Colour Scheme, by Mark Robinson, under a CC-BY-NC- 2.0 licence

Colour Scheme, by Mark Robinson, under a CC-BY-NC- 2.0 licence

The UK will soon break ground on its first new nuclear power plant in more than 20 years now that PM Teresa May has signed off on Hinkley. While clearly a political decision, given the involvement of both French and Chinese companies, my colleagues and I at Bloomberg New Energy Finance are still scratching our heads at how such a project was greenlighted. We’ve spent two years analysing the project, and it’s clear: by the time the plant is operational in 10 years it will be completely outdated, trying to keep up with a modernized grid. But perhaps most concerning, Hinkley will cost more than other energy alternatives and will increase electric bills across the UK.

First, a quick recap. Hinkley is a joint venture between EDF, France’s largest utility, and China General Nuclear Power Group, and will cost roughly £18 billion to construct. The blueprint is based on Areva’s reactor technology and is expected to go online in a decade. Supporters of the project say Hinkley is a great idea for three main reasons: 1) it will help secure Britain’s electricity supply 2) the electricity it produces will be carbon free and 3) the project’s approval will pave the way for another 3-5 new nuclear projects, adding 10-14 GW of capacity. Throw in the fact that coal plants around the UK may be forced to retire by 2025, advocates claim Hinkley and new nuclear will propel the UK into achieving a sustainable, and secure, decarbonisation of its electricity sector and economy.

Now, let’s look at the data. The plant is expected to provide just 7 per cent of the country’s annual electricity needs (with a capacity of 3.2GW). Not enough to travel the nuclear road using yesterday’s technology. Here’s why:

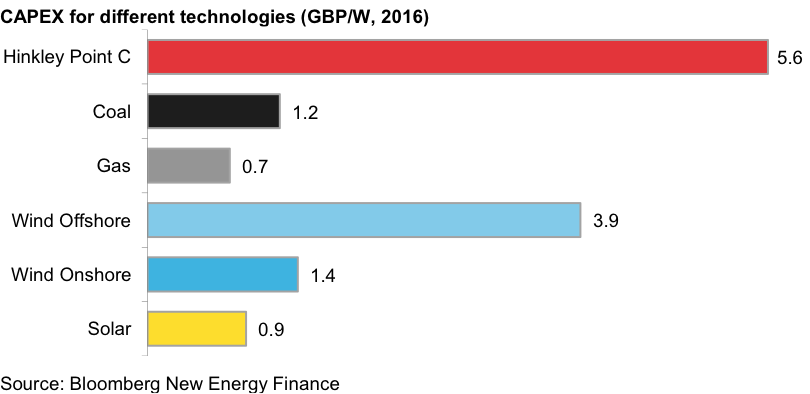

Nuclear energy is expensive. Hinkley will cost EDF £18 billion to build. When we compared this price to any alternative, it’s clear that nuclear is the most expensive option (see chart). Worse still, the UK taxpayer will indirectly fund the project to guarantee its owners’ revenue. To get Hinkley built, the government signed a 35-year, inflation linked, contract for difference (CfD) — a price guarantee —with EDF, at a staggering £92.5/MWh (in 2012). Other new nuclear plants are expected to get similar contracts, both in price and duration. As a comparison, for the 2017/18 delivery year, onshore wind and solar projects received much less, with 15 year CfDs at £80/MWh.

Nuclear is slow to develop. It will take 10 years for Hinkley to get built and produce power. The remaining nuclear projects are expected to have similar time frames. This means the UK’s full nuclear capacity will not be completed prior to 2030. A lot can happen in 15 years, and the UK risks getting “stuck” with a bunch of large nuclear reactors which were commissioned to address a security of supply issue that no longer exists or has been solved by newer, faster technology. Further, the short and medium-term supply concerns that the UK faces — as coal and old nuclear plants shut down — will likely be addressed with new gas plants that will be marginalised once Hinkley starts generating.

Hinkley and its peers are an old technology. As variable renewables — whose output is beyond human control, such as wind and solar —are added to the system, the UK grid will need to balance these with flexible generators. Instead, the proposed nuclear reactors are designed to operate at stable levels, offering almost no flexibility. Further, their sheer size will crowd out new technologies that combine the secure and carbon-free power generation offered by nuclear, with the agility that a system with high wind and solar penetrations needs.

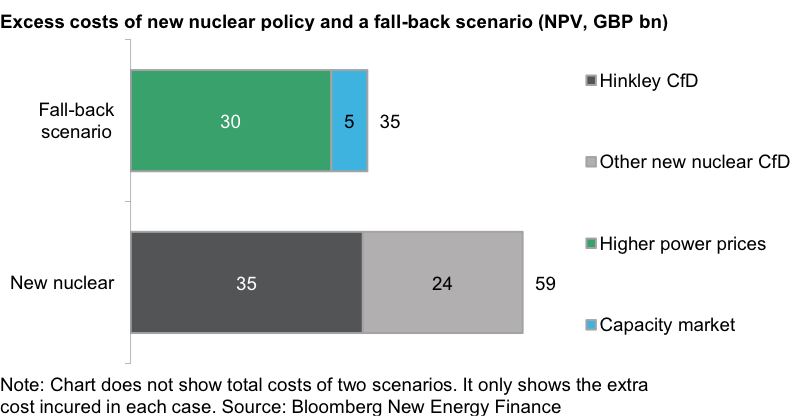

So what’s the alternative, and what does it cost? In order to assess the cost of Hinkley to the UK consumer, BNEF came up with a fall-back scenario. In this set-up we assumed that all existing nuclear plants get their lifetime extended to a 50-year maximum. Though we believe new and clean backup technologies could be competitive in time, in our scenario we make the conservative assumption that any remaining capacity gaps are filled with gas plants. These would be enabled by the capacity market — an auction mechanism to guarantee security of supply. This scenario also pushes up power prices. BNEF then compared the costs of the Hinkley CfD, along with an assumed £80/MWh CfD for the other nuclear projects, to the added capacity market and power market cost of our fall-back alternative.

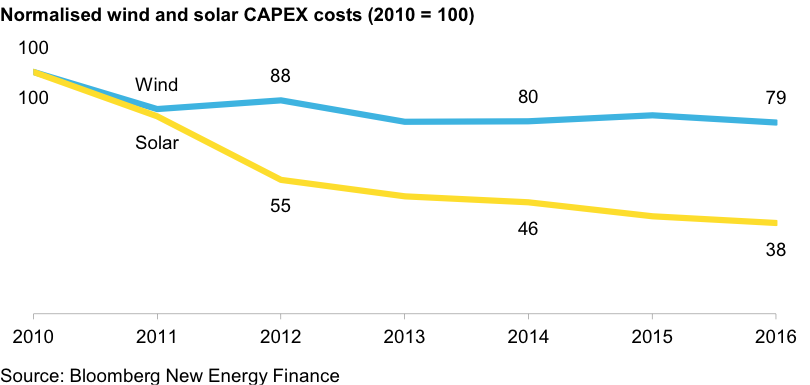

What we found was that the government’s new nuclear policy would cost UK electricity consumers an extra £24 billion compared to our fall-back alternative. This money could be used to encourage the adoption of new, clean, and promising technologies. In the past, government support schemes have driven the build out of uncompetitive technologies, helping lower their costs significantly. For example, wind and solar costs have dropped by 21 per cent and 62 per cent respectively over the last six years, during a period of high government subsidies and build targets.

On the environmental side too, Hinkley and new nuclear plants fail to stand up to our fall-back alternative. It is true that in 2040, a UK electricity sector without nuclear, and (conservatively) assuming more gas, would emit 37 per cent more carbon emissions. This, though, misses three issues. First of all, our modelling shows that between 2015 and 2040, emissions from electricity generation in the UK will fall by 60-70 per cent, irrespective of scenario, the lower end of this range representing the fall-back scenario and the higher end the nuclear scenario. That drop is primarily driven by a large uptake in renewables. Second, the power industry will evolve as rapidly in the next 10 years as it did in the last. Given space and opportunity, new clean, flexible technologies will come to the fore. Finally, nuclear comes with its own environmental concerns, as the storage of spent fuel is a long term issue.

Given the data, all the analysis we’ve written for the past two years is proof that Hinkley Point and the policy it represents come with few advantages that other technologies can’t offer. The disadvantages are many. The UK government is locking bill payers into a few large projects that will deliver a lot less bang for their buck, and divert resources away from other, more promising, technologies.

♣♣♣

Notes:

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy

Andreas Gandolfo is the lead European Power Analyst at Bloomberg New Energy Finance. His recent work has focused on European power market forecasting and integration of EVs in European grids. He holds a BA in Economics and International Relations from Tufts University, and an MS in Mechanical Engineering and Energy System from Columbia University.

Andreas Gandolfo is the lead European Power Analyst at Bloomberg New Energy Finance. His recent work has focused on European power market forecasting and integration of EVs in European grids. He holds a BA in Economics and International Relations from Tufts University, and an MS in Mechanical Engineering and Energy System from Columbia University.

No need to scratch your head any longer about why the UK government is backing Hinkley Point nuclear power station against all known logic. Just read this article from the Science Policy Research Unit of the University of Sussex, then all will become clear: http://www.sussex.ac.uk/broadcast/read/36984#.V-TshqU2QSY.twitter

All the concerns are based on expense and hypotheticals about green energy tech that “might” be ready and cheaper by the time it goes online, but that’s a big might and we’ve got a huge problem now with both carbon emissions and an energy crunch that is already here. This is not a time to get cheap over saving the planet and energy security. We need a mix of all green energy tech and nuclear energy which, by the way, is also green despite its image which mostly really stems from fear of nuclear weapons. The last thing we can do is spend years delaying big carbon free projects.

Green energy is not scalable yet (e.g., a study found that to power California alone via wind turbines would require more steel and copper than exists in the entire globe. Furthermore much of the green energy tech can become hostage to China at any time, which produces almost all our battery tech. Solar also has a lot of really dirty sourcing costs including Uighur slave labor, tons of coal used in the process, large transportation footprint, etc.

However, it is also true that there is also a major overreliance on China for both the raw materials and the refineries required to produce nuclear fuel.