Proponents of the blockchain technology envision a world without financial service providers. Asset ownership would thereby be recorded in a distributed, non-manipulable ledger – the blockchain – that is stored on each participant’s computer. Except for the digital currency bitcoin, this technology has not been widely applied so far. Many promises surrounding blockchain exist. The most important ones are examined here.

Blockchain is cheaper than the current payment system

The more people use blockchain and the more transactions occur, the larger the blockchain becomes. Depending on participation in the system, projections for 2030 estimate the size of Bitcoin’s blockchain to lie between 0.1 terabyte and 1.9 billion terabyte. Corresponding storage space would be needed on each participant’s computer. While the storage capacities grow exponentially, the scale still implies that the blockchain technology will not work on mobile devices.

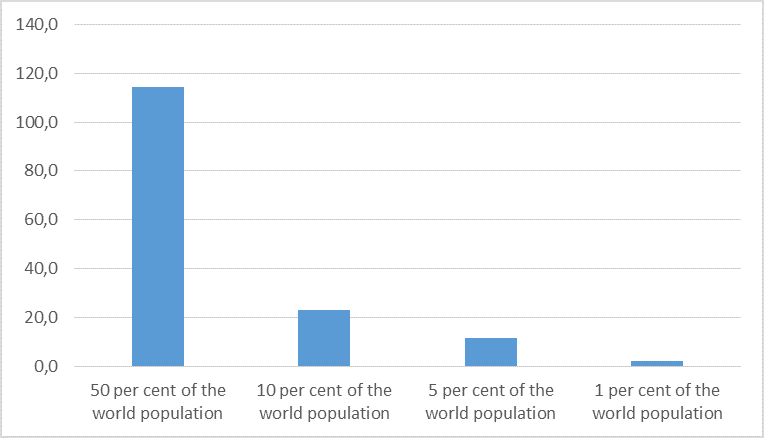

A rising participation in a blockchain system would also imply that a larger number of transactions would need to be validated by miners, which are computers competing to find a solution to a complex arithmetical problem. Miners consume energy, in 2013 about 23.5 GWh per day in the bitcoin network. Projections for 2030 show that an increase in participation would result in a yearly energy consumption by the miners that could exceed today’s worldwide energy supply by 14 per cent (see figure 1). The share of energy consumption of the service sector is currently at 13 per cent with payment systems’ energy consumption only part of this. Even in case of low participation in blockchain, its energy consumption would still be significant.

Figure 1: Energy consumption of the mining process

Note: Yearly energy consumption of the bitcoin blockchain mining process in 2030 as percentage of worldwide energy supply in 2014 for different population participation rates. Source: blockchain.info, International Energy Agency, Sorge/Krohn-Grimberghe, United Nations, own calculations

Blockchain is faster than the current payment system

Currently, the verification of a transaction in Bitcoin’s blockchain takes 9.3 minutes. VISA’s payment system can process 2,000 transactions per second on average. Hence, the blockchain technology is relatively slow compared to VISA. However, in the current payment system, cross-border transfers of money often still take a couple of days: Several banks and central banks are involved and their processing systems for these transactions are not standardized. In addition to that, the duration also depends on compliance obligations with anti-money-laundering laws. These really should also apply to blockchain service providers. Overall, the blockchain technology might be faster than current technology in some cases. However, that is mainly due to missing standards and regulatory obligations.

Blockchain does not need a regulated third party

Participants in blockchain transactions should be compliant with comparable rules and regulation as participants in the current system. The question is who should be responsible for ensuring compliance with the regulatory framework. In a blockchain transaction there is no intermediary. Instead, miners are the service providers. Hence, they could be the entities to be regulated and supervised. Legislators should consequently consider registration requirements for miners, e.g. in form of a single passport for supplying mining services in the EU.

Blockchain is less error-prone than the current payment system

Errors can occur whenever human interaction is involved. The blockchain technology removes human interaction and replaces it with code. It may therefore be less error-prone. However, the smooth functioning of the blockchain technology depends on its code. If there is a loophole embedded in the code, fixing it is impossible. As the hacking of Ethereum’s Distributed Autonomous Organization (DAO), a blockchain investment fund, has shown, blockchain proponents interpret the blockchain’s code as a legal contract. In this incident, one of the participants was able to use a loophole in the code to transfer money from other participants into a sub-fund via a splitting function. According to the DAO’s legal contract, all rules are defined by the code itself, so there is legal uncertainty whether this was theft or just a feature of the code. Legal liability with respect to the blockchain technology seems to remain unsolved. If it actually replaces a payment system, it needs to be ensured that the standards for legal liability in cases of error, fraud or non-compliance are maintained. Whether the blockchain is a company or a contract or just a code needs to be legally defined.

Blockchain is safer than the current payment system

The blockchain technology relies on miners to validate transactions. Blocks are validated only if there is consensus among the miners about the most recent version of the blockchain. However, this reasoning only works if the pool of miners is large. If more than 50 per cent of the miners’ computing power were in one hand, manipulation would be possible. Today, 19 mining pools share 98.8 per cent of the market for mining services. However, the largest four miners’ combined market share makes up 56.7 per cent of the total market. An unregulated and oligopolistic market for mining services might facilitate manipulation of the blockchain. This would be particularly likely if there was a geographical concentration of miners in countries with lax or non-existent regulation. Moreover, mining is also possible via so-called botnets – huge networks of hijacked internet-of-things devices such as routers or cameras. Legislators and regulators should create a framework for ensuring fair competition among miners and a non-discriminatory treatment of blockchain participants.

Summing up, it is still uncertain whether the blockchain will be a disruption to financial services. For a well-functioning market for blockchain applications to emerge, these have to be able to compete with current systems. Blockchain services need a legal definition and should be compliant with rules and regulation. Moreover, there should be registration requirements for mining services as well as supervision since miners could become critical infrastructure.

♣♣♣

Notes:

- This blog post appeared originally on the website of the Cologne Institute for Economic Research.

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Power (cropped), by IF, under a CC0 licence

- Before commenting, please read our Comment Policy.

Markus Demary is senior economist in the research unit financial and real estate markets at the Cologne Institute for Economic Research (Institut der deutschen Wirtschaft Köln). He studied economics at the Rheinische Friedrich-Wilhelms-Universität Bonn and he holds a doctoral degree from the Christian-Albrechts-Universität zu Kiel. Moreover, he is lecturer for Behavioral Finance at Ulm University.

Markus Demary is senior economist in the research unit financial and real estate markets at the Cologne Institute for Economic Research (Institut der deutschen Wirtschaft Köln). He studied economics at the Rheinische Friedrich-Wilhelms-Universität Bonn and he holds a doctoral degree from the Christian-Albrechts-Universität zu Kiel. Moreover, he is lecturer for Behavioral Finance at Ulm University.

Vera Demary is head of the research unit “Structural Change and Competition” at the Cologne Institute for Economic Research (Institut der deutschen Wirtschaft Köln). She studied economics at Paderborn University, Memorial University of Newfoundland and Erasmus University Rotterdam and holds a doctoral degree from the University of Cologne. Her current research focusses on topics at the interface of digitization and competition.

Vera Demary is head of the research unit “Structural Change and Competition” at the Cologne Institute for Economic Research (Institut der deutschen Wirtschaft Köln). She studied economics at Paderborn University, Memorial University of Newfoundland and Erasmus University Rotterdam and holds a doctoral degree from the University of Cologne. Her current research focusses on topics at the interface of digitization and competition.

Perhaps its important to mention that this is a type of blockchain (which is the infrastructure underlying bitcoin), rather than blockchain as a general concept. The underlying components are being used in many ways across a wide range of industries. Some are permissioned networks requiring no mining or complicated consensus protocols. This is only touching a very small segment of the market