Numerous reports warn that Brexit may have negative effects on the UK stock market. But whatever the outcome, it seems unlikely that the impact will be a uniform one, argue Costas Milas, Tim Worrall, and Robert Zymek.

Numerous reports warn that Brexit may have negative effects on the UK stock market. But whatever the outcome, it seems unlikely that the impact will be a uniform one, argue Costas Milas, Tim Worrall, and Robert Zymek.

There have been a number of warnings that a vote to leave the European Union on 23 June may have adverse effects on the UK stock market, both from public institutions – such as the Treasury and the IMF – and private companies in the financial sector. These predictions suggest that Brexit would reduce the expected profitability of listed companies, causing the FTSE to drop.

Yet whatever the outcome of the referendum may spell for the stock market overall, it seems unlikely that the impact of the vote should be uniform across listed companies: some would surely be hit harder by the reality of Brexit, while others might even stand to gain. In a recently published research note, we attempt to determine which companies are viewed as relatively vulnerable to the economic impact of Brexit by stock market participants, and which companies are expected to profit more if the UK leaves the EU. We do so by analysing the behaviour of companies’ daily stock returns since the official announcement of the referendum date on 20 February.

Changes in “Brexit Sentiment”

We investigate which companies have tended to experience “abnormal” movements in their stock returns – that is, significant positive or negative movements in their returns relative to the market as a whole – in response to changes in the perceived likelihood of Brexit (“Brexit sentiment”). Changes in that likelihood are identified from the odds on Brexit offered in betting markets.

We use bookmakers’ odds as a measure of Brexit sentiment because i) daily data on the odds offered by a variety of bookmakers are readily available; ii) the referendum betting market has been very active; and iii) betting markets have been argued to provide a better prediction of electoral outcomes than polls both in the UK (as argued by David Bell) and elsewhere.

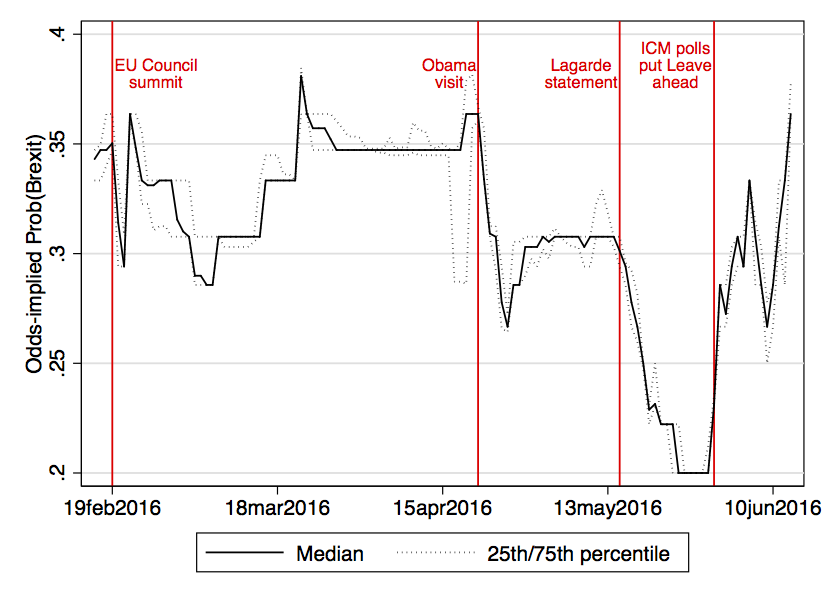

Figure 1 plots the evolution of the probability of Brexit implied in the Brexit odds offered by the median bookmaker, and the 25th and 75th percentiles of the distribution of bookmakers’ odds. The figure highlights that there have been significant changes in Brexit sentiment over time, with the odds-implied Brexit probability rising as high as 37 per cent in mid-March, and falling as low as 20 per cent in late May. It also shows very little evidence of “disagreement” between bookmakers.

What Do “Losers” and “Winners” look like?

Our methodology identifies 103 out of 618 companies from the FTSE All-Shares Index whose stock returns robustly display abnormal movements in response to changing Brexit odds. Out of these, 81 see their returns decline relative to the market as the likelihood of Brexit rises, marking them out as possible relative “Brexit losers”. The remaining 22 companies see their returns increase in the face of shortening Brexit odds, indicating that they might be potential relative “Brexit winners”. (A full list of these companies can be found in our paper.)

Using data on company characteristics, we then investigate what differentiates those companies the market views as “Brexit losers” from those it seems to regard as “Brexit winners”. Unsurprisingly, the share of companies in the former group reporting Europe as important overseas markets exceeds the share of companies in the latter group with major business in Europe by a factor of almost three (see Figure 2).

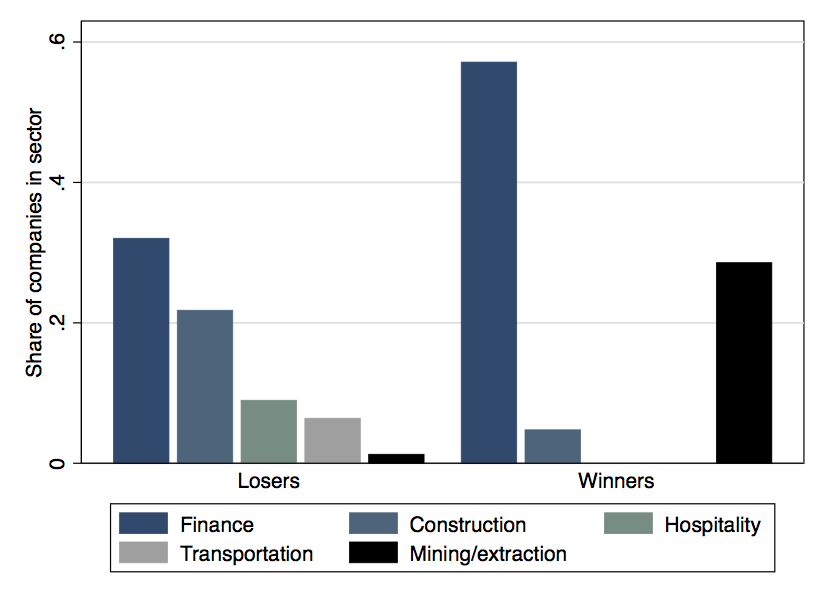

However, our findings also contradict two popular beliefs. First, contrary to the perception that “big business” benefits especially from continued EU membership, we find little difference between the median sizes of companies on the “losers” and “winners” side. Second, contradicting the notion that Brexit would hurt financial-services firms, 12 out of 22 likely “Brexit winners” are investment funds – most of which invest predominantly outside Europe. The remaining “Brexit winners” can be placed broadly in the mining and extraction sector, while the majority of the non-financial “Brexit losers” can be placed in the construction industry, hospitality services, and transportation services (see Figure 3).

However, our findings also contradict two popular beliefs. First, contrary to the perception that “big business” benefits especially from continued EU membership, we find little difference between the median sizes of companies on the “losers” and “winners” side. Second, contradicting the notion that Brexit would hurt financial-services firms, 12 out of 22 likely “Brexit winners” are investment funds – most of which invest predominantly outside Europe. The remaining “Brexit winners” can be placed broadly in the mining and extraction sector, while the majority of the non-financial “Brexit losers” can be placed in the construction industry, hospitality services, and transportation services (see Figure 3).

Our methodology cannot tell us how the outcome of Thursday’s vote will affect the stock market as a whole. But our findings do lead us to expect some re-shuffling in markets on Friday – irrespective of the result – as the stock prices of “losers” and “winners” adjust to the news. In the morning of 24 June our first look will be at the Electoral Commission website, to learn the voters’ verdict about the political future of the UK. Our second look will be at the stock market, to see how well our predictions have fared.

Costas Milas is Professor of Finance at the University of Liverpool.

Tim Worrall is Professor of Economics and Deputy Head of the School of Economics at the University of Edinburgh.

Robert Zymek is Lecturer in Economics at the University of Edinburgh.

Featured image credit: Metro Centric CC BY