Blockchain and its associated technologies burst into the public consciousness in 2015 after a relatively slow build-up spanning several years. In the course of 2017 blockchain became one of the most hyped technologies ever and has found a particularly keen audience in the banking world due to the promise of greater efficiency, or in other words, cost.

Banks globally have been testing the blockchain technology for some time now, either to implement in their core banking system or integrate into their traditional systems. Currently, there is a discussion around blockchain moving beyond the initial excitement of ‘blockchain will fix everything’ to a clearer and more considered view of its most appropriate use cases.

The need of the hour is to focus on domains where the legal, regulatory, or political environments hinder the establishment of a central controlling authority such as in the online world. Blockchain has the potential to provide a universally distributed system that can be used by several retail banks to share transactions or record keeping with each other, negating the need for a central authority of the internet.

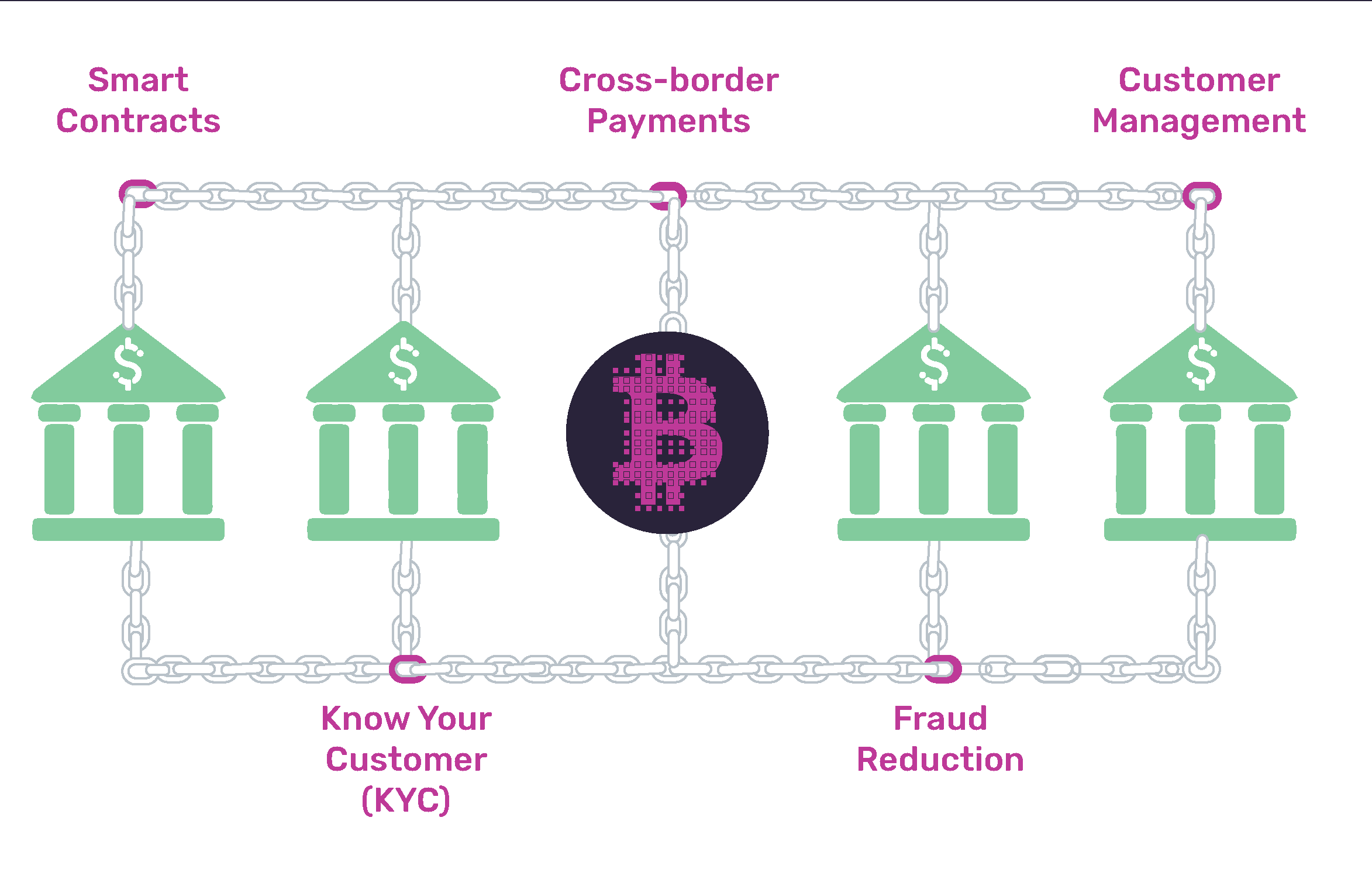

One of the most promising applications of the blockchain technology is the smart contract. It enforces the obligations of all parties in a contract, without the added expense of a middleman. In the case of complex processes such as mortgages, elements of the analogue process could be automated via smart contracts. For example, creating shared copies of legal agreements and full electronic audit trails, would expedite the release of funds, and reduce the time from contract exchange to completion. Banco Santander is piloting use cases around precisely this.

Banks spend millions of dollars annually to keep up with Know-Your-Customer (anti money laundering regulation) and customer due diligence requirements. A blockchain allows the independent verification of one client by one organisation to be accessed by another organisation so the KYC process wouldn’t have to start over again, which in turn reduces the cost burden on banks. The reduction in administrative costs for compliance departments would be significant. Dozens of start-ups are working on building blockchain systems for customer identification, including KYC Chain, Cambridge Blockchain, Tradle, Credits and Blockstack.

The transfer of value is an expensive and slow process, especially for cross-border payments. Currently, cross-border payments cost ten times more than domestic ones. In the UK alone there is scope to realise annual savings of over £600 million. If a customer wants to transfer money from France to their family in the Gambia, for example, it takes a number of different banks (and currencies) before the money can be collected. Blockchain can speed up and simplify the process, cutting out many of the traditional middlemen, while significantly reducing the costs (certainly as compared to a service such as Western Union). Beyond this, and more fundamentally, the more seamless global and domestic payment mechanisms are, the more households and businesses will benefit from the global economy.

As most banking systems are built on a centralised database, they have one point of failure rather than many, making them more vulnerable. Blockchain’s distributed ledger would eliminate some of the current crimes being perpetrated online, as it stores, encrypts, and verifies every single bit of data in a transaction. In the event of a breach or fraudulent activity, it would be made immediately obvious to all parties that have permission to access the transaction data on that ledger.

Finally, the transparency and traceability of blockchain technology can improve the effectiveness of loyalty and rewards schemes as part of performance management systems. After all, employee sentiment and use will only improve if rewards are actually delivered and companies and their employees can agree on whether a certain transaction has taken place.

Regulators across the world, especially in the financial services sector, are expected to scrutinise blockchain technologies thoroughly throughout 2018 and into 2019. Indeed the Bank of England announced in June that they will rebuild its Real Time Gross Settlement system so that it can interface with private businesses and platforms using the blockchain. However, blockchain is still three to five years away from commercial feasibility, primarily because of the difficulty to establish common standards. In the long term, the strategic value of blockchain will only be realised if cooperation among multiple players is achieved at scale.

Figure 1. Five prime use cases of blockchain in retail banking

Source: GlobalData Disruptor tech database

♣♣♣

Notes:

- The post gives the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Photo by Alexshorter, under a CC-BY-SA-4.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Kit Carson is head of banking and fintech at GlobalData. He is passionate about the consumer and champions innovative approaches to the provision of financial services. Prior to joining GlobalData in 2014, Kit spent 10 years working directly with customers and in head-office environments within the UK financial services sector.

Kit Carson is head of banking and fintech at GlobalData. He is passionate about the consumer and champions innovative approaches to the provision of financial services. Prior to joining GlobalData in 2014, Kit spent 10 years working directly with customers and in head-office environments within the UK financial services sector.