On 21 January 2016, the International Monetary Fund approved disbursement of a USD 114 Million loan to Ghana. It was the third such effort in the recent past to align the economy’s sails towards greater stability. Even though this played a pivotal role in defusing a pervasive sense of crisis, investors have grown wary of the woes bedevilling what was, not too long ago, the poster child of ‘Africa Rising’.

The last two years have presented a wild ride for Ghana and policy seems to have lost the master stroke to pull the economy out of the rut. It is against this backdrop that investors await the November 2016 general election with great anticipation; on the one hand hoping for continuity in stability, whilst on the other hoping for change in the course that the economy has taken.

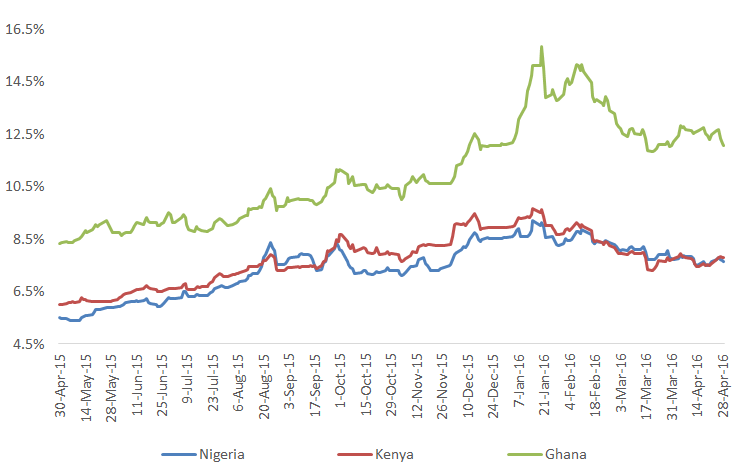

The overarching concern is that Ghana’s economy is grappling with what seems to be a road towards stagflation. Economic growth momentum has lost pace, sagging to a low of 3.5 per cent in 2015 from 14.0 per cent in 2011 at the height of the boom in commodity prices; industry has been hamstrung by the energy crisis that has resulted in frequent disruption of electricity supply; and now the inflation genie is out of the bottle, defying months of aggressive monetary contraction, to tower at 19.2 per cent in March 2016. Investors’ jitters have manifested in the international debt market with the country’s Eurobond yield soaring high above that of regional peers.

Fig.1 Ten Year Eurobond Yields

Source: Bloomberg

It is not lost to investors that with the monetary policy rate at 26 per cent, Bank of Ghana now has to step gingerly on the extent to which it can tighten conditions in the monetary environment to tread that often elusive safe ground between mitigating inflation and choking the economy to near stagnation.

On the fiscal front, the budget for 2016 is anchored considerably on expenditure rationalization and pruning excesses to nudge the budget deficit down to set targets, with little to suggest stimulus spending that could be banked on to rev up the faltering economy in the coming quarters. This shifts focus to the political arena and the agenda of the administration that assumes office following the November 2016 election.

Addressing Constraints & Rebalancing the Economy

More than sending global oil prices tanking further, the collapse of the Doha Talks (April 2016) sent the unequivocal message that if major producers could fail to reach a deal to stabilize their economic lifeline, producers like Ghana, with less of a say at the bargaining table, ought to fast-track the rebalancing and structural transformation of their economies.

Productivity constraints hold back Ghana’s potential as an industrial hub in West Africa. World Bank estimates, for instance, indicate that businesses lose up to 11 per cent of the value of aggregate sales due to power outages, compared to 5.5 per cent suffered by their counterparts in Kenya. It is a major drawback on Ghana’s attractiveness as an investment destination.

The decision to remove visa requirements for all Africans marks a major milestone in the country’s efforts at tapping into the vast potential of deeper regional integration, a frontier that is yet to be well explored by West Africa when benchmarked against East Africa. The Economic Community of West African States boasts US$ 704.4 million in GDP size (just about as large as Switzerland), and portends enormous opportunities for investment, given integration as a catalyst.

Such are the issues that dominate investors’ concern as the country heads to the ballot and there is no telling in which direction the political wind will ultimately blow. In the July 2015 by-election, the incumbent National Democratic Congress wrested the Talensi parliamentary seat from the opposition, an indicator that President John Mahama should not be mistaken for a lame duck as he seeks re-election. Former first lady and National Democratic Party Presidential flag bearer, Nana Konadu Agyeman-Rawlings, is, on the other hand, casting herself as the change candidate at a time when deteriorated economic conditions have created a disenfranchised constituency of voters. Time will tell.

♣♣♣

Notes:

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Accra, Ghana, by YawAnsong, CC BY-SA 3.0

- Before commenting, please read our Comment Policy

Julians Amboko is a Research Analyst with StratLink Africa Ltd, a Nairobi-based financial advisory firm focusing on emerging and frontier markets. He covers macroeconomic research and analysis for Sub-Saharan Africa, including markets such as Nigeria, Kenya, Ethiopia, Ghana, and Angola.

Julians Amboko is a Research Analyst with StratLink Africa Ltd, a Nairobi-based financial advisory firm focusing on emerging and frontier markets. He covers macroeconomic research and analysis for Sub-Saharan Africa, including markets such as Nigeria, Kenya, Ethiopia, Ghana, and Angola.

Ghana’s economic situation is worrisome and raises pertinent questions on just how sustainability will be in the long-run. Good analysis.