Productivity growth has been slow in Western countries since the global financial crisis, but in Italy it has been stagnating for 25 years. Fadi Hassan and Gianmarco Ottaviano investigate inefficiency and misallocation in the Italian economy to draw broader lessons about what lies behind the ‘productivity puzzle’.

Productivity growth has been slow in Western countries since the global financial crisis, but in Italy it has been stagnating for 25 years. Fadi Hassan and Gianmarco Ottaviano investigate inefficiency and misallocation in the Italian economy to draw broader lessons about what lies behind the ‘productivity puzzle’.

Productivity has recently slowed down in many economies around the world. In the Eurozone, the UK and the United States, the standard measure of ‘total factor productivity’ (TFP) is still below the level it was at before the global financial crisis. In 2016, US labour productivity growth even fell into negative territory for the first time in the last three decades.

These trends are particularly worrying because productivity lies at the heart of long-term growth. A crucial challenge in understanding what lies behind this ‘productivity puzzle’ is the relatively short time span for which data can be analysed. An exception is Italy where productivity growth started to stagnate 25 years ago.

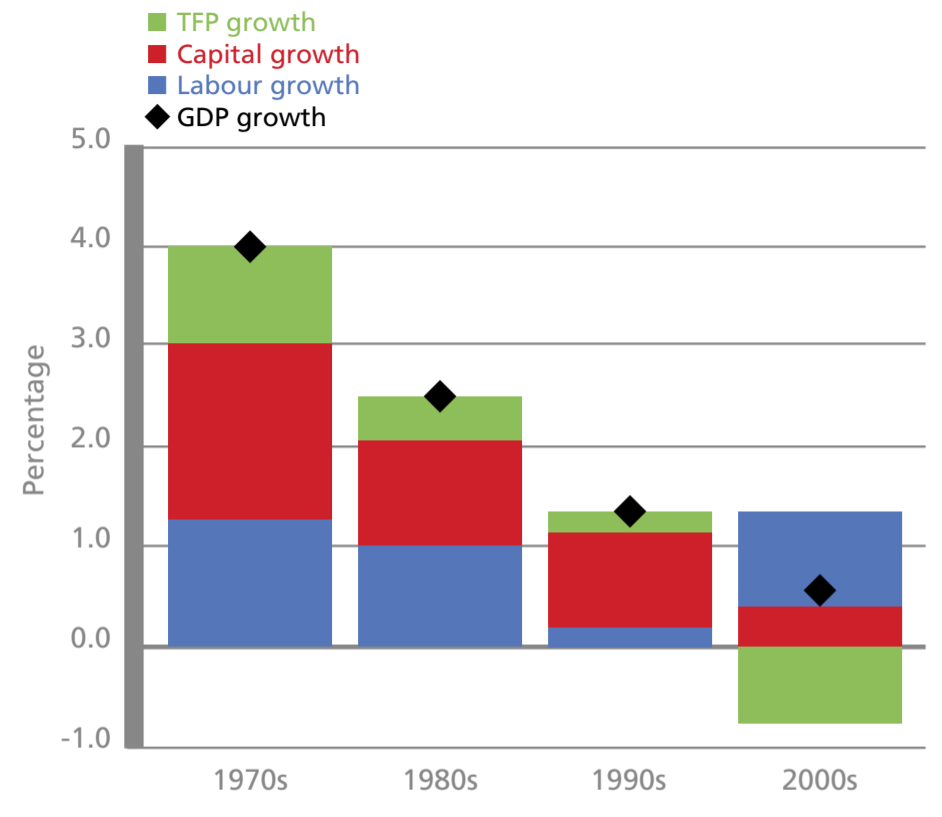

Figure 1 shows a growth accounting decomposition for Italy over the past four decades and the results are quite emblematic. TFP growth shrank throughout the decades, becoming negative in the 2000s. Italy turned from being among the fastest growing EU economies into the ‘sleeping beauty of Europe’ – a country rich in talent and history but suffering from a long-lasting stagnation.

Figure 1: Growth accounting in Italy

Note: Data from EU-KLEMS

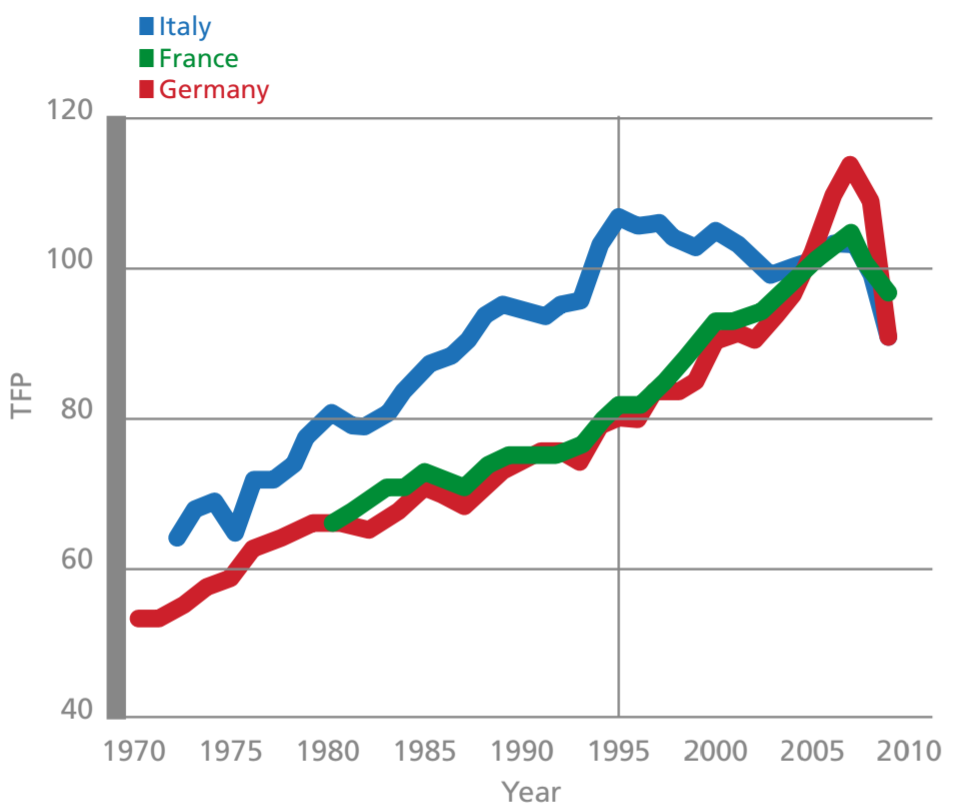

TFP dynamics in the manufacturing sector, where measurement issues are less tricky than in services, captures well the timeline of the Italian decline. Figure 2 shows a dramatic slowdown in TFP growth since the mid-1990s for Italy compared with France and Germany, where TFP continued to grow up to the global financial crisis. Italy therefore offers an interesting case to investigate in search of broader lessons that may hold beyond local specificities.

Figure 2: Evolution of total factor productivity in manufacturing

Note: Data from EU-KLEMS

We analyse the firm-level dimension of aggregate productivity and focus on the concept of resource ‘misallocation’ and its impact on productivity. The ‘productivity’ we refer to – TFP – measures how effectively given amounts of productive factors (capital and labour) are used. Clearly the economy’s aggregate TFP depends on its firms’ TFP. This happens along two dimensions:

- On the one hand, for given amounts of factors used by each firm, aggregate TFP grows when individual firm TFP grows – for example, thanks to the adoption of better technologies or management practices.

- On the other hand, for given individual firm-level TFP, aggregate TFP depends on how factors are allocated across firms. As long as market frictions ‘distort’ the allocation of product demand and factor supply away from high-TFP firms towards low-TFP rivals, they lead to lower aggregate TFP than in an ideal situation of frictionless markets.

How do we measure misallocation? Building on a distinction between physical TFP (measured as the ability to generate physical output from given inputs) and revenue TFP (TFPR, measured as the ability to generate revenue from given inputs), we observe that in the absence of frictions, TFPR should be the same for all firms while firms can still differ in their physical TFP.

The idea behind this result is simple: with no frictions, the marginal revenue product of inputs should be equalised across firms as factors move from low to high marginal revenue product firms. As marginal revenue product equalisation implies TFPR equalisation, Hsieh and Klenow call deviations from a situation in which TFPR is equalised ‘misallocation’. They propose a simple way to measure its consequences for aggregate TFP.

This is also the definition of misallocation that we adopt. It implies that the dispersion of TFPR across firms can be used to measure the extent of misallocation. It also implies that firms with a TFPR higher than the sectoral average are inefficiently small, while those with a TFPR below the sectoral average are inefficiently large. These are the two key implications of previous research on misallocation that we use.

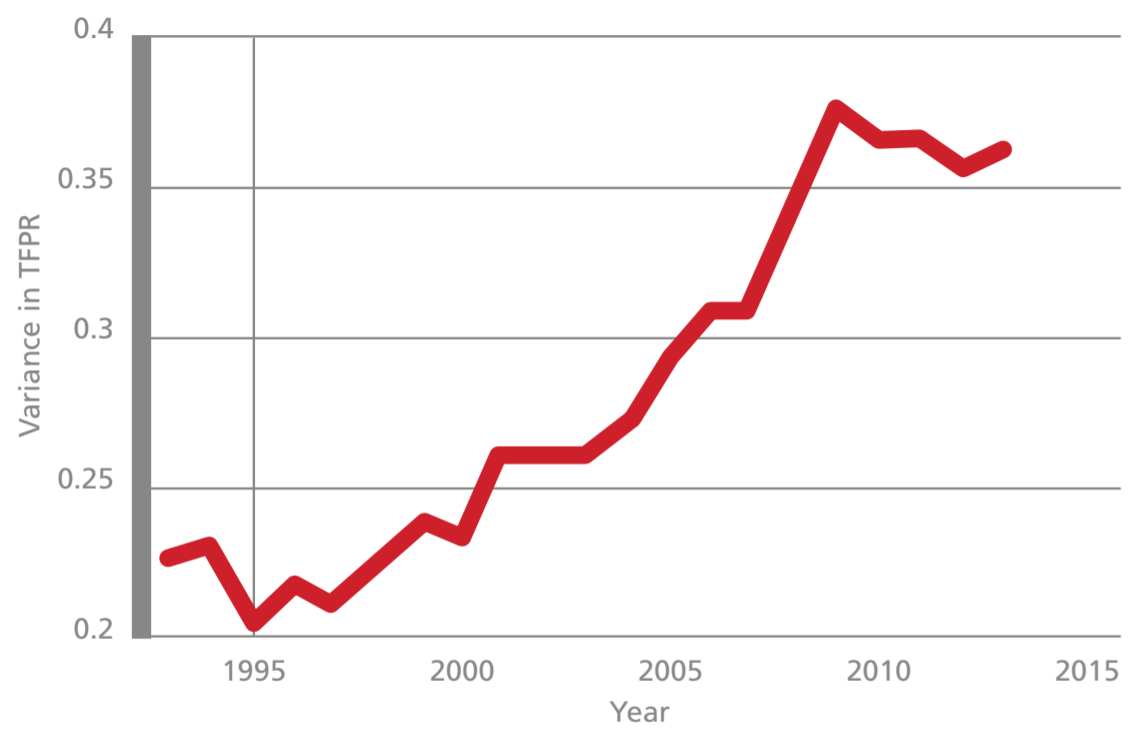

With these definitions in mind, we study the universe of Italian incorporated companies over the period from 1993 to 2013. We find strong evidence of increased misallocation since 1995 (see Figure 3). If misallocation had remained at its 1995 level, aggregate TFP in 2013 would have been 18% higher than its current level. This would have translated into 1% higher GDP growth per year, which would have helped to close the growth gap with France and Germany.

Figure 3: Evolution of aggregate misallocation (1993-2013)

Note: Data from CERVED

We find that the main source of misallocation comes from the within-industry component rather than the between-industry component: misallocation has mainly risen within sectors than between them. This implies that moving factors of production from, for example, textiles into information technology would increase aggregate productivity less than ensuring that more efficient firms within textiles are the ones that absorb more resources.

Importantly, we find evidence that misallocation has increased more in sectors where the world technological frontier has expanded faster when, in the wake of Griffith et al, we measure the speed of technological change in a sector by the average change of R&D intensity in advanced countries. Relative specialisation in those sectors explains why, perhaps surprisingly, misallocation has increased particularly in the regions of Northern Italy, which traditionally are the driving forces of the Italian economy.

The broader message is that an important part of the explanation of the recent productivity puzzle may lie in a generally rising difficulty of reallocating resources across firms within sectors where technology is changing faster rather than between sectors with different speeds of technological change.

Analysis of the characteristics of firms that are inefficiently sized sheds additional light on the relationship between exposure to frontier shocks and misallocation within industries. In particular, we look at corporate ownership and management, finance, workforce composition, internationalisation and innovation.

We find that the firms that are more likely to be inefficiently small and thus under-resourced are those that employ a larger share of graduates and invest more in intangible assets. In contrast, those that are inefficiently large and thus overresourced are the firms with a large share of workers under a wage supplementation scheme, and which are family-managed and financially constrained.

We interpret this as evidence that rising within-industry misallocation is consistent with an increase in the volatility of idiosyncratic shocks to firms, due to their heterogeneous ability to respond to sectoral frontier shocks in the presence of sluggish reallocation of resources.

What does this all mean for policies to raise productivity? One implication is that rather than trying to switch resources between sectors, policy intervention should aim at allocating capital and labour to the best performing firms within sectors.

Policy intervention should therefore focus less on moving capital and labour from – for example, textiles to electronics – than on facilitating the mobility of workers and capital towards the most productive firms within the textile sector. Similarly, higher benefits would be reaped by moving the factors of production to the most productive firms within depressed geographical areas rather than moving them to more vibrant areas.

This represents both an opportunity and a challenge. An opportunity, because moving factors within sector or area is less costly than across them; but also a challenge, because it is harder to determine what prevents high-productivity firms from expanding and low-productivity firms from shrinking within the same sector or geographical area.

More generally, setting the framework conditions for the proper functioning of market-driven reallocations could be more effective than pursuing traditional industrial policies aimed at ‘picking winners’, whether they are sectors or regions.

Please read our comments policy before commenting.

Note: This article is based on a contribution to the spring 2018 edition of CentrePiece: The Magazine of the Centre for Economic Performance. It gives the views of the authors, not the position of EUROPP – European Politics and Policy or the London School of Economics. Featured image credit: CEP

_________________________________

Fadi Hassan – Trinity College Dublin / CEP

Fadi Hassan is an Assistant Professor of Economics at Trinity College Dublin and is a Research Associate in the Centre for Economic Performance’s trade programme.

–

Gianmarco Ottaviano – CEP

Gianmarco Ottaviano is Professor of Economics at the LSE and Director of the Centre for Economic Performance’s trade programme.