the music industry ends up not being reflected in aggregate GDP.

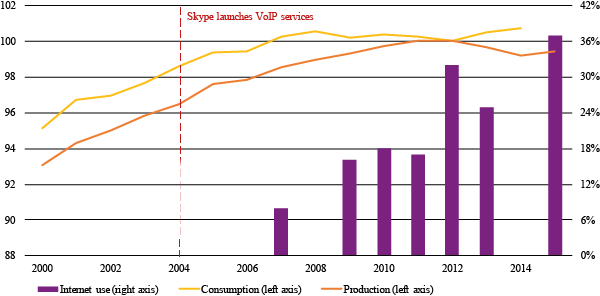

Similarly, it has become possible to make cheap calls over the internet rather than over more expensive telephone networks ever since Skype introduced its Voice over internet protocol (VoIP) service in 2004. As a result, the number of adults making voice or video calls online has increased from around one in ten in 2007 to nearly four in ten today. And about 80 per cent of these users end up paying nothing for their calls (Ofcom 2015). The increase in the number of online communication channels (e.g. email, social media, and instant messaging apps) also reduces the need for conventional voice calls and SMS messaging altogether. But this new form of digital communication appears to be largely absent in official statistics; the last ten years has seen a tailing off in the growth rates of both consumption and production of the telecommunication sector (see Figure 2).[1]

Figure 2. UK internet activity and economic activity in communication services

Nowadays contact with customers increasingly happens online. This has significant implications for consumer-facing business services like banking, travel agents, and insurance. For example, instead of visiting a travel agent, you use free online travel booking services. Activities that were previously undertaken in the market economy have become part of ‘home production’ instead. But, by convention, home production activities (e.g. domestic activities, including cleaning and cooking) are not counted as part of GDP. This tendency for the disintermediation of information-intensive service activities still has a considerable way to run, with potentially significant implications for the interpretation of conventional measures of productive activity.

As a result, the current treatment of digital products in the national accounts inevitably tends to result in the underestimation of the value generated by the digital economy. But figuring out the unobservable value created by the internet-based activities is by no means easy. Several approaches have been suggested to quantify the uncaptured digital activity.

For instance, one could use advertising revenues to impute digital product value (Nakamura and Soloveichik 2015).[2] But because advertising expenditures constitute only a small fraction of GDP, this approach tends to find that allowing for ‘free’ media in this way has only rather a small impact on GDP. There are, however, several shortcomings with this approach to valuing the digital economy.

First, valuing products at cost is potentially misleading when marginal costs are zero as there is no guarantee that the full value of the digital product is captured in the advertising expenditure.[3]

Second, this approach ignores the value of digital services that are produced without requiring any compensation, such as the millions of blogs or Wikipedia entries.

Third, it neglects the value generated by those businesses that do not rely on advertisement revenues, but instead earn revenues by selling (often repackaged) information about the users’ habits. Hence, it provides very much a lower bound on the value of digital product.

Alternative measurement approaches

Alternatively, the value of the uncaptured digital activity can be inferred from the opportunity cost (see Becker 1965) of the time spent online using free digital products (Goolsbee and Klenow 2006, Brynjolfsson and Oh 2012) or adjusting the telecommunication services output to account for the rapid growth in internet traffic (Mandel 2012). Both approaches suggest that accounting for this activity could add between one-third and two-thirds of a percentage point to the average annual growth rate of the UK economy over the past decade.

The digital revolution is also disrupting traditional business models. The reduced search and matching costs offered by a range of online marketplaces are unlocking the market for skills (known as the ‘gig economy’) and the market for underutilised assets (known as the ‘sharing economy’). But the traditional statistical distinction between firms producing and households consuming leaves little room to account for households as value creators, which poses conceptual and practical measurement challenges.

The gap between what is measured and what is valued grows every time a new good or service is introduced or whenever existing goods or services become available for free – as is often the case in a digitising world. Now is the time to ask ourselves whether the current framework of the national accounts is flexible enough to capture the full extent of the transformation brought about by the digital revolution. The risk of postponing this discussion is that the fast pace in the development of the digital economy would drive a possibly fast spreading rift between what in principle we are trying to measure and what is instead captured by the official statistics.

Concluding remarks and a proposed network

For the UK, I have proposed that the statistical authorities establish a centre of economic measurement. This network will bring together leading academics, industry, and expert users to undertake research and development into the measurement of the economy, and propose experimental statistics to capture the new phenomena.

To be agile in measuring these new phenomena, national statistical institutes should be leaders in exploiting existing and new data sources. In order to build up the capability to unlock this trove of information, I have recommended that the UK establishes a hub for the development and application of data science techniques. This hub will make use of the data already held by government and explore the potential for using new techniques of collecting and analysing private sector big data, such as web scraping, text-mining, and machine learning.

The UK is by no means alone in facing these challenges. Ensuring statistics accurately reflect a changing economy is one of the hardest challenges faced by national statistical institutes worldwide. A progressive response to these challenges requires them not only to be abreast in understanding and explaining the limitations of its statistics, but also the ambition and curiosity to develop more appropriate measures.

[1] This is even more surprising if one notes that these figures include the cost of accessing the internet.

[2] This methodology builds on the work of Cremeans (1980), who proposed a barter mechanism for measuring free media and is consistent with the tradition of valuing products at cost when consumption is not purchased (e.g. public goods and services) or unpriced (e.g. owner-occupied housing and financial intermediation services).

[3] Most web sites and apps are built with free, open-source applications. This makes producing and running a site or app cheap. Moreover, the rapid fall on the cost of production for digital goods has meant that there is now an oversupply of advertising space, so that the cost of advertising itself has also been reduced by the advent of the digital economy.

Watch Sir Charles Bean discuss his review of UK economic statistics

♣♣♣

Notes:

- This article was originally published in Vox, the Policy Portal of the Centre for Economic Policy Research (CEPR).

- This post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Pexels

Charles Bean is a Professor of Economics at LSE. From 2000 to 2014, he served at the Bank of England as, successively, Executive Director and Chief Economist, and then Deputy Governor for Monetary Policy, in which capacity he was a member of the Monetary Policy and Financial Policy Committees. Before joining the Bank, he was a member of faculty at LSE and was Managing Editor of the Review of Economic Studies; he has also worked at HM Treasury. He was President of the Royal Economic Society from 2013 to 2015 and was knighted in 2014 for services to monetary policy and central banking. He holds a PhD from MIT.

Charles Bean is a Professor of Economics at LSE. From 2000 to 2014, he served at the Bank of England as, successively, Executive Director and Chief Economist, and then Deputy Governor for Monetary Policy, in which capacity he was a member of the Monetary Policy and Financial Policy Committees. Before joining the Bank, he was a member of faculty at LSE and was Managing Editor of the Review of Economic Studies; he has also worked at HM Treasury. He was President of the Royal Economic Society from 2013 to 2015 and was knighted in 2014 for services to monetary policy and central banking. He holds a PhD from MIT.