By Riccardo Crescenzi and Simona Iammarino, LSE, department of Geography and Environment.

By Riccardo Crescenzi and Simona Iammarino, LSE, department of Geography and Environment.

Corporate networks have dramatically altered regional connectivity and interdependence around the world. Multinational enterprises’ (MNE) networks have created both winning and lagging cities in a globalised world, spurring uneven regional development. For regions and cities access to internal and external knowledge is not about simple regional connectedness – i.e. the architecture of transport and communication infrastructure. It is the broader connectivity that matters: the capability of individuals, firms, organizations and institutions to interact and engage across geographical space and within networks. Ultimately, regions that improved their connectivity during the crisis benefit from more favourable post-crisis trajectories (at least in the short-term) both in terms of GDP and employment.

European regions: densely connected by people, businesses and ideas

Regional economic development depends on the two-way (inward and outward) connectivity that shapes the regional churn of skills, talent, competences and business functions. The dynamic recombination of key cognitive and productive local assets pushes cities and regions to constantly adapt, react and develop in an ever-changing global environment.

What matters are the spatial extent, nature and directionality of this connectivity. First, in a globalised world the geographical extent of resource inflows and outflows needs to be also extra-local, international and global (spatial extent). Second, the nature of the flows is highly diverse: different types of capital, skills and knowledge are bundled in the intra- and inter-firm connections that form global production networks and value chains, and their diversity translates into a variety of impact on the regions and cities involved. Third, regional economies can be simultaneously origin and/or destination of the flows of investment by MNEs. The simultaneous exposure to inflows and outflows (bi-directionality) – as in most of the European Union – makes the concepts of ‘host’ and ‘home’ overlap and blur. The extent of connectivity underlies the ability of cities and regions to renew their competitive advantages and to react to shocks, determining their long-term resilience, performance and welfare.

Measuring connectivity

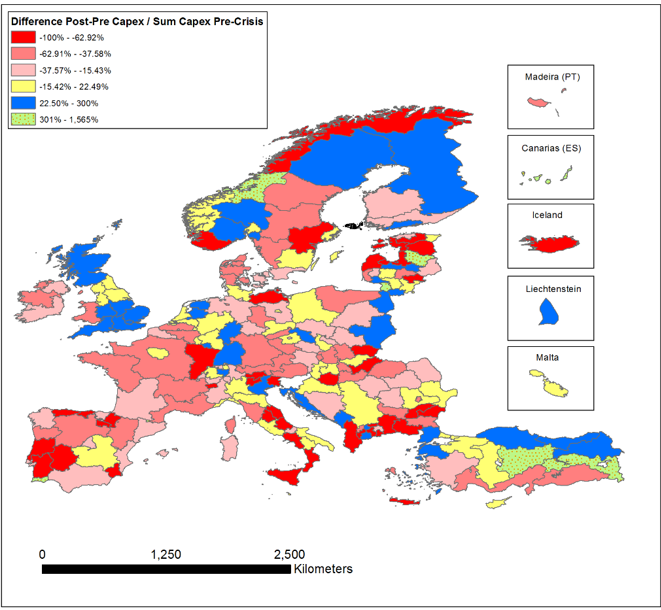

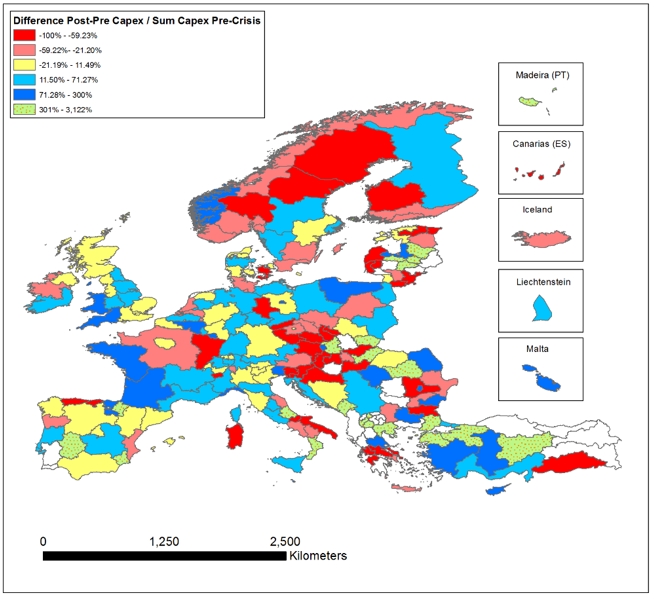

An idea of regional connectivity can be provided by Foreign Direct Investment (FDI) in and from the European regions. This indicator gives a preliminary indication of their capacity to adapt their position in global flows in response to shocks – Figures 1 and 2 look respectively at the relative variation of FDI cumulative capital expenditure inflows and outflows between the pre-crisis (2003-2008) and the post-crisis (2009-2014) periods.

Source: authors’ elaboration on fDi–Markets data

Source: authors’ elaboration on fDi–Markets data

Different colours mark different positions of the regions in the distribution of the reactions to the 2008 crisis in terms of inward and outward FDI. The classification is based on the distribution of the normalised change in the capital invested between the two periods: each colour-coded category identifies a quintile of the distribution.[1] A sixth category – the green colour with orange dots – is included in the maps to identify outliers (i.e. regions with pre-crisis investment values close to zero that inflate the change even with modest increases in the following period). Whilst focussing on the individual maps can shed light on the evolution of investment flows over time (changes in connectivity across space), the comparison of the two maps offers a first description of the directionality of the flows and their relative balance.

Stayers, Slippers and Climbers

Both maps mark in yellow the regions that can be classified as stayers, i.e. those that maintained a similar magnitude of FDI inflows and/or outflows before and after the crisis (percentage change close to zero). Figure 1 shows that, in terms of inflows, the stayers are localised: a) around the central axis of Europe from the North (Yorkshire and the Humber, North East, and North West England), to the Centre (Île-de-France, Southern- and Western Netherlands, north-west of Germany, and Lombardia, Liguria, and Emilia-Romagna in northern Italy), and the South (Apulia and Basilicata in the Italian Mezzogiorno); b) in Eastern Europe, with regions in Hungary (Central and Western Transdanubia, Northern Hungary), Lithuania (Kaunas, Šiauliai and Vilnius Counties), Romania (Sud-Muntenia and Sud-Est) and in the candidate countries of the Balkans (Albania and Kosovo) and Turkey (East Marmara, Istanbul, West Anatolia). Turning to FDI outflows in Figure 2, the stayers are concentrated in the north (Scotland, Northern Ireland, North West England) and south (South East and East of England) of the United Kingdom; north of Italy (Lombardy, Veneto, Trentino-Alto Adige); and large part of Spain (e.g. Galicia, Madrid, Castile and León, Aragon, Catalonia, Andalusia). The regions of Paris (Île-de-France), Milan (Lombardia) and those in the north-west of Germany are the most noticeable stayers in terms of both inflows and outflows, suggesting a strong resistance to external shocks in terms of global capital flows. Different is the pattern of regions such as Scotland, South East and East England, Northern Netherlands, or Friuli-Venezia Giulia in Italy: they retain their position in terms of outflows but improve their capacity to attract foreign investments. Other regions, such as Północno-Zachodni in the north-west Poland, Castilla-La Mancha in Spain, Lazio, Emilia-Romagna and Liguria in Italy, Yorkshire and the Humber and North East England in the UK, and Central Greece, manifest the opposite pattern, i.e. being stayer in attractiveness toward foreign capital but experiencing increases in outflows.

While in fact some regions are stayers in terms of their FDI connectivity, others are climbers, improving their position in terms of inflows and/or outflows after the crisis (they are marked in different shades of blue in the two figures). The dark blue areas identify those regions that gained the most after the 2008 shock. Figure 1 presents a rather disappointing picture: very few EU regions have been able to exceed their pre-crisis position and – considering the fast growth of developing and emerging economies in the same period – it is clear that the shock has so far taken a conspicuous toll in terms of attractiveness of foreign capital. Climbers are some of the historically most attractive regions of Europe – South-East and South-West England, Scotland, Baden-Wurttemberg and the south of Norway – but also ‘new entries’ in the East of Europe that started from very low levels before the crisis, e.g. the eastern regions of Poland, some in Romania and Bulgaria, in the Baltic States, and in part of Turkey. Figure 4 shows instead a very different picture: many more regions have increased their outward investment projects after the crisis, possibly due to concurrent technological and organisational forces spurring the rationalization of MNE operations and boosting the offshoring of an increasing number of business functions. In almost all EU ‘old’ members, regions are investing more abroad than they did before the crisis: South West and Wales in the UK, West and South West in France, some northern and central Italian regions. However, outward climbers are to be found also in eastern Europe, for example the northern regions in Poland, and in candidate countries such as Serbia and Turkey.

Climbers with respect to both outward and inward flows are harder to find, with a few notable exceptions such as Baden-Wurttemberg and Hessen in Germany, the South of England and the Midlands in the UK, traditionally regarded as European regional winners. Emerging winners may be found in the Adriatic Croatia, and in the region Wschodni in Poland. In line with our conceptual framework, the winners show a remarkable increase in the magnitude of their flows that is coupled with bi-directionality, providing local actors with greater connectivity and, as a result, with growing opportunities for the renewal of local and regional economic structures.

The regions that experienced a contraction in their connectivity after the crisis – here labelled slippers – are depicted in shades of red in both figures. Figure 1 confirms that large part of the European regions have still not recovered from the crisis: slippers are located in the entire periphery of Europe – Portugal, Spain, southern Italy and Greece – although with different intensities, but also in France (East France), Sweden (East Middle Sweden) and central (Mecklenburg-Western Pomerania in Germany) and eastern EU members (especially in some regions of Bulgaria, Estonia, Hungary, Latvia, Lithuania and Slovakia). Figure 2 indicates that that the reduction in outward investment has remained confined to the eastern part of France (East France), southern Italy (Apulia, Molise, and Sardinia), Sweden (Middle and Upper Norrland), Easter Austria, and eastern EU members.

Overall, the combined picture provided by both maps for slippers indicates that many peripheral European regions can be classified as losers, having lost their overall connectivity (inward and outward) through MNE investment flows.

Connected regions fare batter in terms of employment and growth

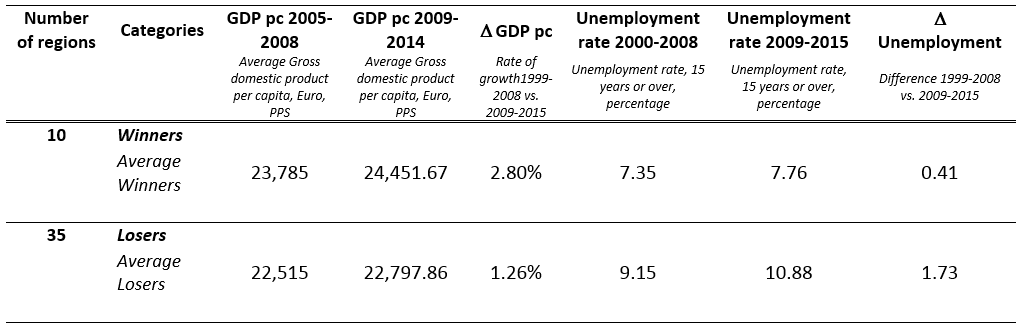

Finally, Table 1 looks at GDP and unemployment for winners and losers (i.e. climbers/slippers simultaneously for both inward and outward FDI). The key difference between winners and losers is not in GDP per capita levels (both groups are in line with the EU28 average), confirming that our suggested classification does not reflect ‘simple’ disparities in income levels. Notwithstanding the similarity in initial conditions, however, winners benefit from more favourable post-crisis trajectories (at least in the short-term observed here) both in terms of GDP and unemployment. Favourable changes in two-way connectivity are generally associated with higher positive changes in GDP per capita and – in particular – to very modest increases in unemployment rates. The winners suffered an increase in their unemployment rate by 0.41 percentage points against an average increase by 1.79% in the losers and 1.49% in the EU28. This provides tentative support to the initial intuition that two-way connectivity and its nature are fundamental elements for the understanding of regional trajectories.

Source: authors’ elaboration on Eurostat data

Interdependence and connectivity make public policy particularly important, both in ‘looking up’ – i.e. lobbying to address global negative externalities that need be corrected through international regulation, – and in ‘looking down’ – i.e. supporting regional systemic integration and institutional capacity building for development and resilience.

This blog post is based on Crescenzi R. and Iammarino S., “Global Investments and Regional Development Trajectories: the Missing Links“, Regional Studies, 51(1), 97-115, 2017, DOI: 10.1080/00343404.2016.1262016 [Open Access]