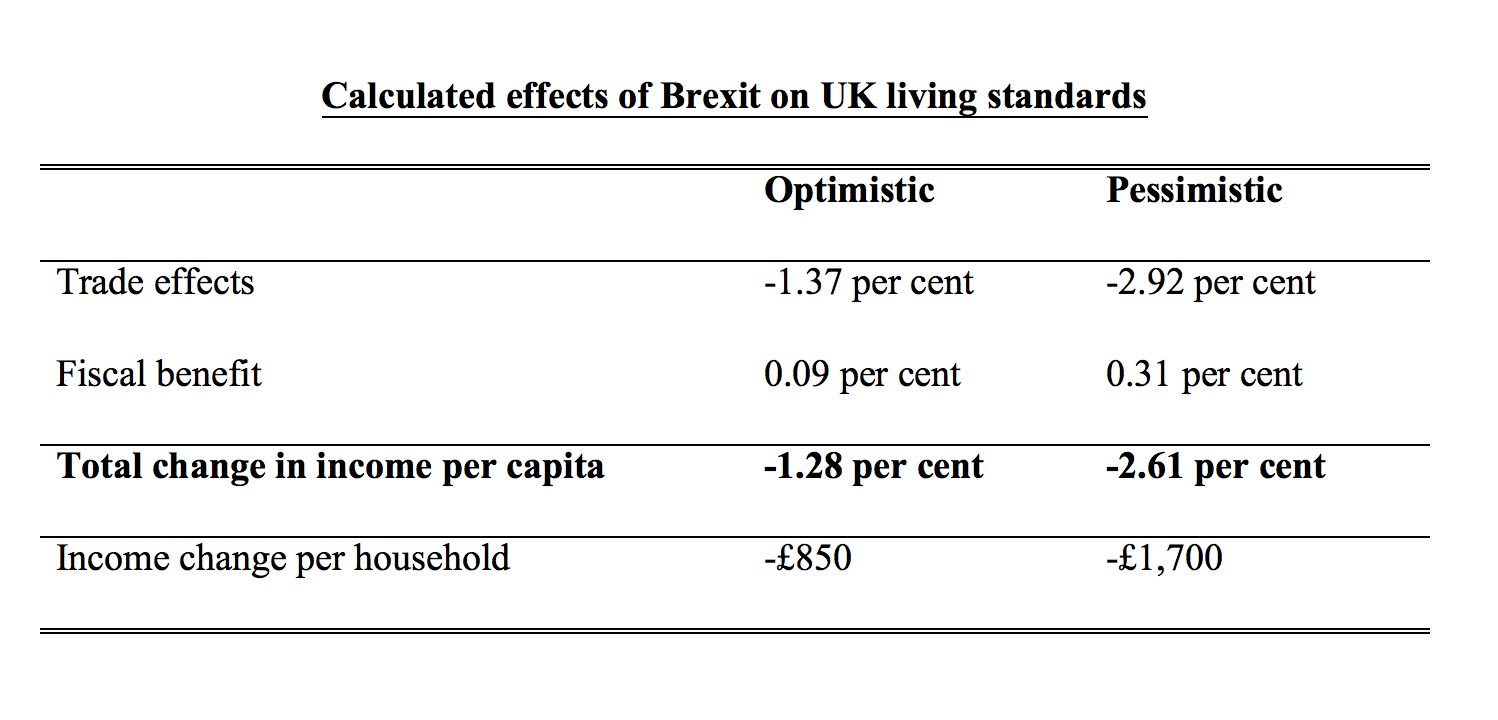

For over two years, a research team at the Centre for Economic Performance (CEP) has been studying the likely impact of the UK leaving the European Union. Their latest report focuses on the impact of ‘Brexit’ through changing trade patterns. Under ‘optimistic’ assumptions, there is a fall in national income of 1.3 per cent (about £850 per household). Under ‘pessimistic’ assumptions, this doubles to 2.6 per cent. When the dynamic effects of higher trade costs on productivity are included, the cost may rise to between 6.3 per cent and 9.5 per cent in the long run.

There are many issues that will weigh in the minds of voters in the run up to the 23rd June EU referendum. Many people feel that they are oppressed by a remote, undemocratic super-state that can over-rule British laws. Others believe that the EU promotes better co-operation between communities that were at war for centuries. These views often stem from deeply held political and moral beliefs.

Economics can make a small contribution to the debate by considering what might be the material costs and benefits of leaving the EU. If there are economic benefits, then for Eurosceptics it’s a win-win. On the other hand, if there are economic costs to Brexit, then even a die-hard Leaver must consider whether the price is too high. Some might be prepared to pay any cost, for them it is ‘death before enslavement’. To most people however, it’s not so all-or-nothing. They will look at the likely costs and benefits, and this will help inform their decision.

Figuring out the economic costs and benefits of Brexit

An obvious benefit of Brexit is that the UK will not have to send so much money to Brussels. On net this is around 0.31 per cent of our national income. An equally obvious cost of Brexit is that trade between the UK and EU will be lower if the UK leaves than if it stays. The degree to which trade costs will be higher outside the EU is a big question. But it’s a fact that even when countries have comprehensive trade deals (such as Norway’s deal in the European Economic Area, EEA) there are still non-tariff barriers due to regulatory differences, border checks, rule-of-origin requirements and anti-dumping actions. This is why even Norway has been found to have less trade with the EU than would be expected from such a deep level of integration.

There are a rich menu of economic models to analyse the impact of trade arrangements, but it turns out that most of them have a pretty similar structure when it comes to thinking about welfare gains. Our work develops a state-of-the-art (but bog-standard) trade model plus industry-level data on exports and imports covering all sectors of the economy in every country in the world. This, plus an estimate of how trade responds to costs, enables us to figure out how trade patterns and living standards will change when trade costs (tariff and non-tariff barriers) change after Brexit.

Since it is hard to know precisely how trade costs will change after Brexit, we look at two stark scenarios. An ‘optimistic’ scenario is that the UK swiftly strikes a deal so that it gets deep access to the EU single market, like Norway. A ‘pessimistic’ scenario is that the UK is unwilling to accept the free movement of labour and the associated regulations that are part of the ‘access price’ to the single market and so will prefer the usual EU external tariffs. Trade will fall by more in this case.

The table shows the results of our analysis. There is a drop in income per person of 1.3 per cent in the optimistic case, which doubles to 2.6 per cent in the pessimistic case. This translates to a fall of between £850 and £1,700 per UK household.

Source: CEP calculations (Technical details available here). Income based on allocating GDP loss per household. For example, 1.3 per cent of UK GDP is £23 billion and there are about 27 million households.

Source: CEP calculations (Technical details available here). Income based on allocating GDP loss per household. For example, 1.3 per cent of UK GDP is £23 billion and there are about 27 million households.

Is the pessimistic scenario too optimistic? Probably yes

The calculations we make are very narrow. They assume away any positive effects that trade may have on productivity through more competition, innovation, foreign investment and migration. We also abstract away from the economic damage induced by the policy uncertainty in the very difficult negotiating period following a Brexit vote. Negotiations over new trade agreements could stretch over many years.

An alternative ‘back of the envelope’ way to estimate the effects of Brexit is to look at what actually happens when countries joined the EU compared with being in free trade areas like the European Free Trade Area or EEA. The trade effects are big – a jump of a quarter or more. Combining this with estimates of the impact of trade on GDP from real falls in trade costs leads to an implied fall of UK national income of between 6.3 per cent and 9.5 per cent. Interestingly, this is squarely within the range of values that others have estimated have been the historical benefits of the UK joining the EU of around 8 per cent to 10 per cent.

This tripling of the costs of trade loss are also consistent with the literature of economic research comparing the actual benefits of trade liberalisation (big) with those predicted from static models like those presented here (much smaller). Naturally, UK trade with the EU does not disappear in any scenario – there remains a ‘trade deal’ in all cases. It is simply that there is less than it would have been had the UK remained a member.

It makes little sense to point to a decline in the EU’s share of total UK trade over the last decade as evidence that the single market has ‘failed to reduce trade costs.’ This decade has witnessed the rapid growth of Asian trade powerhouses as well as the worst global economic crisis since the Great Depression. Britain’s trade with Europe has increased since 2000, it’s just that trade with China has increased much faster.

Is the optimistic case too pessimistic?

How could things turn out better? First, could the UK negotiate a sweetheart deal much better than Norway or Switzerland have managed? This seems unlikely. About half of the UK’s exports go to the EU,whereas only 10 per cent of the EU’s exports are destined for the UK, so the bargaining power is lopsided. What’s more, the EU will not want to be seen to be offering generous rewards for leaving as this will encourage other members to try the same trick. And in addition, all this assumes that everyone is behaving reasonably and rationally – unfortunately divorces tend to be much messier. Kicking the EU when it is undergoing a major refugee crisis and a long-running monetary crisis might provoke some very grumpy outcomes.

Second, could the UK strike better trade deals with non-EU countries like the United States, China and India than with the EU? Although the UK will not have to compromise with other EU members when doing such deals, it cannot offer access to the biggest single market in the world as the EU does (UK GDP is under a fifth of the size of the single market). The EU is in the final stages of negotiation with the United States and Japan on deals estimated to raise GDP by 0.6 per cent. If the UK cannot replicate these deals (and the United States has stated it is not interested in a UK-only deal), this will be a further income loss on top of the estimates here.

Finally, what about the promised bonfire of red-tape when we leave the EU? Being outside the EU would enable the UK in principle to jettison some irritating regulations. But it’s worth bearing in mind that being in the EU has not stopped the UK from having one of the most flexible product and labour markets in the OECD (behind only the United States and sometimes Canada).

The real question is whether much better regulation will really be forthcoming after Brexit. We often hear by Eurosceptics that “the 100 most burdensome EU regulations have been estimated to impose annual costs of £33.3 billion”. But what they neglect to mention is that the government impact assessments they cite also estimate that the same 100 regulations bring benefits to Britain of £58.6 billion per year! It’s been argued that by getting rid only of those regulations where costs are deemed to outweigh benefits, 0.9 per cent of GDP could be saved. About half of this is estimated to come from the Renewable Energy Strategy and the Working Time Directive. It’s unclear that tearing up these environmental and employment protections will be politically feasible or really as economically beneficial in the long run as the impact assessments find.

Is Brexit a price worth paying?

Many people may decide that knocking a grand or two off their salary or pension is worthwhile to get Brussels off their backs. Some – though probably fewer – might even say the same if the bill rises to over £6,000 a year. These are reasonable positions and every voter will make up their own mind over the price they are willing to pay. But those who say that leaving the EU is a win-win because Britons will both feel more free and become a lot richer are not being candid about the evidence. The standard trade models given here, calculations from trade and income differences of being in and out of the EU and also historical assessments show a consistent picture – Brexit will cost. The only question is ‘exactly how much’?

Authors’ note: The piece summarises the study ‘The consequences of Brexit for UK trade and living standards’. The report has been attacked by Vote Leave. First, they say the report is EU funded. This is untrue: our work is funded by the UK’s Economic and Social Research Council (as a whole, CEP receives less than 5 per cent of its funding from the EU). Second, they say the authors lack credibility because we also supported euro entry. This too is untrue: Professor John Van Reenen, who has been CEP Director since 2003, has never supported the UK joining the euro. Vote Leave’s other points were all addressed by the original report and are amplified in the above piece

Please read our comments policy before commenting.

Note: This article was originally posted at LSE British Politics and Policy and it gives the views of the authors, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics. Featured image via youtube

Shortened URL for this post: http://bit.ly/1RcY4j8

_________________________________

Swati Dhingra – LSE

Swati Dhingra is a Lecturer in Economics at the LSE.

–

Gianmarco Ottaviano – LSE

Gianmarco Ottaviano – LSE

Gianmarco Ottaviano is Professor of Economics at the LSE.

–

Thomas Sampson – LSE

Thomas Sampson – LSE

Thomas Sampson is an Assistant Professor in Economics at the LSE.

–

John Van Reenen – LSE

John Van Reenen – LSE

John Van Reenen is Professor of Economics at the LSE and Director of the CEP.

Since the UK only has small amounts of representation in the EU relative to the whole, with maybe 14-16% of the population, only 8% representation in the commission, and is not part of the Eurozone, its negotiating clout within the EU with regards to external trade negotiations is extremely limited as a share of the increased negotiating clout of the EU as a whole. The improved clout of the whole EU unit is improved by having more members, but the benefits to the individual states are severely limited by the internal horse-trading, which favors the Eurozone countries. By the same argument about negotiating power, the UK will be overpowered internally by Eurozone countries.

Also, trade only makes up 28.4% of the UK economy, and export to the EU is itself only about 30% of all export. However, import from the EU makes up a larger share of UK GDP, and the initial fall in trade would lead to both falling imports and exports as well as a reorientation of the UK toward domestic consumption of goods and services. Moreover, the fall in the value of sterling and the fall in food prices (due to abandoning the CAP) would stimulate exports and actually lower total import amounts as the UK seeks the most efficient manufacturers of food.

It’s also definitely not safe to assume that there would be a decline in productivity, since one of the primary sources of low productivity increases is the availability of cheap labour. Businesses that encounter dear labour will be more likely to invest in labour-saving capital, that is, capital that improves productivity of workers.

Your report doesn’t include any of its math, and it’s definitely not clear that the dynamic effects stack up in the way you state.

“Since the UK only has small amounts of representation in the EU relative to the whole, with maybe 14-16% of the population, only 8% representation in the commission, and is not part of the Eurozone, its negotiating clout within the EU with regards to external trade negotiations is extremely limited as a share of the increased negotiating clout of the EU as a whole.”

This line (about the percentage of representation the UK enjoys) is repeated constantly by UKIP in particular, but it’s entirely illogical. Using your argument we’d be obliged to conclude that no state has any influence in the EU given each state only has one Commissioner and only France and Germany have (marginally) more representation in the Parliament/Council. That’s an absurd line of reasoning and is indicative of the kind of soundbite-oriented attempts at analysis that pass for an argument in the UK’s debate.

We have plenty of actual evidence on the UK’s influence in the EU – voting records, countless studies. The evidence is fairly mixed with some studies finding the UK exerts a very large degree of influence and others finding it exerts more limited influence in particular areas. I suggest it would be better to consult this evidence rather than merely pointing at the percentage of the UK’s population (for the record, 1 out of 28 is about 3.6%, not 8%).

Functionaries of the commission, that is, EU civil servants, not commissioners. Moreover, if you read the sources in the report and the course-notes I linked, you will find that groups usually act in the interests of the strongest players within the group. Therefore, the Eurozone acts in the interests of Germany, and the EU acts in the interests of the Eurozone. Because the UK is not in the Eurozone, it cannot compete for dominance on an equal footing with Germany.

Moreover, your entire argument is based on the result of Feyrer, used in a naive and silly way.

I suggest you take a look at these course notes: http://ocw.mit.edu/courses/economics/14-03-microeconomic-theory-and-public-policy-fall-2010/lecture-notes/MIT14_03F10_lec12.pdf

I would imagine most people here are familiar with Feyrer’s study, but I fail to see how this constitutes a “naive and silly” use of his work and your link certainly doesn’t prove that case. In fact that strikes me as a fairly reactionary attempt to dismiss some research on the grounds that you don’t like the conclusion.

What we’re talking about here is how you quantify a drop in trade in terms of the effect on per capita income. There’s no magic formula and quoting Feyrer is a fairly standard way to address this problem – if you have a better way to do so then please post it, but all you’ve essentially posted here is a qualifier.

The problem with Feyrer’s result is not that it predicts that higher trade leads to higher GDP/capita, something expected because of comparitive advantage, but that it was used foolishly as a simple factor (0.7), as though the actual estimate were certain and accurate. Moreover, the paper did not consider several factors, namely that Britain has a persistent current account deficit with the rest of the EU, nor that much of the trade between Britain and the EU would be diverted back to the most efficient producers, since Community Preference by its very nature is intended to divert trade.

Feyrer’s result holds in cases of close-to-balanced trade, but its effects could be swamped by a return to balanced trade, given Britain’s persistent current account deficit.

For an example, consider that Italy’s productivity growth was higher before it joined the Eurozone, which led to large current account deficits driven by large capital inflows and resulting in large divergences in competitiveness (unit labour costs) between the core and periphery in the Eurozone.

Harry. Well done for holding them to account. This was clearly a biased article.

@harry

you are spouting gibberish as if they were common sense economics

adding isolated (and in your case, often wrong) “facts” doesn’t mean correlation …nor do they make sense per themseleves

I understand that the UKIP textbook is for dummies : delusions trump over realities

but at some point, any adult with half a brain should be able to realize when they are spouting nonsense for no other reasons than to flatter their ego “that they were right all along”

1) democratic proportional representation is exactly what it means : you have an amount of vote equal to your number of voting eligible population

the UK is around 12% of the E’s population, so it has around 12% of the voting share when it comes to EU council votes or MEPs number

that’s no conspiracy and means that to advance your own narrow interest means that you must build coalitions and strike compromise : that’s life !!

only in the UK would one find normal that a party with the support of less than 30% of the voting eligible population is able to own a majority of the lower chamber and have a free-ride in autocraticaly running the country (and now the same is true with proto-fascist Poland’s case, but at least there, the people have realized the illiberal nature of their government)

2) the EU Commission is a civil service.

does Whitehall have a share of how many Scots or Welsh must be recruited because they respectively form 8% and 5% of the UK population ?

in addition, the Commission works at the behest of the EU Council and the EU parliament : they never initiate or propose legislation without their input

3) the EU absorbs a bit less than 50% of the UK’s export (a bit less of 40% in goods and around 55% in services)

but this doesn’t reflect the dynamic nature of trade, since it permeates the whole activity of the country allowing domestic-only firms to have any business at all

let’s take an example : a foreign plant in the UK may import industrial goods from other countries, as part of its logistical chain and export the final product elsewhere

any disruption in those “imports” may not automatically lead to a switch to domestic suppliers (either because they are not as price-efficient or do not have the technological/capacity know-how), and instead is forced to slim-down its operations in the UK

when a firm has a customer that represents 10% of its turnover, it’s an important one

when the customer is 30%+, it’s called a lifeline : you keep working with it or go under

add to this the impact to the purely domestic economy : the plant will provide business to domestic suppliers of goods and services, but the employees of that foreign firm in the UK will also generate paid taxes and business to other local businesses without which a town or a region could be devastated, leading to further loss of revenue for other domestic-oriented businesses

it’s best to think about global trade as you think about keynesian investment theory : it operates as a multiplying factor for wealth

anything that impedes or obstructs it act in the opposite way : as a multiplying, wealth-destroying depressing factor

4) you say that fall of sterling or trade disruption would lead to reorientation towards more productive-efficient areas

the assumption you make is that RIGHT NOW, they aren’t being smart operators and paying premium for shoddy products

could you please prove that ?

could please show that both consumers and private sectors firm manager are not efficiently managing their purchases as per what they regard as their needs

and if they can’t do it now as in a normal, everyday settings, what evidence do you have that they will do so when under duress of a breakdown in trade patterns (say plunge in sterling’s value or drastic increase in trade tariffs with its major trade partners) ?

5) currently, the UK is a laggard in terms of productivity among OECD members

the reason are several and not limited to availability of “rather cheap” non-native educated labour

again, you make the assumption that firms are not currently hiring as per their best interests, but would magically do so under duress when catastrophe befalls them after a brexit

to pretend that productivity would increase afterwards, make several assumptions (that you leave unsaid) : a reduction in their number of employees, while having similar level of private-sector wealth generation

do you want to increase statistical productivity with large layouts throughout the country ?

alternately, increasing productivity to the top OECD while keeping the same number of employees, would mean increasing wealth generation by 20%-30% y/y for the next 5 years at least

how are you going to achieve that in times of upheaval and reduced trade, since you assume that the private sector is too inefficient and dumb to already do it NOW ?

7) as a corollary, you also assume that products and services from the EU are also not the most efficient, quality and price-wise, when they are purchased by UK agents compared to rest of the world ones (or in UKIP delusions, white anglosphere world).

could you provide evidence for those assumptions ?

8) Germany is around 15% of the EU, population and GDP-wise

and no, both the EU and the Eurozone do not work towards only the benefit of Germany

what Germany (and every other member states, bar the UK consistently) does is build alliances to strike compromises that benefit as many country as possible, so that it incrementally provides for itself too

the UK nativist authoritarian strategy is “me, me me and only me … or the high seas” …

in addition, EU council vote records show that the UK was 78% in with all the decisions agreed by the EU.

whatever the reasons of then then british governments for agreements, that’s definitely not the pattern of an international organisation (the EU) that take decisions CONSISTENTLY or STRUCTURALLY against its members

or think it this way : how many times did a law or regulation was not passed in Westminster’s parliament because of in-party rebellion, opposition’s refusal or Lord’s chamber ‘s obstruction ?

does it mean that the UK method of government is structurally biased against taking decisions that (in your narrow-mindedness) you judge to be in your interest ?

9) there is no “Community Preference” but in your own ignorant mind

that’s something that existed in the UK for Commonwealth countries and was deeply inefficient. something that UKIP and Brexit supporters wants to reintroduce by pretending that it somehow now exists in the EU.

I mean, seriously cut the crap with the delusions

firms in the EU are free to buy whatever goods or services from anywhere in the world

what they have to respect are consumer protection legislation to ensure that their suppliers do not endanger the health and safety of their end-customers

now, if you (and UKIP) want to be free to sell to UK consumers shoddy stuff that is cheap but unsafe, then so be it … and I dearly hope you would then be sued for your personal possessions when the inevitable litigations comes back to hit you, as victims pile in

Best regards,

1) Whatever. There is no need to build supranational coalitions if we are independent.

2) I agree they are a civil service, which I already said. But the UK has never agreed to unite into a single nation as Scotland did and was not conquered like Wales was. Representation in the Commission is important because it is another forum where the Eurozone countries push their own interests.

3) Sure, but what would happen is a gradual movement to more cost-efficient suppliers in the new circumstances. Optimally, we can maintain a free trading relationship with the EU since it is in all of our interests, but if not, trade will naturally realign in a few years. When the UK joined the EEC, people saw New Zealand food prices rise due to the external tariffs and quotas imposed by the EEC. Food imports thereafter reoriented toward the EEC countries.

4) Answered in 3

5) Low productivity growth and hiring of cheap labour is in the interest of business for as long as it is sustainable. It requires less investment in productive labour-saving capital and lower wage costs, implying higher corporate profits.

6) There was no 6

7) Community preference, that is, the external tariff. World food prices are substantially lower than the food prices in the EU, this is an example of trade diversion to the EU.

8) Deny it all you like. Germany is the main beneficiary of the Eurozone and through it effectively controls the EU. Look how Germany is signing agreements with Turkey over the objections of most Europeans.

9) Community preference exists. Just look it up. I did not come up with the idea. It is interesting that you compare it with Joseph Chamberlain’s idea of Imperial Preference, since this is exactly what it is. It’s just not _our_ Empire.

http://penguincompaniontoeu.com/additional_entries/community-preference/