Built in 1927 on the eve of the Great Depression, the Palm Beach residence of President Donald Trump – Mar-a-Lago – ranks among the 20 biggest houses in the United States. At 62,500 square feet, it is about 35 times the size of the median suburban house in the country.

Analysing a large dataset of houses built between 1920 and 2009, my research asks whether this kind of ‘upscaling’ of housing size at the top of the distribution incited US households to ‘keep up with the Joneses’, with ultimately disastrous consequences in the 2008 financial crisis.

Classical economists from Adam Smith to Karl Marx were certainly aware of the potential impact of ‘upward-looking’ comparison effects on economic behaviour. Smith noted that ‘It is from our disposition to admire, and consequently to imitate, the rich and the great, that they are enabled to set, or to lead what is called the fashion’; while according to Marx, ‘a house may be large or small; as long as the neighbouring houses are likewise small, it satisfies all social requirement for a residence. But let there arise next to the little house a palace, and the little house shrinks to a hut.’

From 1940 onwards, suburbs accounted for more US population growth than central cities and, by 2000, half of the entire population lived in the suburbs of metropolitan areas. This period simultaneously saw an impressive upscaling in the size of suburban single-family houses: the median newly built suburban house doubled in size after 1945, while the top 10 per cent of houses built – ‘superstar houses’ – experienced an upscaling of nearly 120 per cent, reaching an average size of 7,000 square feet on the eve of the financial crisis.

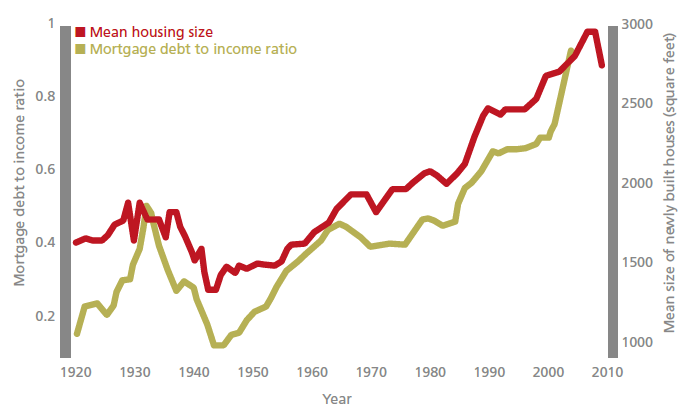

Meanwhile, the ratio of mortgage debt to income went from 20 per cent of total household income in 1945 to 90 per cent in 2008, following a trend that closely matched the historical variation in housing size (see Figure 1).

Figure 1. Changes in US housing size and the ratio of mortgage debt to income since the 1920s

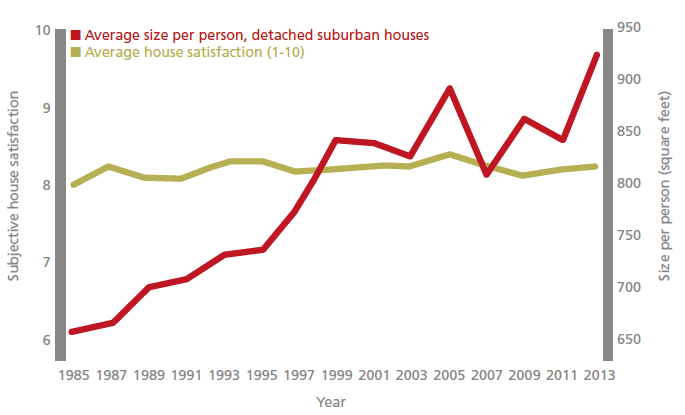

Despite this major upscaling in housing size, there was no increase in households’ expressed satisfaction with their homes after the 1980s. The flatness of the house satisfaction curve evidenced in Figure 2 is particularly puzzling considering that within any given year since 1984, the correlation between housing size and house satisfaction is positive and significant.

Figure 2. Changes in average US house size and average house satisfaction since the 1980s

This result echoes the Easterlin paradox, according to which increasing the income of all does not increase the happiness of all. The paradox has been explained in part by the income comparisons between individuals: if people care about their income relative to others, a relative gain for some leads, by definition, to a relative loss for others.

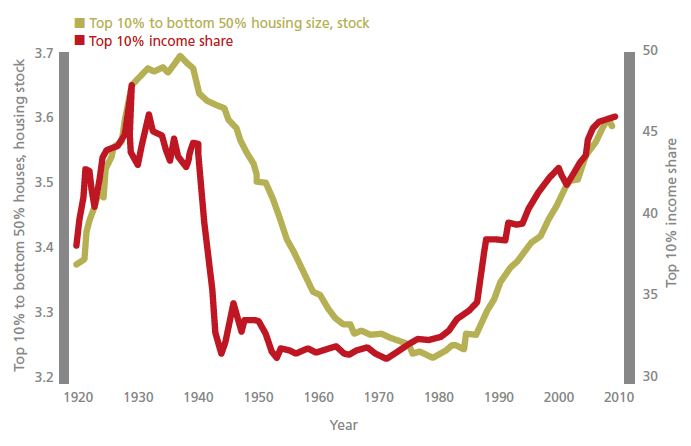

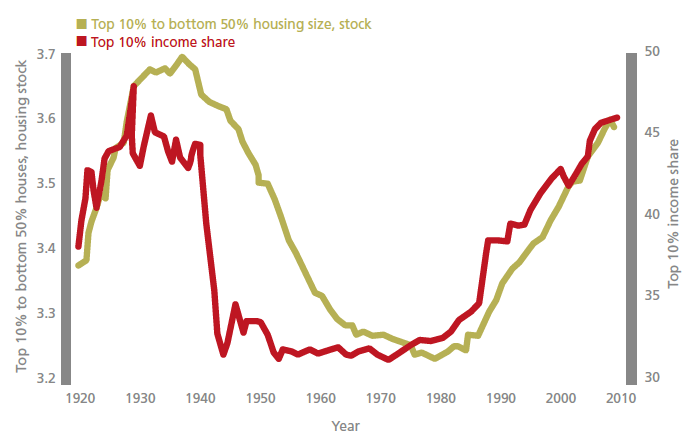

My research reveals that the distribution of housing size followed the U-shaped pattern of top income inequality over a century. As Figure 3 shows, the income share of the top 10 per cent of the US population fell dramatically from around 1940, but then started rising again in the mid-1970s and returned to its pre-war peak in the 2000s. Similarly, the ratio between the size of the top 10 per cent of housing size and the 50 per cent below the median fell from the late 1930s and went back up again from around 1980.

Figure 3. The U-shaped patterns of top income inequality and the distribution of US housing size since the 1920s

I examine if there is evidence that homeowners experiencing a relative downscaling of their house following the construction of bigger units around them value their house less in comparison with similar households who experienced no such change. The data I analyse combine 18 waves of the American Housing Survey from 1984 to 2009 with an original sample of more than three million suburban houses built between 1920 and 2009. My empirical strategy exploits differences in house construction histories across different cohorts of movers, over time and across suburbs.

Suppose two similar households who lived in the same suburb are both surveyed in 1995. The suburb’s variation in top housing size saw a sharp increase between 1980 and 1990 but no rise after that. The only difference between household A and household B is that A moved in 1980 while B moved in 1990. According to my hypothesis based on Easterlin, unless they perfectly internalised future variations in housing size when buying a house, household A, which experienced a rise in top housing size, should be less satisfied than household B, which experienced no change at all.

Figure 4 illustrates the intuition of the research. It compares cross-sectional experienced variation in housing size inequality between old and recent movers, using the same inequality measure as in Figure 3. I find that suburban owners who experienced a relative downscaling of their home record lower satisfaction and house values.

Figure 4. Variation in US housing size inequality between old and recent movers

The richness of my dataset allows me to exploit changes along various segments of the size distribution within suburbs and over time to test which part of the distribution matters. I find that comparison effects are upward-looking, with people in smaller houses looking enviously at neighbours with bigger ones. Being surrounded by houses smaller than the household’s own house does not significantly affect house satisfaction. The utility gains from an increase in own housing size are offset by a similar increase in size of superstar houses, in line with trickle-down theories of consumption.

I further show that when bigger houses get built closer to smaller houses, house satisfaction is lower among the smaller households. The effect is concentrated in suburbs where size inequality is high but segregation is minimal due to geographical constraints on developable land. Thus the relative size effect depends on economic segregation within counties, defined by the distance separating superstar houses from houses below median size.

Lastly, I turn to the relationship between elative house size and mortgage debt. My research provides evidence of a link between top income inequality and household debt. I show that relatively deprived households want to keep up with the Joneses. They react to relative deprivation by increasing the size of their house and subscribing to new mortgage loans. A 1% rise in top housing size during the length of tenure is associated with a 0.1% rise in size through home improvements and a 0.5% rise in the level of outstanding mortgage debt.

Had such households not tried to keep up with the Joneses, I estimate that the ratio of mortgage debt to income would have been 25 percentage points lower on the eve of the financial crisis. This finding is particularly relevant considering the continuous rise in income inequality in the United States, but also given the extensive use of minimum lot size requirements in suburban communities. Zoning regulations, by locally increasing the size of new houses built compared with the size of those before they came into place, may very well have amplified upward-looking comparison effects and increased financial distress, with no long-term improvement in overall house satisfaction.

♣♣♣

Notes:

- This blog post appeared first at CentrePiece, the magazine of LSE’s Centre for Economic Performance, and is based on the author’s paper The Paradox of the Joneses: Superstar Houses and Mortgage Frenzy in Suburban America, CEP Discussion Paper No. 1462

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics and Political Science.

- Featured image credit: Suburbia, by David Shankbone, under a GFDL or CC-BY-SA-3.0 licence, via Wikimedia Commons

- Before commenting, please read our Comment Policy.

Clément Bellet is a research officer in CEP’s wellbeing programme. His research participates in an attempt to reconcile the consumption and savings literature with important findings in behavioural economics, in particular with happiness economics and theories of social preferences. He has been examining ways in which inequality affects choices and wellbeing due to externalities in individual preferences, in India and the United States. He explores issues relative to conspicuous consumption and social status, marketing, happiness at work, inequality and poverty. Clément completed his PhD in economics at Sciences Po Paris and was a visiting scholar at the University of California Berkeley in 2014-2015. He previously worked as a Short Term Consultant for the World Bank.

Clément Bellet is a research officer in CEP’s wellbeing programme. His research participates in an attempt to reconcile the consumption and savings literature with important findings in behavioural economics, in particular with happiness economics and theories of social preferences. He has been examining ways in which inequality affects choices and wellbeing due to externalities in individual preferences, in India and the United States. He explores issues relative to conspicuous consumption and social status, marketing, happiness at work, inequality and poverty. Clément completed his PhD in economics at Sciences Po Paris and was a visiting scholar at the University of California Berkeley in 2014-2015. He previously worked as a Short Term Consultant for the World Bank.