Analysing how millions of multinational corporations structure their global ownership chains reveals that Cayman acts as a ‘sink’ offshore financial centre where foreign capital accumulates and data trails often end, writes Jan Fichtner (University of Amsterdam).

Analysing how millions of multinational corporations structure their global ownership chains reveals that Cayman acts as a ‘sink’ offshore financial centre where foreign capital accumulates and data trails often end, writes Jan Fichtner (University of Amsterdam).

Try to guess what the top destination of outward foreign direct investment (FDI) from Brazil is! Could it be the United States as the largest economy in the world, neighbouring Argentina, or maybe fellow BRIC country China?

All wrong! It’s the Cayman Islands, a tiny group of islands in the Caribbean just south of Cuba. In 2015, the stock of FDI from Brazil into the Cayman Islands amounted to a staggering US$52 billion (with US$2.5 billion going in the opposite direction). This represents over one third of total outward FDI from Brazil. What’s more, investors domiciled in the Cayman Islands hold portfolio investment in Brazil worth over US$26 billion (with US$2.6 billion in the opposite direction).

Even if work by the FickleFormulas project is showing how problematic and imprecise macroeconomic indicators such as FDI are, these are astonishing numbers: the Cayman Islands has a population of only 60,000 and a domestic economy of just US$3 billion. Moreover, Brazil is not the only country in Latin America which has strong bilateral investment ties to Cayman. Chile, for example, has FDI into the Cayman Islands of US$7.5 billion while Cayman holds US$1.5 billion of FDI into Chile.

But Cayman is not only a large financial centre for countries in Latin America. Rather, the jurisdiction arguably acts as a central node of contemporary global finance. The combined value of banking activity from abroad, foreign portfolio investment, and foreign direct investment is over US$4,000 billion. That is, this tiny Caribbean archipelago has attracted more foreign assets than various advanced industrial countries such as Japan, Canada, or Italy, even though they have economies generating several hundred times Cayman’s gross domestic product. How can we explain that such a miniscule jurisdiction, far removed from the centres of global trade and finance, is in fact the largest international financial centre of all Latin America and the Caribbean?

As I have argued in a recent research paper, the Cayman Islands should be seen as a key node in an Anglo-American financial triangle that also involves the United States – its major counterpart jurisdiction in banking and investment – and the United Kingdom – its sovereign power.

It should be remembered, contrary to many media reports, that Cayman is not an independent country, but a British overseas territory. Cayman controls domestic matters such as taxation and regulation, and London takes care of international affairs and defence.

Remarkably, in legal terms it is still correct today to refer to the Cayman Islands and other British dependencies, such as Bermuda or the British Virgin Islands (also large offshore financial centres), as ‘colonies’ of the United Kingdom. This status provides Cayman with a level of political and economic stability that competing jurisdictions like Belize or Panama cannot offer. The Cayman Islands also inherited a very business-friendly legal system based on English common law, which is attractive to multinational corporations and investors such as hedge funds. Beyond that, there is a very strong presence of the Big Four global accounting firms, always eager to help draft Cayman laws and facilitate financial activities.

Hedge funds – lightly regulated ‘alternative’ investors that primarily cater to wealthy individuals and large institutions – illustrate the status of the Cayman Islands as an ‘upmarket’ offshore financial centre particularly well.

More than 50 per cent of all global hedge funds are legally domiciled in the Cayman Islands, benefiting from zero taxation and tailored regulation, even if the actual hedge fund managers work almost exclusively in New York and London (or NY-LON). This makes hedge funds a quintessentially Anglo-American financial industry. Since hedge funds almost exclusively buy financial securities for short-term trading, most of their activities show up in statistics on portfolio investment.

According to data from the IMF, in mid-2016 Cayman was the world’s fifth largest financial centre in terms of foreign portfolio investment, which was worth an astonishing US$2,640 billion at that point. Thus, Cayman has attracted more portfolio investment than Germany, the Netherlands, and Japan.

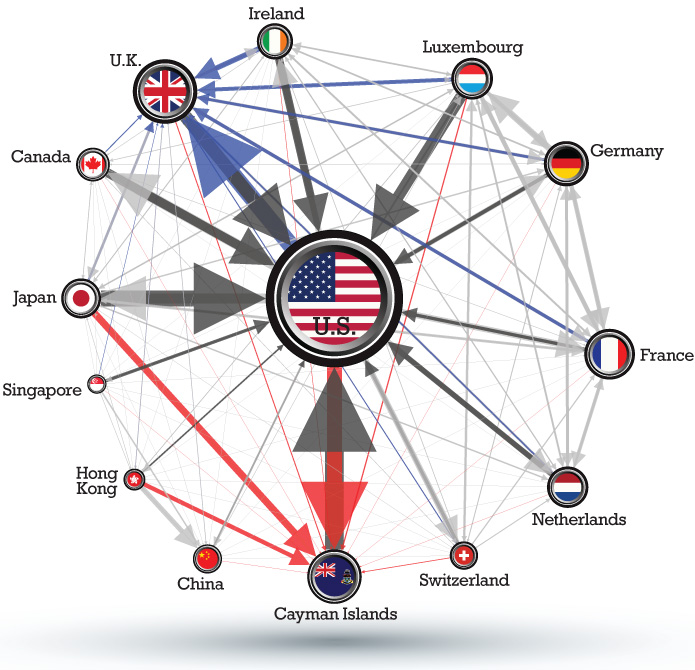

Combining data from the IMF and the US Treasury has allowed me to visualise the role of the Cayman Islands in international portfolio investment.

Figure 1 (below) shows that Cayman primarily acts as a kind of conduit to US financial markets for investors from Japan and Hong Kong. American investors have invested massively in hedge funds, which are legally domiciled in Cayman. In turn, these hedge funds have mainly bought US securities, closing the financial loop between the US and the Cayman Islands. This unique financial loop explains why Cayman is the largest holder of US securities in the world (excluding US long-term debt, of which the Japanese and Chinese central banks hold more than US$1,000 billion each).

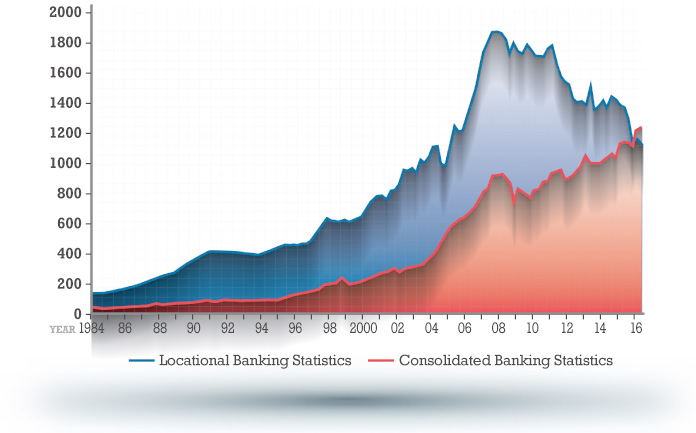

Another huge segment for the Cayman offshore financial centre is banking. Here, both Japan and the US act as the dominant counterpart countries. American and other foreign banks use the Cayman Islands for intra-group transactions in US dollars. However, according to the Locational Banking Statistics of the Bank for International Settlements (BIS), intra-group transactions by foreign banks peaked in 2011 and have been declining ever since (see Figure 2, below).

The Consolidated Banking Statistics of the BIS provide another perspective on the Cayman Islands banking centre. They show claims by foreign banks on counterparties resident in Cayman (e.g. hedge funds). In 2016, foreign banks had consolidated claims on Cayman counterparties of over US$1,200 billion – a new all-time high. Quite surprisingly, Japanese banks account for over 40 percent of that large number, which is the highest share of all countries, while American banks are responsible for about 30 percent.

But is the role of the Cayman Islands as one of the largest offshore financial centres relevant to people outside of high finance?

In a recent research paper, the CORPNET project analysed how millions of multinational corporations structure their global ownership chains. We found that Cayman acts as a ‘sink’ offshore financial centre that attracts and ‘retains’ foreign capital and/or where data trails often end. Large multinational agriculture commodity companies such as Bunge or Cargill that are active in the Amazon basin (e.g. in soy production) use the Cayman Islands in their global corporate ownership chains, thus most likely undermining the sustainability of a key global environmental commons.

The Offshore Shell Games 2017 study recently found that Cayman subsidiaries of the top 500 American multinationals have reported profits of over US$46 billion – 13 times Cayman’s GDP! In this way, these large corporations save billions of taxes in the United States.

In 2015, the Tax Justice Network classified Cayman as a secrecy jurisdiction. Hence, even though it has increased regulation in recent years due to international pressure, the Cayman Islands still provides foreign corporations and investors with a considerable degree of secrecy – in addition to zero taxation, of course. Therefore, Cayman continues to facilitate opacity and tax avoidance.

As an ‘upmarket’ offshore financial centre, Cayman is reacting to international pressure in order to avoid reputational damage. London, as Cayman’s sovereign power, could arguably force the jurisdiction to become much more transparent – if the political will existed.

But there lies the real Cayman conundrum: why do short-term financial interests in Britain still dominate over long-term concerns for society and the environment?

Notes:

• The views expressed here are of the authors rather than the Centre or the LSE

• This post draws on the co-authored article “Uncovering Offshore Financial Centers: Conduits and Sinks in the Global Corporate Ownership Network” (Nature, 2017)

• Please read our Comments Policy before commenting

Goedemiddag Jan

Ja, ik spreek nederlands, maar ik ben eigenlijk Brits.

And a vey useful language it turned out to be in my job as multilingual researcher, global financial intelligence, including South Africa.

I’ve only just picked up on your article as a result of doing other research but I’ve bad news for your colleague Professor Morris, something that I suspected years ago – part of my job was putting together a global inventory of investment funds – that something that now has the FBI not not only frothing at the mouth but banging on the door of Congress demanding that all unregulated funds, namely hedge and PE funds, be brought under the control of the SEC, probably under the 13F rule, on the grounds they are being used as money laundering vehicles. And where are ca 75% hedge funds domiciled – Cayman Islands! 11,0000 in total.

Some twenty odd years ago when I did get information from the CIMA it ran to 12 pages. Today on the Internet it stands at 180, though most of my information came by way of Ireland, the Central Bank, given that at the time nearly all tax haven domiciled funds were being listed on the Irish Stock Exchange

If you know the Cayman Islands then you must know Maple & Calder (The Maples Group) the one that puts Mossack &Fonseca (Panama Papers) and Appleby (Paradise Papers) in the shade. Latest titbit about them – they’ve just become the latest Listing Sponsor, Investment Funds, on the Irish Stock Exchange

Prettige dag

Trish Wilson

Dear Patricia,

thanks for your comment. Keep up the important work of monitoring what’s going on in the Cayman Islands.

Kind regards,

Jan

I congratulate you on your data collection and analysis.

I find it confusing why you should want to add a spectre of nefarious dealings to Cayman; when Britain and New York are where the entire global financial system was nearly destroyed for the 3rd time in the last 30 years.

Isn’t Cayman really, the equivalent of Austria under Metternich from 180801848 – a tiny state that controlled the theatre of Europe,

I never understand why it is not possible to look at Cayman’s achievements – essentially as the largest lender to the US government – and say, what skill and confidence. I was leading an official visit to Singapore in 2007 and Professor Jayakumar – then Singapore’s Deputy Prime Minister and former Justice Minister said: “If you have a Cayman fund, we just wave you in, because we trust their regulations”. Between 2008-2012, 60% of companies investing in China where Cayman Funds. Cayman is not perfect, but picking an agricultural company registered in Cayman that may be misbehaving in the Amazon undermines your credibility and seems to forced up something ominous about Cayman.

They are just bloody disciplined and run their country the way Apple runs as a company. Apple is not perfect, as labour disputes show. But that hardly warrants clouding their stupendous accomplishments.

Otherwise, I enjoyed your paper. Excellent graphics.

cheers

M.

Professor Gilbert NMO Morris

#cayman #Financial #Treasuries #Banking