Philip Hammond, by Foreign and Commonwealth Office, under a CC-BY-2.o licence

Philip Hammond, by Foreign and Commonwealth Office, under a CC-BY-2.o licence

In his first Autumn Statement (and last – since he has decided to abolish them in favour of an annual November budget), the Chancellor presented the key forecasts from the Office for Budet Responsibility’s economic and fiscal outlook, the first since the June referendum. While there is still major uncertainty around the likely form of Brexit, the consensus is that it will inflict damage on the economy. The Chancellor highlights the UK’s weak productivity performance and outlines some policies to address it. However, given the scale of the challenge, now heightened by Brexit, the current package of government policies does little to dampen fears for the economic health of the UK.

A worse outlook for the UK

The OBR is used to making forecasts that are subject to uncertain assumptions, but the current climate presents an unprecedented challenge. Like the rest of us, the OBR has little idea about what form Brexit will take, and bases its forecasts on likely lower trade, investment and immigration. The headline figures are pretty grim: Brexit (which it assumes will happen in 2019) will imply a 2.4 percentage point reduction to growth over the next five years and additional borrowing of nearly £60 billion. Government debt is forecast to reach over 90 per cent of GDP in 2017-18, and the previous fiscal targets of achieving surplus by 2020 will not be met. The OBR admits that these estimates are subject to a higher than usual degree of uncertainty, but notes that they are more optimistic than the Bank of England’s latest report and the Treasury’s pre-referendum analysis – and implicitly assume that Brexit is a relatively smooth process — which of course it may not be.

This is set against a fragile recovery from the financial crisis. While headline GDP growth has been relatively strong in recent years, this has been driven by an impressive employment performance (the employment rate is currently at 74.5 per cent, the highest rate since comparable records began in 1971). Productivity – the ingredient necessary for sustainable growth – fell sharply following the financial crisis and has been stagnant ever since, and relatedly, so have wages. Moreover, the UK currently has a very large current account deficit compared to the past and versus other G7 economies, and business investment in both capital and R&D is lower than in other countries.

Investing in productivity growth

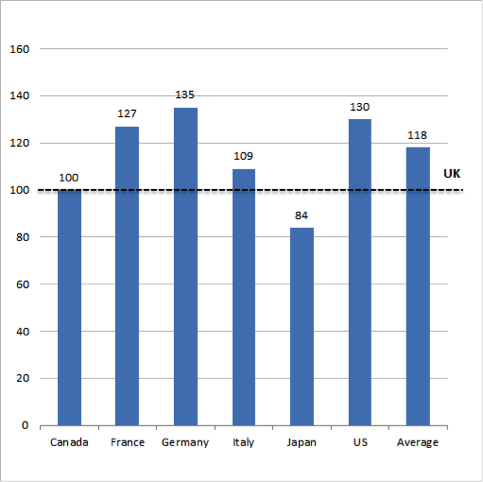

As expected, Hammond confirmed that government would remain committed to fiscal balance, but would adopt a more “flexible” approach. In this vein, and highlighting the UK’s long-standing and well known productivity gap with other advanced economies (Figure 1) he announced the new National Productivity Investment Fund (NPIF), worth £23 billion, to be funded through additional government borrowing, and to be used in R&D and infrastructure.

Figure 1: The UK’s productivity gap with other G7 economies

Notes: ONS International Comparisons of Productivity – First Estimates, 2015, Date: 6 October 2016. Table 1: Current price GDP per hour worked. UK=100.

Since the austerity and reduced private sector investment that has followed the financial crisis, there has been a strong case for government to exploit low interest rates and fund productive investment. The NPIF is therefore welcome news, particularly coupled with the newly established National Infrastructure Commission which should help identify the most valuable projects. However, this new fund is unlikely to be enough, given the scale of the challenge. In infrastructure, it is largely agreed that the planning regime represents a major impediment to development. And more action is required to reduce the cost of capital of infrastructure projects in order to attract private investment (without the need for guarantees that end up costing the taxpayer more).

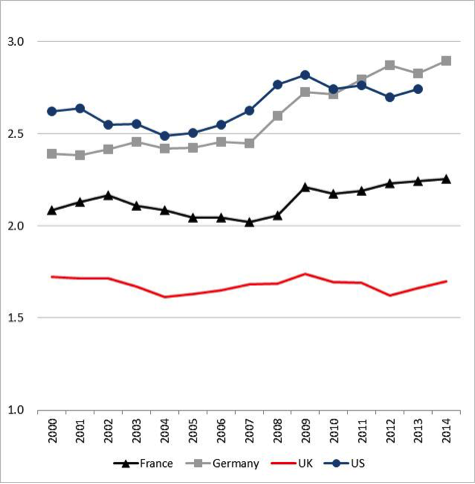

The £2 billion annual additional funding allocated to the science budget is a step in the right direction, but it would take total R&D spending as a share of GDP to 1.8 per cent (from the current 1.7 per cent) – whereas our main comparators tend to spend more (figure 2). At the same time, Brexit introduces new risks to the university and research sector which tend to be international and outward looking, through potentially fewer international students, academics, access to funding and cross-border collaborations: government should consider ways to mitigate these risks.

Figure 2: Spending on R&D (government and business) as a percentage of GDP

Notes: Gross domestic expenditure on R&D (GERD), percentage of GDP. Source: OECD Dataset: MSTI, extracted on 24 October 2016.

The UK needs to get better at commercialising ideas, and one key issue has been access to finance. The Chancellor announced that there will be a review into barriers to accessing patient capital – and boosting the British Business Bank, which provides finance to high growth SMEs, is likely to help. But given the lack of competition in the banking sector, and issues of short-termism in UK business and financial markets – other levers could be beneficial. We can expect more from government in this area as its industrial strategy is developed – Theresa May has indicated that a white paper will be published in the New Year.

There was little mention of skills in the Autumn Statement, though Hammond did indicate that there would be continued support for improving management capabilities – which have been shown to matter for productivity. The UK has long-standing skills gaps – both in specific areas where shortages are reported (STEM subjects and languages, for example), but also in basic literacy/numeracy and more generic soft skills. Given that UK plc will be less able to import skills, it seems more important than ever that we invest in our education system. Yet there were no announcements of additional funds for schools or further education. Moreover, government plans to promote grammar schools are unlikely to raise average standards and would favour better off families.

Inclusive growth

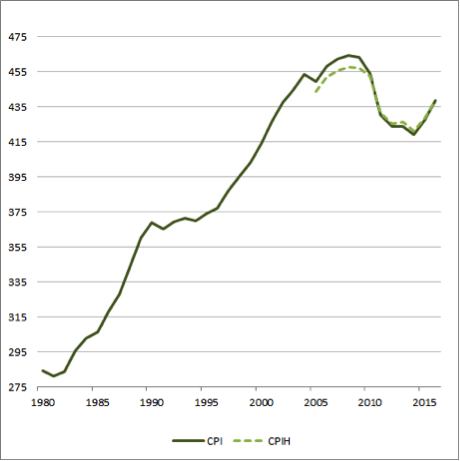

It is not only important to focus on growth, but also on how its gains are distributed across society. Median worker pay is still 4-5 per cent lower than its pre-crisis peak (Figure 3), corresponding to almost a 20 per cent drop relative to the trend in real wage growth from 1980 to the early 2000s. Given the economic outlook, it seems unlikely that prospects are going to improve in the near term.

Figure 3: Median Worker Pay

Notes: Median real weekly earnings, 2015 prices. Source: Annual Survey of Hours and Earnings (ASHE) weekly earnings numbers, deflated by CPI and CPIH (from 2005).

Hammond highlighted the challenges surrounding the “gig economy” whereby increased self-employed status is reducing tax income. It is important to consider how the tax code and regulations can evolve to respond to these types of issues that arise due to rapid technological change.

What more can be done?

The LSE has re-launched its Growth Commission, which first reported in 2013 with a set of recommendations around infrastructure, skills and financing innovation – some of which, most notably the National Infrastructure Commission, were adopted, but many of which still apply today. In light of developments since 2013, the Commission will now focus on four key areas: openness, finance and the city, industrial policy and labour markets.

The Commission is drawing on evidence given in public evidence sessions by business leaders, academics, policymakers and stakeholders in the UK economy, and will be reporting in January 2017.

♣♣♣

Notes:

- The post gives the views of the author, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy.

Anna Valero is an Economics PhD candidate at the LSE, a Research Economist at the Centre for Economic Performance and a member of the LSE Growth Commission Secretariat. Her work is focused on firm organisation and workforce skills, and their effects on productivity and innovation. More generally, Anna is interested in understanding UK economic performance, the drivers of growth and implications for policy. Before resuming her studies, Anna was at Deloitte for a number of years where she was a Manager in the Economic Consulting practice and qualified as a Chartered Accountant.

Anna Valero is an Economics PhD candidate at the LSE, a Research Economist at the Centre for Economic Performance and a member of the LSE Growth Commission Secretariat. Her work is focused on firm organisation and workforce skills, and their effects on productivity and innovation. More generally, Anna is interested in understanding UK economic performance, the drivers of growth and implications for policy. Before resuming her studies, Anna was at Deloitte for a number of years where she was a Manager in the Economic Consulting practice and qualified as a Chartered Accountant.