Every government has an industrial strategy however it is articulated: government affects the investment climate for business through tax and regulation; establishes national priorities; invests in skills, infrastructure and research; and procures outputs from the private sector – all of which influence the evolution of the private economy.

In the UK, business and politics have always been intertwined. The desire shown by the political class to nudge and shape firms goes right to the top, with incoming prime ministers often setting out visions for how companies should work soon after arriving in Downing Street.

The tradition stretches right back to Robert Walpole, whose 1721 reforms included subsidies and taxes designed to support the country’s wool manufacturers. Following the Second World War, Clement Attlee’s Labour government introduced laws aimed at ‘distributing industry’ more widely across the country: South Wales and Tyneside were key targets.

A number of policy mistakes occurred in the 1960s and 1970s as governments doubled down on losing bets, wasting billions of taxpayer funds chasing declining industries in which they had no comparative advantage – British Leyland is a famous example. Industrial policy then fell out of vogue, and in the 1980s, Margaret Thatcher ushered in an era of free markets and privatisation – paring back both economy-wide and sector- or place-based interventions.

When Tony Blair’s Labour government instigated wide-ranging economic reforms, most were economy-wide, including a new emphasis on research and development (R&D), public capital investment and a long-term commitment to public education and expenditure on science. The financial crisis in 2008 rekindled interest in industrial strategy in the UK and abroad, and business secretary Peter Mandelson began to develop a case for a return to more selective industrial policy.

But it was his successor Vince Cable in the coalition government who formally set out an industrial strategy that included support for key sectors and technologies, and which was coupled with more focus on place-based policies like the Northern Powerhouse. There was a brief hiatus after the 2015 election, when the government published its ‘Productivity Plan’ but did not commit to an industrial strategy per se.

But following last year’s referendum and this year’s general election, it is time for another phase. Since taking office, prime minister Theresa May committed to a new industrial strategy ‘to get the whole economy firing’, and the government set out its ideas in a Green Paper in January.

The need for an industrial strategy

The experience to date shows that what varies is how far governments have been willing to spell out their industrial strategy, and the arguments that motivate it. The recent UK experience has also shown that there has been far too much chopping and changing in this space – it is a worrying sign when your business department has had four names in the past ten years.

Stable policy frameworks are needed to stimulate business investment, and the UK is in need of a long-term and overarching modern industrial strategy in order to deal with a number of challenges facing the economy – both old and new:

- First, the UK must address its poor productivity performance. Productivity growth is the necessary ingredient for longrun sustainable growth, yet productivity fell after the financial crisis and has been flat ever since, and our longstanding gap with countries such as France, Germany and the United States has widened.

- Second, the UK must strive for growth that is equitable, regionally balanced and environmentally sustainable.

- Third, as Brexit becomes a reality, and the UK redefines its international relationships, the government must consider how to mitigate risks to UK trade, international investment and access to international talent, all of which can be expected to have large impacts on UK business.

Here we draw on the recent LSE Growth Commission report (2017) to set out proposals for the key areas of focus for policy-makers developing the inevitable iteration of the UK’s industrial strategy following the general election.

Stop rearranging the deckchairs

The UK’s industrial strategy has long been fragmented and mercurial, with teams in different government departments often working separately, and regular re-branding or changing of business policies. This creates uncertainty for investors.

A case in point is the ‘Growth Accelerator’ programme, which was introduced by the coalition government in 2012 to help small and medium-sized enterprises access coaching and match-funding services. It was scrapped in 2015 with little justification: initial evaluations had found that the Growth Accelerator was viewed positively by businesses and other involved parties, and more robust economic evaluations of the programme were planned.

Lessons can be learned from the frameworks governing UK monetary, fiscal and competition policy (summarised in Table 1), where objectives are defined and enshrined in law, and independent agents play a role in offering advice and, in some cases, taking policy decisions. The remit of such bodies is transparent, with justifications for their advice presented in statutory publications. This creates a more stable framework and promotes open government with external scrutiny by academics, thinktanks and journalists.

Table 1: Examples of UK policy frameworks (click to enlarge)

Source: LSE Growth Commission (2017)

Ending the short-term and opaque system should be the first step. Industrial strategy should be given a new law or long-lasting mandate. And since the existing European Union (EU) state aid framework has blocked arbitrary political intervention in the economy, a new one is needed more than ever when the UK leaves the EU.

A set of transparent rules for intervention is also required, and this should be based on identifying – quantitatively where possible – market failures. Competitive processes should be used wherever feasible to ensure that government support is channelled to its most beneficial use. Ex-post reviews, examining how and why taxpayer funds were used to support industry should be conducted annually.

The ultimate objective is a strategy isolated from political cycles. An independent body of some form would help to achieve this. There is a menu of options to choose from – the Bank of England’s Monetary Policy Committee, and the UK’s independent budget, antitrust and infrastructure bodies. Any one of these would be better than the current ad hoc set up.

To enhance transparency, the government should publish a long-term plan setting shared objectives and aligning decision-makers across government, industry and other stakeholders. The body responsible for industrial strategy should publish a standardised Industrial Strategy Report on the state of UK business each year. This would provide regular material on the productivity of UK firms, with updates on industry- or location-specific policies, together with their costs and measured impacts.

Breaking new ground

The UK needs to invest more in R&D. Both government and business R&D are consistently lower than international comparators as a share of GDP. We know that public R&D spills over to the private sector, and also ‘leverages-in’ private R&D, and there is therefore a strong case for increasing such spending in line with our peers.

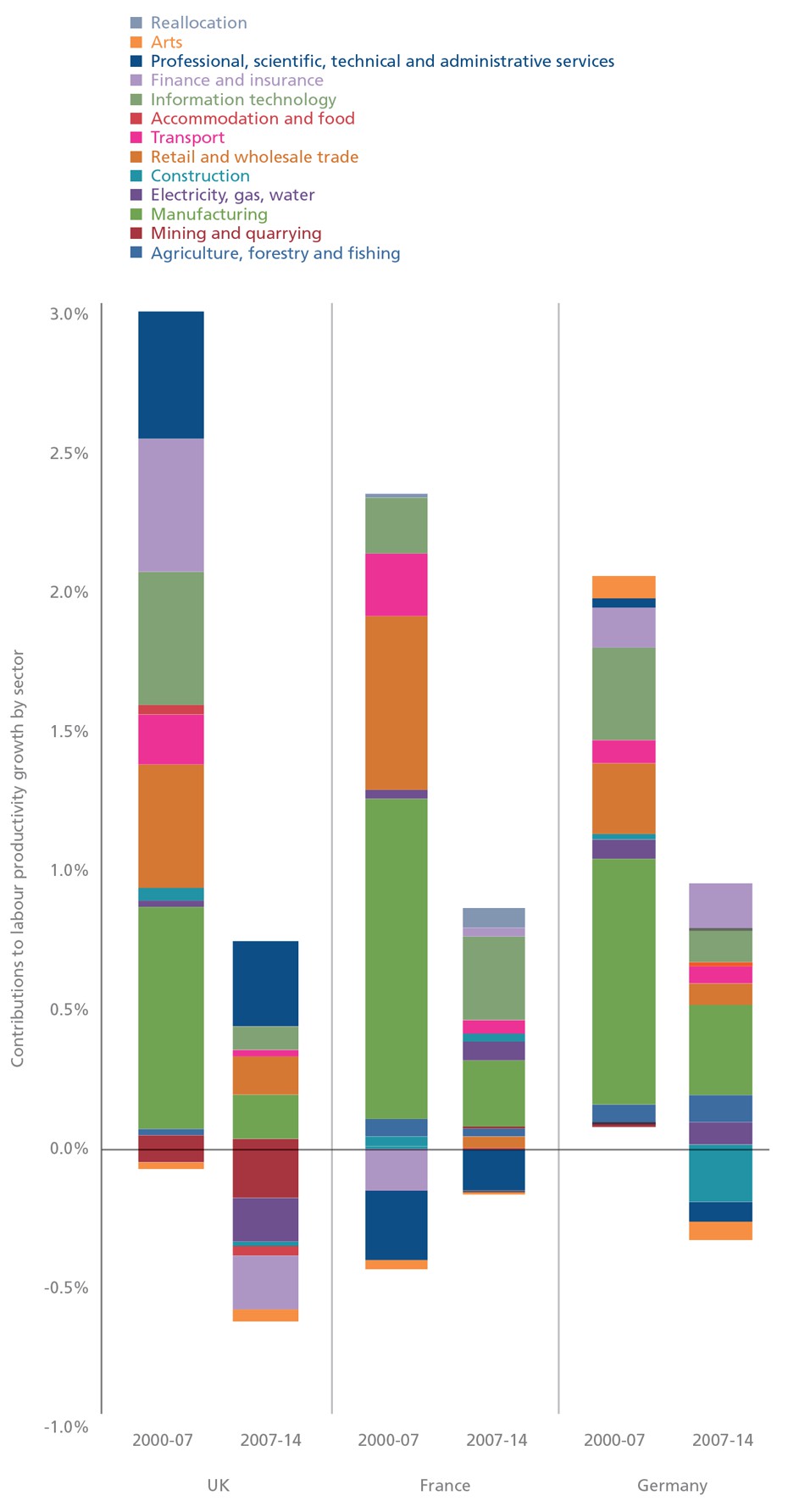

But the importance of research and innovation does not just apply to high-tech sectors like aerospace and pharmaceuticals: the UK is primarily a service economy, and the service sectors have been the main contributors to productivity growth both before and after the financial crisis. As Figure 1 shows, productivity growth in professional, scientific, technical and administrative services has held up relatively well since the crisis – a pattern that differentiates the UK from France and Germany.

While the UK excels in terms of the quality and impact of its research, we lag behind other countries in terms of commercialisation. Compared with the United States, business and universities collaborate far less (Dowling Review, 2015). Government focus to date has been predominantly on the supply side of research (universities). But reviews on this topic in recent years have noted that the demand side – particularly from businesses carrying out R&D – is crucial.

Key to addressing this is improving access to finance for innovative firms, which involves more action to improve competition in the banking sector and measures to stimulate alternative sources of finance (UK firms tend to rely on debt finance, which is less conducive to innovation than equity finance). Lessons can also be learned from ‘patient capital’ funds, which have already been developed by some universities.

Figure 1. Decomposition of labour productivity growth (Gross value added, GVA, per hour)

Policies for sectors

It is important that processes for granting support to particular sectors are competitive, transparent and based on a real understanding of whether there are market failures that the government can usefully address. This can help to avoid policy being influenced by the lobbying of incumbents with outcomes that are not necessarily beneficial for the UK economy as a whole. Strong and transparent institutions governing the UK’s industrial strategy can help to justify the grounds for sector-based support.

Sector support should not be restricted to high-performance/high-growth sectors like aerospace and pharmaceuticals. Low productivity sectors such as retail, hotels and administrative services employ a large share of the population, and suffer significant obstacles to growth (such as the availability of skills or investment in technology) that the government can help to address. Policies that seek to raise productivity in such sectors could have large aggregate effects and also help to reduce inequality.

But it is not always easy to define a sector, and indeed there may be multiple sectors that face common challenges. There is scope therefore for a ‘mission-oriented’ approach, which can help to bring together all relevant companies or technologies across sectors, and be wide-ranging enough to address public policy challenges in areas such as air quality in cities, health and social care.

For example, the early sector deal on the transition to ultra-low emission vehicles mentioned in the recent Green Paper could be part of a wider mission to improve air quality in cities, and extended to include other relevant sectors or technologies, and a number of complementary government levers (such as procurement of low emission bus fleets, and government regulation or incentives to raise consumer demand for these types of vehicle).

Policies for places

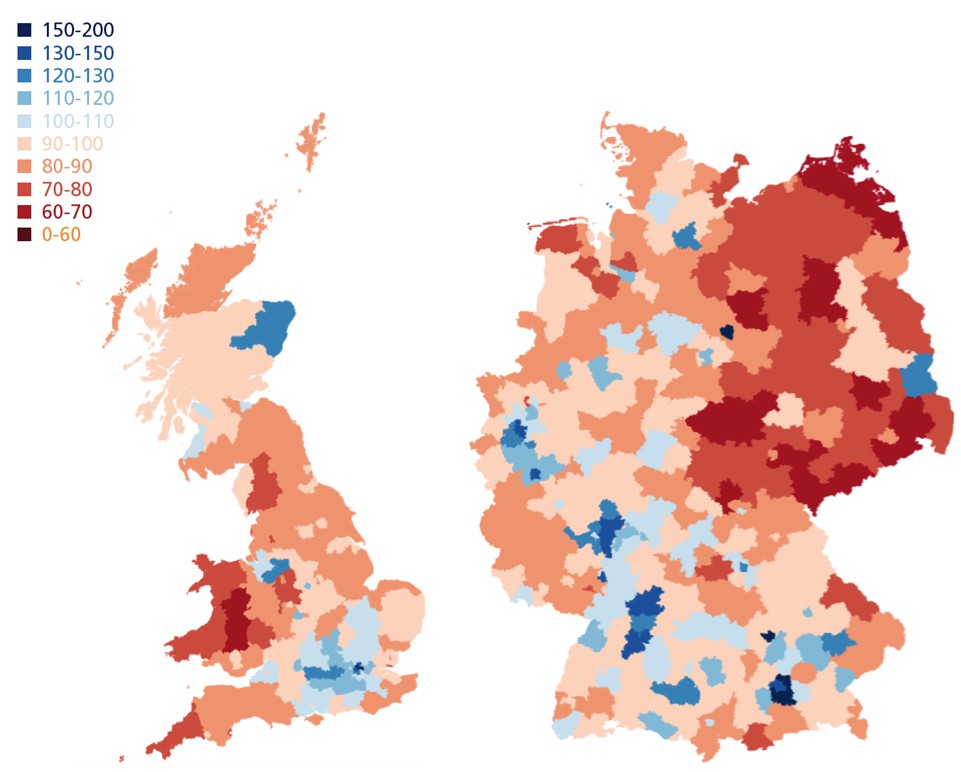

Regional disparities are now wider in the UK than in other West European countries. Figure 2 plots regional productivity relative to the country average for both the UK and Germany. This reveals that the UK’s high productivity regions are highly concentrated, but that there is more spread throughout (mainly Western) Germany. Similarly, the UK is more concentrated at the low end, with Wales standing out as hosting regions with particularly low productivity relative to the UK average.

With the trend towards devolution and the agreement of a number of City Deals over the last few years, a number of important policy levers that can help to deliver an effective industrial strategy – including skills, innovation and infrastructure – are now at the level of nations and regions.

But the current structure of local and regional governance is not well placed to address local challenges. While local enterprise partnerships (LEPs) have the potential to help deliver successful local economic growth strategies, there is some disjointedness between them and local government and it is unclear how they fit into the evolving devolution landscape.

There are also concerns that they lack sufficient resources and the incentives to invest in projects for long-term development. The devolution agenda and regional initiatives will therefore need to be underpinned by a national strategy to deliver policies that are tailored to each part of the UK’s industrial strengths, and the right balance between local initiative and central direction.

Another lever available for improving policies for places is universities’ capacity to improve regional economic performance via their role as producers of skills and incubators of innovation. Once again, there is a coordination problem here, with no formal requirement that LEPs work together with universities. It is crucial therefore to improve engagement between LEPs, local government and universities.

Conclusion

Developing an effective industrial strategy for the UK is no mean feat, not least because it requires the cooperation and coordination of a multitude of stakeholders – particularly across government, business and the education sector. Our starting point is that institutional reform will enable government to take a longer-term view on these issues, based on political consensus, which would not only increase the chances of success, but also reduce policy uncertainty and help stimulate investment across the economy.

Figure 2. Productivity per hour, regions in the UK and Germany compared to national average

Note: The maps show GVA per hour at NUTS3 level in 2014, with the overall country’s level set to 100 (index). Northern Ireland is not on the UK map (as NUTS3 disaggregated data are not available), but the values for the NUTS3 regions within Great Britain are calculated with reference to the UK average (including Northern Ireland). Source: UK data from Office for National Statistics release (January 2017), German data from the federal states’ national accounts.

♣♣♣

Notes:

- This blog post appeared originally at CentrePiece, a magazine of LSE’s Centre for Economic Performance (CEP).

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: London, by MikesPhotos, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Anna Valero is a Research Officer at the CEP, and an Economics PhD candidate at the London School of Economics. Her research is focused on the drivers of productivity and innovation, and in particular how management practices and workforce skills affect the productivity of firms and regions. Anna has been working on the UK productivity challenge, most recently, as a research director for the LSE Growth Commission. Previously, Anna was a manager at Deloitte’s Economic Consulting practice where she specialised in regulatory, competition and strategic economics.

Anna Valero is a Research Officer at the CEP, and an Economics PhD candidate at the London School of Economics. Her research is focused on the drivers of productivity and innovation, and in particular how management practices and workforce skills affect the productivity of firms and regions. Anna has been working on the UK productivity challenge, most recently, as a research director for the LSE Growth Commission. Previously, Anna was a manager at Deloitte’s Economic Consulting practice where she specialised in regulatory, competition and strategic economics.

Richard Davies is Chief of Staff of the LSE Growth Commission, run by the Centre for Economic Performance, and a visiting fellow at University College London. Before this he held various roles in economic policy, research, journalism and the voluntary sector, most recently as Economics Advisor to the Chancellor of the Exchequer, George Osborne, from 2015-2016.

Richard Davies is Chief of Staff of the LSE Growth Commission, run by the Centre for Economic Performance, and a visiting fellow at University College London. Before this he held various roles in economic policy, research, journalism and the voluntary sector, most recently as Economics Advisor to the Chancellor of the Exchequer, George Osborne, from 2015-2016.