Like many other consumer transactions, the buying and selling of drugs are increasingly moving online. This is one very visible dimension of cybercrime – and it has been receiving growing attention from researchers as the online drugs markets have expanded rapidly.

A key feature of online drugs platforms is that they are located on the so-called ‘dark web’, which is accessible via the sophisticated technology of anonymisation software and encryption programs, and buying and selling transactions are conducted using the anonymous cryptocurrency, Bitcoin.

Our research so far has empirically studied these online drugs platforms by scraping large amounts of data from their websites and by focusing specifically on three economic questions:

- First, we have conducted an appraisal and empirical analysis of the buyer ratings of online drugs purchases that the platforms collect.

- Second, we are looking at whether these ratings act to generate a reputation mechanism for sellers in the illegal online market setting as happens in legal online markets.

- Third, we are analysing the dynamics of the market, as both seller turnover and platform turnover are high in online drugs markets.

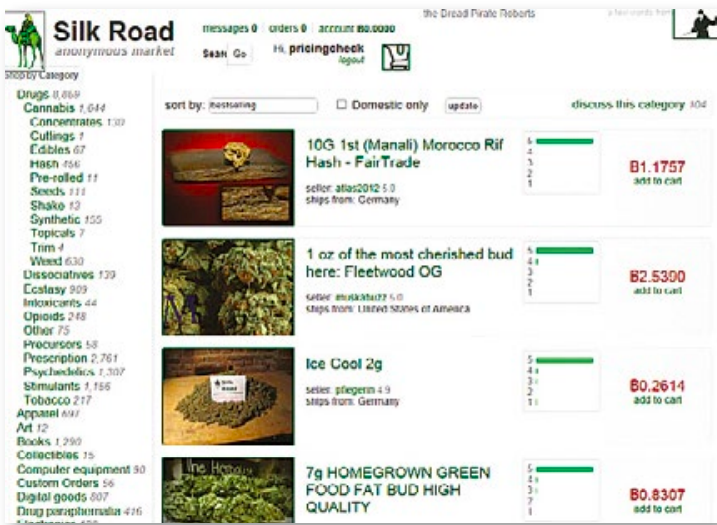

While there is a small scale prior history of drugs being bought and sold online, the origins of today’s online drugs markets date back to the establishment of ‘Silk Road’, the best known platform, in January 2011. Silk Road distinguished itself from the black markets that had been operating before by its highly professional website and its ability to ensure anonymity. Figure 1 shows a sample screenshot of the site.

Figure 1. Sample screenshot of Silk Road, the pioneering online drugs platform

Silk Road operated for just under three years before being shut down following the arrest of its founder, Ross Ulbricht, the libertarian who set up and ran the site (under the administrator name, ‘Dread Pirate Roberts’) and who is currently serving a life sentence for doing so. Trade on the site grew massively over its time of operation: in May 2011, it had around 340 listings; by the time of its closure in October 2013, there were around 13,000 drugs listings on the platform.

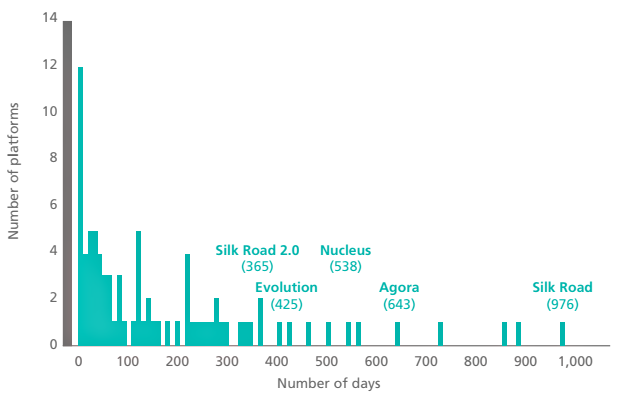

Figure 2. Lifetimes of 83 online drugs platforms

Since the demise of Silk Road, a large number of online drugs platforms have come and gone, some lasting only a few days, but others running longer – and making a lot of money. Figure 2 shows the lifetimes of 83 dark web drugs platforms and names some of the larger sites.

For our research, data were scraped from four of the largest online drugs platforms – Agora, Evolution, Nucleus and Silk Road 2.0 – between 2013 and 2016 and then analysed to present evidence on the economic functioning of online drugs markets.

A key research question is how well – or badly – these markets operate given the high probability of problems of ‘moral hazard’ arising because of their illegal nature and because they are populated by individuals engaged in criminal actions. Some of the findings come from analysing these data in ways similar to other research on legal online markets, such as eBay or Amazon, where there is a focus on whether online activity alters the way in which trust between market participants operates and whether it affects the efficiency of outcomes.

A particular emphasis has been placed on whether online activity enhances or diminishes seller reputations so that problems of moral hazard either improve or deteriorate in the context of online commerce (see Cabral and Hortaçsu, 2010). Buyers might be concerned about the quality of the products they are looking to buy and therefore forgo purchasing opportunities. At the same time, sellers might worry whether they will be paid.

Some striking findings emerge.

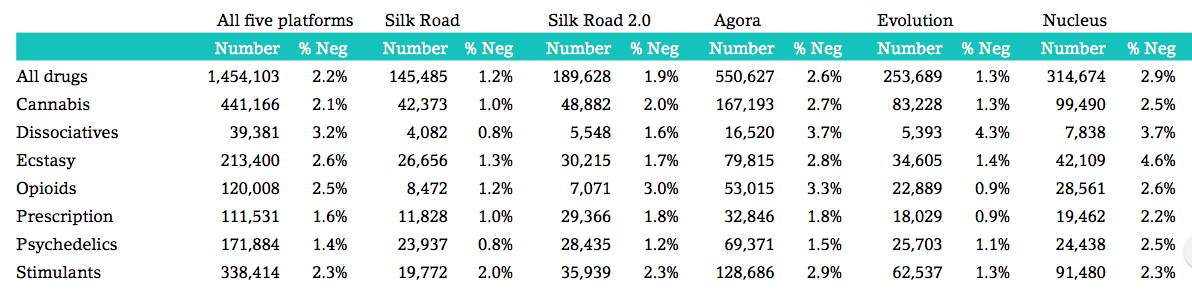

Analysis of around 1.5 million drugs transactions scraped from the four platforms (plus data on Silk Road from Christin, 2012) shows that, for the most part, online drugs markets function without the significant problems of moral hazard that a priori one might think would constrain their operation.

In fact, only a small minority of online drugs deals receive bad ratings from buyers, as Table 1 shows. This is lower than the incidence of drugs rip-offs that researchers have reported in analyses of the quality of drugs available from street transactions (Galenianos et al, 2012).

Moreover, as with legal online markets, if sellers do receive bad ratings, this typically leads to them experiencing significant sales reductions and market exit. Thus, perhaps contrary to what many people’s first intuition might be, reputation mechanisms appear to work relatively well even in these illegal online marketplaces.

Our research also finds that drugs platforms exit and get closed down for different reasons. As the online drugs markets have emerged and grown rapidly, they have attracted attention from both the media and law enforcement agencies.

Table 1. Negative ratings of drugs transactions

Notes: Silk Road data from Christin (2012). Silk Road 2.0, Agora, Evolution and Nucleus data from downloads of each dark web platform collected in Bhaskar et al (2017).

As a result, some have been seized and shut down. Others have undertaken exit scams and run off with the money they were holding (in Bitcoins often running into millions of pounds). Thus, the market has become characterised by platform (and seller) entry and exit. It is interesting to consider whether this has had a deterrent effect on potential buyers and sellers.

An examination of what happens to the online drugs market when large platforms exit suggests no evidence of deterrence. In fact, the markets seem to bounce back rapidly and get bigger as sellers migrate quickly to different sites and continue to ply their trade online.

Our research has looked at three specific cases: the well-known seizure of the original Silk Road; the shutdown of its successor Silk Road 2.0 by law enforcement agencies; and the exit scam by the then market leader, Evolution. There is no evidence that these large scale exits deterred buyers or sellers from continuing to engage in online drugs sales and purchases, with new platforms rapidly arising to replace those taken down.

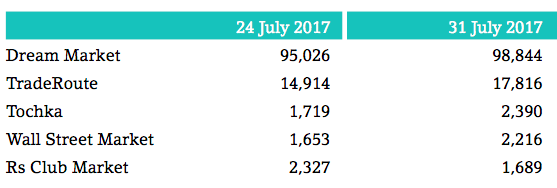

Very recently – in July 2017 – the then market leader AlphaBay was taken down, along with another relatively large platform, Hansa. But again, despite widespread media coverage, this also seems not to have reduced sellers’ appetite for selling drugs online as new sites rapidly expanded in terms of drugs listings following the shutdown. Table 2 reproduces data showing this for four out of five platforms in the week at the end of July 2017 after AlphaBay and Hansa were seized.

So despite high turnover of the platforms that host the buyers and sellers of drugs, the online drugs market seems resilient. As with legal online markets, illegal online markets are substituting for offline economic activity (street transactions in the case of drugs) as buyers and sellers increasingly operate online: a trend that seems unlikely to end any time soon. Thus, it seems that the role of law enforcement in the ‘war on drugs’ may need to be one of devoting more resources and finding better means to tackle drug buying and selling in the cyber domain.

Table 2. Numbers of drug listings before and after the shutdown of AlphaBay and Hansa

Notes: Numbers from Cyberint research, as reported on BBC website, 1 August 2017.

♣♣♣

Notes:

- Robin Linacre contributed to this work in a personal capacity and in his own time. The opinions expressed are the authors’ own, and the research is not linked to any of Robin Linacre’s work for the Ministry of Justice.

- This blog post appeared originally on CentrePiece, the magazine of LSE’s Centre for Economic Performance. It summarises the authors’ The Economic Functioning of Online Drugs Markets, CEP Discussion Paper No. 1490; forthcoming in the Journal of Economic Behaviour and Organisation.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Spider web, by Jyrki Salmi, under a CC-BY-NC-SA-2.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

V Bhaskar is at the University of Texas at Austin.

V Bhaskar is at the University of Texas at Austin.

Robin Linacre is at the UK Ministry of Justice

Robin Linacre is at the UK Ministry of Justice

Stephen Machin is Professor of Economics at LSE and Director of the School’s Centre for Economic Performance (CEP). His expertise is in labour market inequality, economics of education and economics of crime.

Stephen Machin is Professor of Economics at LSE and Director of the School’s Centre for Economic Performance (CEP). His expertise is in labour market inequality, economics of education and economics of crime.