Between May and December 2008, Western Digital, one of the largest computer hard disk manufacturers in the world, experienced a severe shock*. Its stock price fell from $37.53 to $11.45. In 2009, the company reported in its proxy statement that it used discretion, as opposed to objective performance metrics, for evaluating its CEO. In 2008, it had not used discretion in the executive’s performance evaluation. Western Digital thus changed how it evaluated its leader after the 2008 shock. This example illustrates the argument of my recent study that shocks have implications for how firms evaluate their CEOs.

Normally, when a firm’s compensation committee evaluates the CEO, it is well informed about them and their role in generating firm value. This changes when a shock, like the one Western Digital experienced in 2008, occurs. After the shock, the compensation committee lacks information about the post-shock environment. It does not know how the CEO will cope with this new environment, nor how they will contribute to objective measures of firm performance that are commonly used as a basis for compensating them (e.g., reported income).

In the aftermath of a shock, the compensation committee needs to estimate the role of the CEO in driving objective performance measures. This estimation process introduces estimation risk into the performance evaluation. Estimation risk refers to the possibility that the compensation committee may misestimate the CEO’s contribution to objective performance measures, and attribute too much or too little responsibility to the executive.

CEOs are risk-averse and dislike any type of risk, including estimation risk. To lower the executive’s exposure to estimation risk, the compensation committee reduces the role of objective performance measures in their performance evaluation. As a result, CEO compensation will depend less on objective performance measures like reported income.

In a recent study, I test this conjecture using data on 2,737 U.S. firms. Of these firms, 1948 (71.2 per cent) experienced at least one shock between 1950 and 2012 (see the notes below for how I define shocks). I document that CEO compensation is less sensitive to reported income in the year after the shock than before the shock.

An important question then arises: if, after a shock, the compensation committee relies less on objective performance measure for CEO evaluation, how does it go about evaluating the CEO? I argue that it waits until year end to appraise the CEO using discretion. This approach offers the compensation committee time to gather additional information about the firm’s post-shock environment; it can wait until the year is over to adjust CEO pay subjectively based on information obtained during the year.

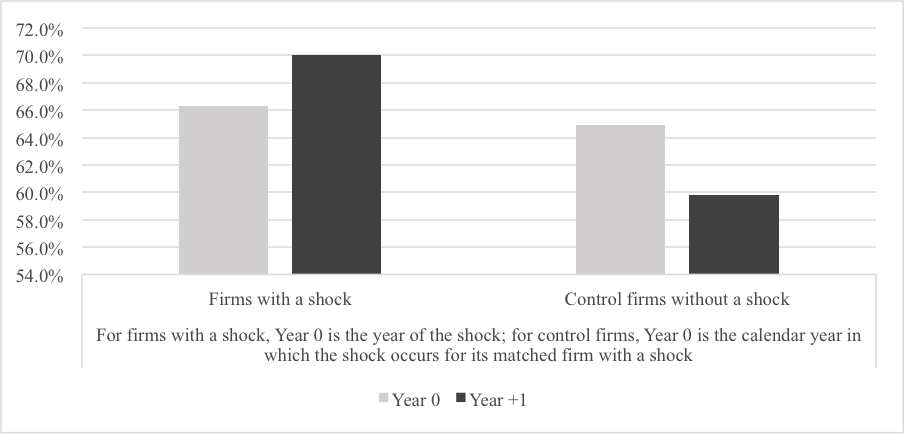

My study shows that, after a shock, firms emphasize subjective CEO performance evaluation and use discretion at the end of the year to appraise them. Figure 1 indicates that 70 per cent of the firms I examined use some form of discretion for evaluating their CEO in the year after a shock, up from 66.3 per cent before. During the same time period, control firms without a shock that were similar in size to firms with a shock and operated in the same industry, decreased their use of discretion in CEO performance evaluation: 59.8 per cent of them evaluated their CEOs using some form of discretion, down from 64.9 per cent.

Figure 1. Percentage of firms that use subjective performance evaluation for appraising their CEO

As time passes since the shock occurred, the compensation committee accumulates information about the post-shock environment in which the firm operates, and learns about the CEO’s role in driving objective performance measures. It then has again more precise information about their contribution to objective performance measures. Estimation risk declines, and the compensation committee relies to a larger extent on objective performance measures when evaluating the CEO. Their compensation will depend again more on objective performance measures.

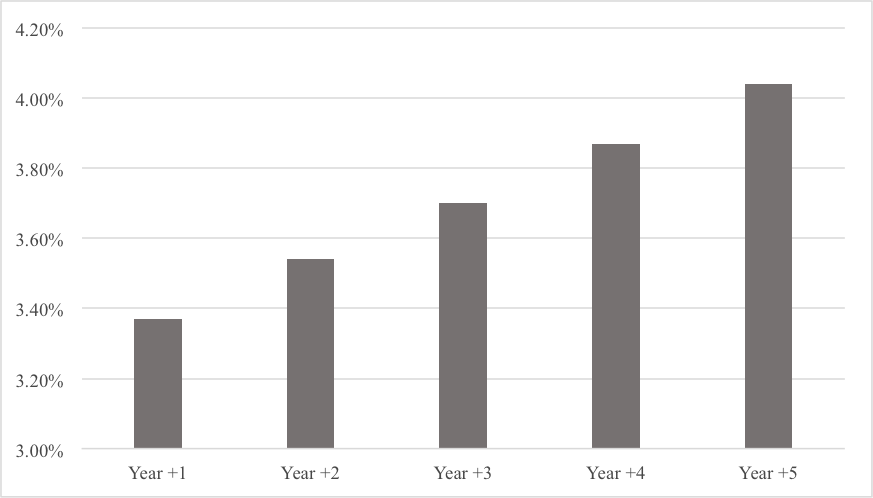

Consistent with this conjecture, my study indicates that, as a shock recedes further into the past, CEO compensation becomes more sensitive to objective performance measures such as reported income. Figure 2 shows that, in the first year after a shock, the sensitivity of their compensation to reported income is such that a 10 per cent increase in reported income results in a 3.37 per cent boost in their pay. By the fifth year after the shock, the sensitivity of compensation to performance has increased such that a 10 per cent increase in reported income is associated with a 4.04 per cent rise in the leader’s pay, which represent 20 per cent more than in the first year after the shock.

Figure 2. Percentage increase in CEO compensation when reported income increases by 10%. For each year between Year +1 and Year +5 after a shock

Economic shocks, then, have implications for CEO performance evaluation, which is not static in an environment characterized by shocks. Instead, their performance evaluation fluctuates between its objective and subjective variants: firms rely less on objective evaluation after a shock, when little is known about post-shock performance measures, only to progressively use it more intensely again as time passes since the shock occurred. Moreover, firms replace objective with subjective evaluation right after a shock.

Also, learning plays a key role, especially after an economic shock. Compensation committees need to learn about the new environment that a shock creates, specifically the role of the leader in driving objective performance measures. While they learn, they put objective performance evaluation on hold and, instead, emphasize a subjective one. Once their understanding of the CEO’s role in driving objective performance measures is again more solid, they re-emphasize objective performance evaluation.

Author notes:

- * My main measure of economic shocks is a firm’s market-adjusted stock returns: when these returns are extremely high or low, the firm experiences a shock. I also measure shocks using data on recessions and expansions from the National Bureau of Economic Research.

- I address two alternative explanations for my results. First, a firm could change CEO performance evaluation after a shock not because it fails to understand objective performance measures in the post-shock environment, but because this environment is different from the environment before the shock, and requires distinct performance measures for CEO performance evaluation. Second, firms experiencing fewer shocks have distinct investment, financing, and governance policies that differentiate from firms experiencing more shocks; these distinct policies may account not only for the firms’ shocks but also for how they evaluate their CEOs. I test for these two explanations, and find that they fail to explain my results.

♣♣♣

Notes:

- This blog post is based on the author’s paper Implications of Economic Shocks for CEO Performance Evaluation, in the European Accounting Review.

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: CEO, by Joshua Ness, under a CC0 licence

- Before commenting, please read our Comment Policy.

Claudine Mangen is the RBC Professor of Responsible Organizations and Associate Professor at the John Molson School of Business at Concordia University in Montreal, Canada. Her research concentrates on corporate governance, disclosure, and power. She tweets at @ProfMangen.

Claudine Mangen is the RBC Professor of Responsible Organizations and Associate Professor at the John Molson School of Business at Concordia University in Montreal, Canada. Her research concentrates on corporate governance, disclosure, and power. She tweets at @ProfMangen.

1 Comments