An article by Kathleen Kahle and René M. Stulz on LSE Business Review analyses the shrinking number of public corporations in the US. We find this phenomenon also in Germany. In our study, we find a decline in the number of listed companies in Germany driven by a decline in initial public offerings (IPOs) and an increase in delistings:

- While in the period 1991-1995 IPOs contributed to an increase in the number of public companies by 2.5 per cent per year, they only contributed to a growth of 1.9 per cent per year in the period 2010-2016.

- Delistings contributed only to a 1.3 per cent decline in public companies over the period 1991-1995, while delistings soared later on and contributed to a decline of 6.4 per cent over the period 2010-2016.

We find that there is no single driving force behind these developments, but several drivers, which we analyse hereafter.

Decline in start-up activity

Young high-growth companies from high technology industries, also known as start-ups, form the pool of candidates for an IPO. These innovative start-ups need to pre-finance their high initial investments and in later stages their growth, but they lack the sufficient collateral for debt financing. Instead, they have to rely on equity financing, often in the form of venture capital.

Venture capitalists often exit their investments in companies through an IPO. Part of the declining number of IPOs in Germany is due to the declining start-up activity. Start-up activity in Germany has been characterised by declining numbers since 2005. While more than half a million new enterprises per year were born 12 years ago, in 2016 the yearly number of new enterprises dropped to only just under 300,000.

Company acquisitions by private equity investors

According to a hypothesis by Elisabeth de Fontenay, the growth of private equity firms has contributed to the decline in initial public offerings and the rise of delistings, because private capital acts as a substitute to shareholders’ capital, but in a less regulated environment with lower compliance costs. With the rise of private equity, there is an attractive alternative to a public listing and thus to an IPO.

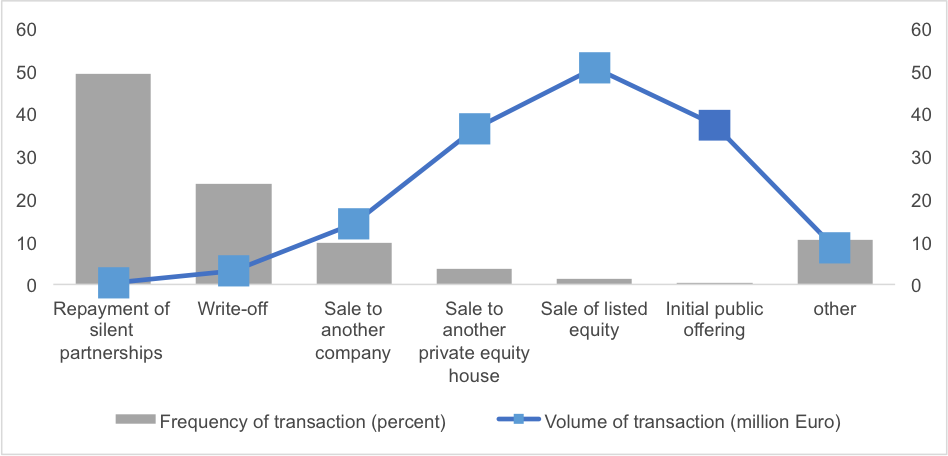

Figure 1: Exit Strategies of Private Equity Investors in Germany

Source: Invest Europe, own calculations

In our study, we find that private equity companies in most cases do not exit via IPOs from their successful investments, but often sell the companies to other companies or to other private equity firms (figure 1). While the data analysis shows that IPO and post-IPO sales are more often used in cases of larger transaction volumes, selling the company to another company is more likely to be chosen for smaller transactions. However, it is of interest to our analysis that the sale of a company to another private equity firm is also chosen for larger transactions comparable to the transaction size of an IPO. This would support the hypothesis that selling a start-up company to a private equity firm is a viable alternative to an IPO.

A shortage of stock investors

The fact that companies prefer selling their shares to another private equity firm to an IPO may also be due to a shortage of corresponding investors in the stock market. The first investor type that withdrew from the stock market was households, which held listed equities worth 11.8 percent of GDP in 2000 and reduced their holdings to currently 8.7 percent of GDP. Banks, insurance companies and investment funds in Germany have reduced their holdings of listed shares, too. Their holdings dropped from 36.4 per cent of GDP in 2000 to currently 15.2 per cent of GDP. At the same time, they have become more involved in other equity investments, e.g. unlisted shares and other equity investments. Their holdings of unquoted shares and private equity rose from 8.5 percent of GDP to 12.6 percent of GDP over the same period (figure 2).

A similar trend is evident for non-financial companies’ asset holdings. These companies have reduced their holdings of listed shares from 31.2 per cent of GDP in 2000 to currently 11.1 per cent of GDP (figure 2). Over the same period, they have increased their holdings of unlisted shares and other equity investments from 27.6 per cent of GDP to 46.8 per cent of GDP. The increase of the other forms of business ownership is likely due to a strategic realignment. In times when knowledge is becoming increasingly important, companies want to gain the knowledge of other companies by buying the entire company. While they have to compete with other bidders for shares of the company on the stock market, they can more easily buy the entire company outside the stock market. Since the younger technology companies are often less capital-intensive, buying a whole company is easier to handle.

Figure 2. Holdings of listed shares and unlisted shares in Germany

Souce: Eurostat, own calculations

Conclusions

From our analysis we conclude that reviving IPOs and stock market participation is desirable. One reason is that stock markets generate important public data about corporate values. In addition, large stock market segments enable investors to diversify their risks. For growing companies, the stock market potentially represents an important source of funding, especially when private equity capital might be less abundant as now. The fact that banks and insurance companies have withdrawn from equity investment seems to be an undesirable side effect of rising financial regulation.

A higher household participation in the stock market is also important, since stock investments are particularly suitable for long-term investments as part of old-age provisions, especially in times of low interest rates. Promoting financial literacy among households might be an important policy task here. Last, but not least, fostering start-up activity will have the positive side effect that the pool for candidates for IPOs will increase again.

Article mentioned:

♣♣♣

Notes:

- This blog post is based on the authors’ study (in German) Unternehmensfinanzierung: Was sind die Gründe für die rückläufigen Börsengänge?

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Deutsche Börse-8262, by Bankenverband – Bundesverband deutscher Banken, Public Domain.

- When you leave a comment, you’re agreeing to our Comment Policy.

Markus Demary is senior economist in the research unit financial and real estate markets at the Cologne Institute for Economic Research (Institut der deutschen Wirtschaft Köln). He studied economics at the Rheinische Friedrich-Wilhelms-Universität Bonn and he holds a doctoral degree from the Christian-Albrechts-Universität zu Kiel. He is also a lecturer in Behavioural Finance at Ulm University.

Markus Demary is senior economist in the research unit financial and real estate markets at the Cologne Institute for Economic Research (Institut der deutschen Wirtschaft Köln). He studied economics at the Rheinische Friedrich-Wilhelms-Universität Bonn and he holds a doctoral degree from the Christian-Albrechts-Universität zu Kiel. He is also a lecturer in Behavioural Finance at Ulm University.

Klaus-Heiner Röhl is a researcher at the Institute for Economic Research in Berlin, and a senior economist in the research unit “Structural Change and Competition”. His research focuses on small and medium enterprises (SME); entrepreneurship and start-ups; business regulation and administrative burden; and regional economics.

Klaus-Heiner Röhl is a researcher at the Institute for Economic Research in Berlin, and a senior economist in the research unit “Structural Change and Competition”. His research focuses on small and medium enterprises (SME); entrepreneurship and start-ups; business regulation and administrative burden; and regional economics.