Italy’s government and the European Commission continue to be locked in a standoff over the Italian budget. Corrado Macchiarelli writes that while the budget plan is badly designed and must be addressed, there is also clearly a need for euro area reforms and more mutual recognition. Ultimately the Economic and Monetary Union is facing a political problem and the current approach to the Italian crisis is not going to aid the popularity of either the EU or the single currency.

Italy’s government and the European Commission continue to be locked in a standoff over the Italian budget. Corrado Macchiarelli writes that while the budget plan is badly designed and must be addressed, there is also clearly a need for euro area reforms and more mutual recognition. Ultimately the Economic and Monetary Union is facing a political problem and the current approach to the Italian crisis is not going to aid the popularity of either the EU or the single currency.

The Italian government has plans for tax and spending that are now seen as one of the biggest challenges to the way the Economic and Monetary Union (EMU) runs. The Italian spending package, which was rejected last month in a historical move by the European Commission, has now been revised downwards by the government, however fundamentally reflecting Rome’s refusal to accept any clues in backing-down.

This opens a whole new chapter for political risk in Europe. The revised programme still involves a new citizens’ income, more generous pensions through a reduction of the pension age and lower taxes. Estimates suggest these measures will cost 2.4% of Italy’s GDP in 2019 (dropping to 2.1% in 2020), clashing with the EMU’s fiscal rules.

On 13 November, the IMF published Italy’s Staff Concluding Statement of the 2018 Article IV Consultation, suggesting Italy should implement a fiscal consolidation plan “based on high-quality measures” – together with a package of structural reforms, and bank balance sheet strengthening – as there are currently too many downside risks to increasing public expenditure. This is also in the light of the IMF’s more conservative output gap projection for Italy, compared to the OECD, the European Commission and the Italian government.

The further IMF endorsement of fiscal attentiveness comes as no good news for the Italian government. As highlighted by many recently, including Francesco Daveri on the Italian watchdog lavoce.info, the reform package proposed by the Italian government, even in its revised form, is clearly not set up right, being a burst to the national economy, with no effective growth prospects. This is because of mere deficit-spending social policies proposed, the “bill of which is essentially being footed by enterprises, banks and insurance companies”.

This idea that financial markets act as an echo chamber for budgetary rules is not new to the EMU debate. There is also a sense that part of the “bad economics” or “policy mistakes” which led to the sovereign debt crisis in 2010 are partly imputable to the wrong rhetoric on austerity (as Simon Wren-Lewis underlines in a recent blog post), missing a key point on the Eurozone crisis: countries issue debt in a currency they have no control over. Here, the ECB could not – for political reasons – in the first instance act as governments’ ‘lender of last resort’. This is what Paul De Grauwe calls a ‘harder’ budget constraint on EMU member states.

From the point of view of deficit spending, and its political underpinning, one important dimension to consider is the international / credibility dimension. Italy has lower total indebtedness – private and public combined – than Britain, France and Spain. However, as far as the EU’s fiscal criteria are concerned, only public debt matters. In addition, other issues are affecting the country’s international stance, including the distribution of non-performing loans across the banking sector, ‘home bias’ or the excessive reliance of public debt’s ownership by the private sector (62.1% of government debt as a percentage of total government debt is held by domestic financial institutions – including the central bank), as well as important competitive issues which have resulted in a dramatic loss of competitiveness over time. Currently, Italy is also the euro area country with the highest expenditure on interests on past debt (as a percentage of GDP), and was projected already last year to be the EMU country with the highest gross financing needs (as a percentage of GDP), according to the European Parliament.

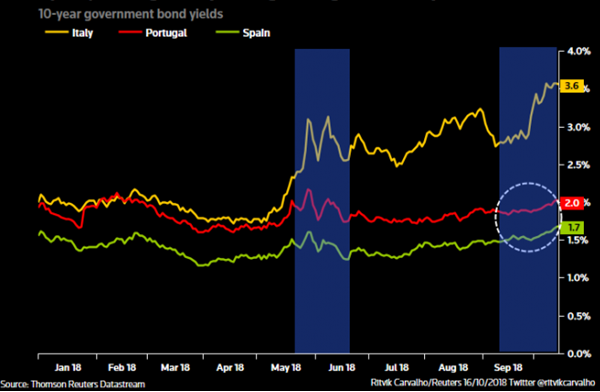

Figure: Ten-year government bond yields in Italy, Portugal and Spain

Source: Thomson Reuters Datastream

Currently, the projected deficit increase, under the threat of sanctions being activated at the European level through the fiscal compact’s corrective arm (the so-called Excessive Deficit Procedure, EDP), is increasing the premium investors demand on Italian government bonds, signalling de facto capital flight, as investors may be perceiving a greater redenomination risk. During the last few months, Reuters’ Abhinav Ramnarayan and Ritvik Carvalho have discussed how the data on spreads between the 10-year Italian government bonds against the German bund show Italy being progressively clustered alongside Greece, rather than Spain and Portugal, which show little effect of contagion. As Figure 1 above shows, from April 2018 onwards the spread of Italy has increased significantly on two occasions while those of Spain and Portugal remained close to previous values (something Peter Schwendner also underlines).

How much ‘politics’ is there in EMU fiscal rules?

There are consistent arguments to put forward proposals that limit the budget deficit of Italy, in the absence of measures addressing the structural concerns of the Italian economy which should be tackled through outright reforms (see the IMF). First and foremost, the current government may not worry about the true costs of skipping the chance for debt reduction, since the burden will fall on future taxpayers and governments, thus providing an incentive to offload these costs to future generations. This is not a new concern in the history of Italy’s debt creation – starting from 1982, Italian debt shattered without the (then) future taxpayers being able to participate in the decision process, nor with their interests being taken into account.

This said, the problem with the current Italian political impasse is that, as the result of financial market risk-pricing, the country’s political clout in EMU affairs has been reduced and any residual fiscal capacity eroded. This stems from the very nature of the EMU, which, in the absence of federal guarantees, risks becoming a zero-sum game. The ECB’s constitution does not allow for the bailout of a member state. In the past the problem was not perceived as dependable: i.e. the EMU zero no bail out clause was simply “not credible” if a large country such as Italy were to run into problems. Today, in the absence of fiscal and political entities like in the U.S., the country is confronted with a hard budget constraint because things are politically different.

How does this play with the current situation?

In the past, no credible ways of enforcing sanctions on sovereign nations were adopted (e.g. Germany and France in 2004/05). In addition, the way the conundrum of the absence of a lender of last resort was solved, at the peak of increased market speculation in 2012, was through Mario Draghi’s announcement of the ECB’s readiness to do “whatever it takes”, which marked the introduction of the Outright Monetary Transactions (OMTs). The crisis further triggered important reforms of the European governance framework, including a Banking Union for Europe that is yet to be completed (but is expected around 2026). However, the introduction of OMTs is challenging, as it represents monetary policy with conditionality, the implications of which are not clear a priori, and the mechanism hadn’t previously been tested.

There should be no stigma in using fiscal policy for growth support (this relates to the issue of EU legitimacy, as De Grauwe recently noted), however one should consider the cost of sustaining aggregate demand – consumption, in particular – through bursting public expenditure, against the increased uncertainty it creates because of political risk. This risks weighing negatively on (business) confidence resulting, on balance, in a negative fiscal expansion.

There are currently five options for the Italian case. The first option is a situation reminiscent of what happened during the sovereign debt crisis, where, under the course of several political frictions and rebuttals, financial markets were essentially able to tip the scale towards budgetary consolidation and hence heavy fiscal restraints and competitiveness adjustments (through a reduction in unit labour costs) in a country like Greece. Something similar could happen if things escalate, the excessive deficit procedure is activated, and investors’ confidence drops further, meaning the Italian budget showdown will play in favour of the European Commission’s policies; something many would read as an Italian Commissariamento.

The second, less likely as well as less desirable option, is that the Italian government will not back-down in the budget standoff, by introducing, for instance, a parallel currency without leaving the euro.

Third, there could be complete flexibility on the Italian budget, as was the case for Germany with the Hartz IV reforms and the violation of the Stability and Growth Pact in 2004 with Romano Prodi’s presidency at the European Commission.

Fourth, an intermediate solution to the first and third options (even if possibly more skewed towards the first) would be a situation where the European Stability Mechanism (ESM) is activated. In case of ESM involvement, as the ECB’s Peter Praet recently signalled, the country will have to take correctional (structural) measures anyway, thus overriding the national political economy. The advantage of ESM involvement in Italy, though, is that it would make it eligible for outright monetary transactions which would help the government step towards a sustainable path by lowering sovereign borrowing costs. In this case as well, however, the ESM policies may have to supersede the government’s commitments with the electorate.

Finally, the last option would involve the recognition that this political shutdown underlines something else, requiring a further opening at the EU (or EMU) level.

A political problem

The biggest weakness in the bloc is now politics and the current approach to the Italian crisis is not going to help the popularity of either the EU or the single currency. As many have underlined, democratic expectations cannot be set at the same level as they are within nation states: the latter re-distribute 40-50 percent of GDP while the EU budget is a mere 1 percent of GDP. The legitimacy of the EMU is nevertheless key and the ‘politics’ beyond fiscal rules make the principle of ‘no taxation without representation’ more relevant than ever for the Italian political standoff.

Support for the euro has been rising in the past couple of years, but this is fragile. At the beginning of last year, the vast majority of Italians expressed discontent about the EU’s handling of the refugee crisis and the economy. Italy has currently a Eurosceptic majority (about 60 percent) according to Eurobarometer data. The badly designed budgetary plan in Italy needs addressing, and there is also a general need to cope with the logic that the EU now has stricter fiscal rules (including the excessive deficit procedure’s semi-automatic sanctions, implemented through reversed majority voting). But this notwithstanding, there is clearly a need for euro area reforms and more mutual recognition.

Practically, the instrument to achieve this would have to combine risk reduction at the EU/EMU level (for example through a Capital Markets Union) and the national level through lower sovereign debt (as part of the 2-Pack, 6-Pack and Fiscal Compact) with cap exposure by banks (see the IMF). This would require, at the same time, signalling at the EMU level for more concessions on complete risk sharing, through an explicit fiscal agreement. In other words, a policy that focuses on the stick and no carrot at the EMU level hasn’t worked in the past and will certainly not work in the future, particularly if the EMU is looking to create a consensus and convergence of (political) interests from the bottom.

Please read our comments policy before commenting.

Note: A longer version of this article is available at the author’s personal blog. This article gives the views of the author, not the position of EUROPP – European Politics and Policy or the London School of Economics. Featured image: Giuseppe Conte, credit: NATO (CC BY-NC-ND 2.0)

_________________________________

Corrado Macchiarelli – Brunel University London / LSE

Corrado Macchiarelli is a Lecturer at Brunel and a Visiting Fellow in European Political Economy at the LSE European Institute.

2 Comments