John Van Reenen reacts to the news today that the UK has avoided economic contraction in the last quarter. Whilst Osborne may see this as cause to celebrate, there is nothing commendable about an economy that continues to stagnate. This news should not be taken as a sign to continue down the path of austerity. Rather, a policy change, starting with more public investment, is needed if the UK is going to recover.

John Van Reenen reacts to the news today that the UK has avoided economic contraction in the last quarter. Whilst Osborne may see this as cause to celebrate, there is nothing commendable about an economy that continues to stagnate. This news should not be taken as a sign to continue down the path of austerity. Rather, a policy change, starting with more public investment, is needed if the UK is going to recover.

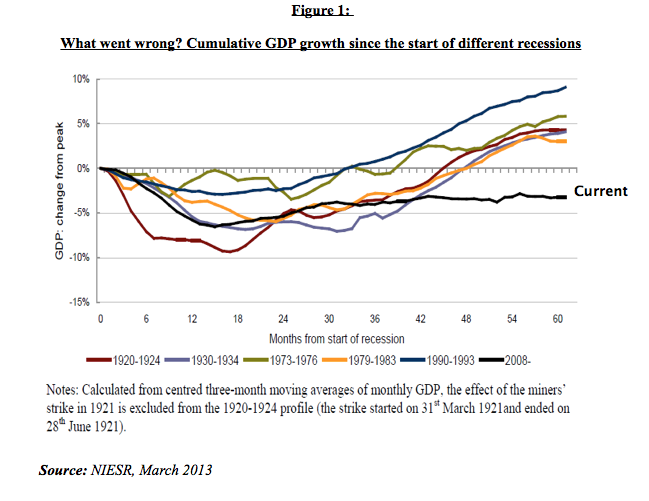

So it’s official: the Office of National Statistics says we are not in a “triple dip” recession as GDP growth was 0.3% in the first quarter of the year. And on Tuesday we found out that borrowing was down by £0.3bn. Newsflash! These are pathetic numbers. UK national income is still about 3% smaller than it was in 2008 and this has depressed tax revenues – which are why, incidentally, we can’t get the deficit down. The growth record is even worse than in the Great Depression even adding in the latest numbers (see Figure 1). We are bumping along the bottom when we should be growing strongly at this stage of the business cycle.

From Plan A to Grade D for Depression

The Chancellor launched his Plan A in 2010, a major fiscal consolidation to cut spending and raise taxes despite the worst global economic crisis in a generation. Unlike the Eurozone periphery (Portugal, Ireland, Greece, etc.), we were not forced to do this – we chose to do it. The UK embarked on a fiscal tightening even though interest rates were near zero, launching a major experiment in whether an anti-Keynesian macro policy would restore growth.

I was a sceptic and thought that the coalition government was cutting too much too fast. A medium-term consolidation was needed but not one that was so front-loaded when the UK and the rest of the developed world’s recovery was so wobbly. Other economists I respect took a different view and we argued the case out in public. Most of these initial supporters, however, have changed their minds. This is fine, as Keynes remarked: “When the facts change, I change my mind. What do you do, sir?”

And the facts have changed. Three years after the coalition came to power, it is clear that the grand experiment has failed. Even the citadel of fiscal rectitude, the International Monetary Fund, is now pleading with Chancellor to change course. As Jonathan Portes has noted, this is like the Pope telling you to get comfortable with being gay.

Various intellectual arguments have been advanced in favour of accelerated austerity. The contraction was said to be expansionary as people would realise that the future would look brighter without the government’s debt burden. Unfortunately this “confidence fairy” has refused to wave her economic wand – and probably never did. Contractionary policies are, err, really contractionary after all.

Then there was the “magic number” of a 90% debt-to-GDP ratio beyond which calamity lurked. Last week showed that this threshold was based on statistical errors. And finally there were the bond vigilantes who would send interest rates on government debt through the roof unless the deficit was drastically reduced. Well, interest rates on UK debt remain at historic lows despite credit agencies downgrades. So the Chancellor’s ideological shield is looking distinctly rusty.

Investment, Investment, Investment

A big part of the problem is that so much of the spending cuts have been at the expense of public investment, which is down about 40%. This is precisely the sort of spending that has a big “multiplier” effect on growth – you ‘crowd in’ a lot of private sector investment from government action. The overall size of the fiscal multiplier is also larger than we thought, especially during severe recessions, partly because interest rates are near zero.

What the Chancellor needs to do is get infrastructure spending going – roads, housing, schools, hospitals and a host of other transport and energy projects that were delayed or cancelled by the coalition. This would not even compromise his fiscal mandate to balance the deficit as such spending creates a public capital asset. It isn’t current spending like bumping up civil servants’ salaries. It makes a difference if you borrow to buy a house rather than borrow to go on holiday to Bermuda.

We can also help to cement these changes by pledging not just to invest more, but invest better. The LSE Growth Commission has proposed a new way of making infrastructure decisions that would unlock growth and reduce the policy risk that deters private sector investment.

It’s OK, there are more jobs than ever!

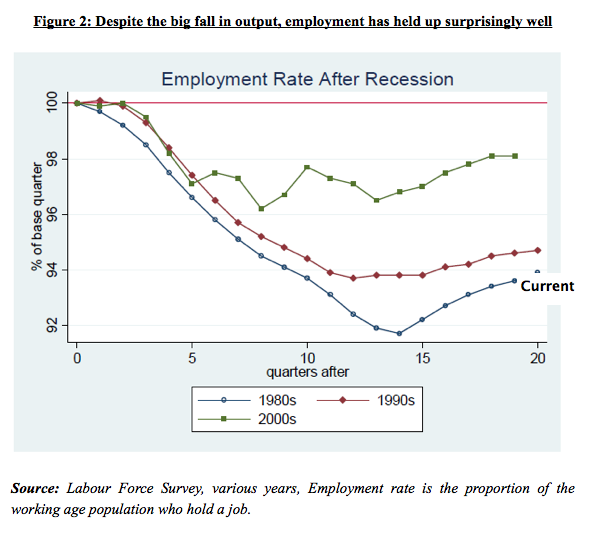

When pressed on our dire economic state, the Chancellor points to the relatively buoyant state of the labour market. We should not get too excited as the rising UK population has helped boost the absolute numbers of people employed. The proportion of the working age population in jobs is still down and unemployment has been stuck at just under 8% for many years, an unacceptable high level.

But it is true that jobs have held up better than anyone expected (see Figure 2) and better than in previous recessions. In part this is testament to the reforms made in the employment service by previous governments. Whereas in the 1980s recession, the government pushed many people onto incapacity benefits to massage down the claimant count numbers, there is now much more emphasis on keeping the unemployed looking for work.

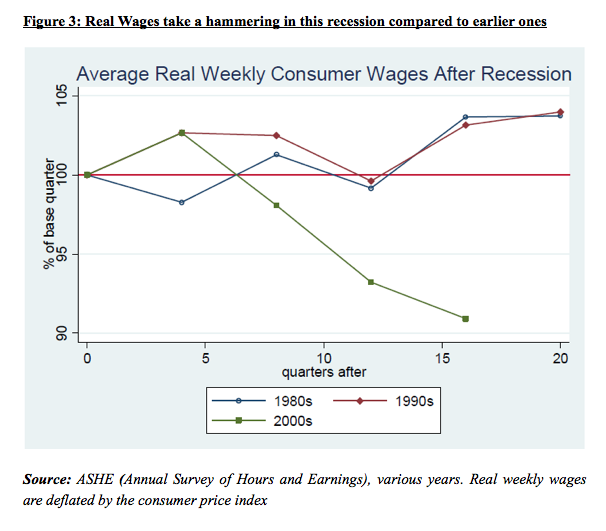

The main reason that unemployment is not even higher, however, is quite simple. Workers have been taking massive real wage cuts, falling by 8% in the four years after the middle of 2008 (see Figure 3). This is unprecedented for a post-war recession and has meant that employers have found it easier to keep them on because labour is relatively cheap. Some job is better than no job, but cuts in average income are nothing to boast about.

It’s not my fault

One refrain we often hear is that the cause of low growth isn’t the government’s fault. It’s because of our main trading partners in the Eurozone being in turmoil. The Chancellor is right that slow growth in the Eurozone is dragging down our export performance.

But what he fails to point out is that our European neighbours are following exactly the same policies of severe austerity as he recommends. It is true that many countries have little choice in the matter as there are forced to by the Troika and have no independent central bank, but Germany, for example, has no excuse for following the “austerian” medicine and seeking to prematurely balance the budget.

The politics are personal

The economics says we should clearly change course, but the conventional wisdom is that politics swings to a different rhythm. It is said that the coalition partners must stick to Plan A because their fate is so inextricably linked with its success. But surely adjusting the plan is better than being pulled into a Japanese-style lost generation and likely electoral defeat?

The politics is probably more personal. The Chancellor’s own political future is shackled to keeping the fiscal faith and not turning back. So he ploughs on, come what may. Maybe history will prove him right and he will become a future Prime Minister so his political strategy is sane. Certainly avoiding a “triple dip” takes some pressure off him after an awful week. But the continuing damage done to over 62 million UK citizens in falling incomes, over 2.5 million unemployed and a scarred generation of young people is an enormous price to pay for one man’s ambition.

Note: This article gives the views of the author, and not the position of the British Politics and Policy blog, nor of the London School of Economics. Please read our comments policy before posting.

John Van Reenen is Director of the Centre for Economic Performance and a Professor at the London School of Economics

This assumes that economic growth should be a goal of any country – weren’t we talking about reducing consumption for many years due to man’s effect on the environment? Now that people are struggling to pay their Sky subscriptions they don’t like environmentalism anymore. People in the UK are still far better off than the vast majority of people in the world.

I see some strong evidence of poor economic performance for the UK, the effect in your story, but nothing on the cause (you ascribe it to inappropriate fiscal policy). What chart would you say best demonstrates the misguided path of fiscal policy….I know the government talks a lot about austerity, but have never seen decent evidence they are practicing what they preach..

The other imperative, besides personal ambition, is the collective wish of his party to downsize the state and this is more important than even the economic health of the nation. Unfortunately the successful spin on the austerity policy and TNA mean that anyone suggesting an alternative course of action is regarded by much of the population as economically illiterate!!