Recent decades have seen a massive economic shift from manufacturing to service industries. But how much of this structural transformation is a shift in organisational boundaries, in which work that was previously done within manufacturing firms is now outsourced to specialised service providers? Giuseppe Berlingieri looks at changes in the US economy over the past 60 years.

Recent decades have seen a massive economic shift from manufacturing to service industries. But how much of this structural transformation is a shift in organisational boundaries, in which work that was previously done within manufacturing firms is now outsourced to specialised service providers? Giuseppe Berlingieri looks at changes in the US economy over the past 60 years.

We are constantly told that we live in a service economy. Over the past few decades, the reported share of services in the economy has certainly experienced a sharp increase in most countries. In the United States, the service sector today accounts for more than 83% of total employment, a considerable increase from its share of 60% in 1947. On the other side of the coin is the widely lamented decline of the manufacturing sector.

But what if both sides of this ‘structural transformation’ of the US economy can in part be explained by the domestic outsourcing of service inputs – for example, manufacturing firms outsourcing work on their annual tax returns to specialised accounting firms? In recent research, I analyse the production side of the economy and the role of firms in shaping the reallocation of labour across sectors.

In particular, I focus on two relatively unexplored mechanisms that can help to explain the rise of services and the fall of manufacturing: first, changes in the composition of intermediate inputs, the goods or services that are used in producing final outputs (for example, tyres bought by car manufacturers or accounting and cleaning services used by most firms); and second, changes in how those intermediate inputs are sourced domestically. I use the standard definition of outsourcing as ‘the acquisition of an intermediate input or service from an unaffiliated supplier’.

What is driving the rise of the US service sector?

Most explanations of structural transformation focus on final demand, with one of the central ideas being that when societies become richer, they prefer to consume more services (see Herrendorf et al, 2013, for a review of this body of research). But two basic facts that emerge from a simple analysis of US industry data suggest that final demand is not the only driver of the rise of services.

First, three industries – finance; real estate; and professional and business services – account for a very large share of the growth of the service sector. The last category includes accounting, engineering, consulting and legal services as well as less skilled work such as security, maintenance and janitorial services. Second, these industries are highly specialised in the production of intermediate inputs, with firms rather than individual consumers demanding the goods and services they provide.

In particular, professional and business services have increased their share in total employment by 9.2 percentage points, accounting for roughly 40% of the total growth of the entire service sector, the biggest contribution among all industries. Moreover, 91% of the output of this industry is sold to firms as intermediate inputs or used for investment, compared with 53% for the economy as a whole. Final consumption and net exports account respectively for just 7% and 2% of the sector’s output.

A changing input-output structure

The specialisation of the professional and business services industry in intermediate production combined with its strong growth is reflected in a parallel change in the input-output structure of the economy. This can be analysed using ‘total requirements’ tables, which show the inputs required from all industries in the economy to produce a dollar of output of a certain commodity. The transactions captured in the tables include indirect inputs (those purchased from a certain industry via a third industry) as well as direct inputs. The main change in the US economy between 1947 and 2002 was a significant increase in the use of professional and business services in the production of all other commodities, and to a smaller extent an increase in the use of finance.

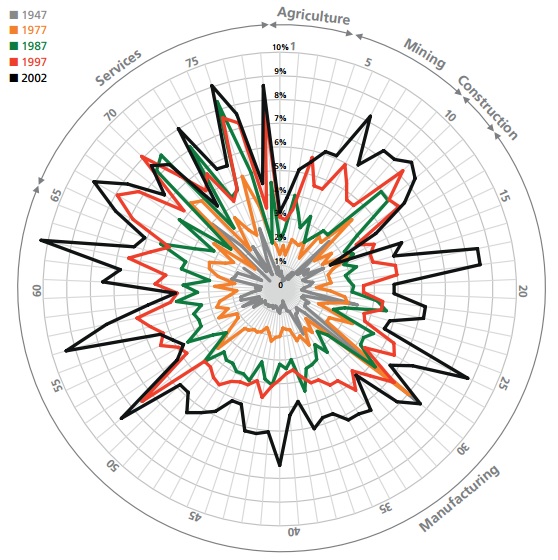

Figure 1 shows for all commodities in the economy the increase in the share of professional and business services in total requirements. Summing up this share over all commodities (around each circle) gives the ‘forward linkage’, a measure of the interconnection of a sector to all other sectors through the supply of intermediate inputs. A sharp rise in the forward linkage of professional and business services implies that the industry has greatly increased its influence on the rest of the economy.

Figure 1: The total use of professional and business services (PBS) in the US economy, 1947-2002

Note: This figure displays, for each year, the share of PBS in the total requirements of all commodities.

Note: This figure displays, for each year, the share of PBS in the total requirements of all commodities.

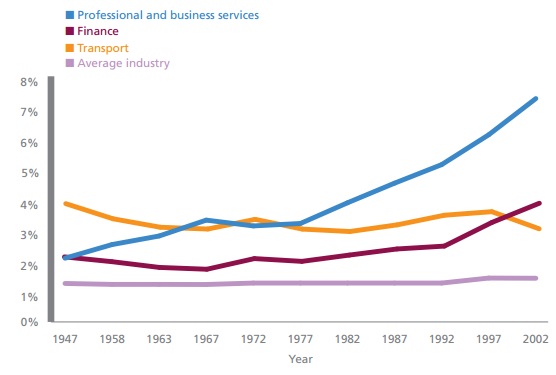

Figure 2 shows the evolution of the average forward linkage for a selection of industries. Professional and business services have become the industry with the biggest influence on the rest of the economy, overtaking industries with traditionally high forward linkage, such as transport (industry 65 in Figure 1), and overshadowing fast growing industries, such as finance.

Figure 2: Average forward linkage over time for selected industries

Note: This figure plots, for each industry, the total forward linkage divided by the number of commodities. In a given year, the share displayed for PBS is the average along a circle of Figure 1

Note: This figure plots, for each industry, the total forward linkage divided by the number of commodities. In a given year, the share displayed for PBS is the average along a circle of Figure 1

Structural change: the role of intermediate inputs and outsourcing

My study looks at the changes in demand for intermediate inputs in a simple growth accounting model that captures the fully-fledged input-output structure of the US economy. In this setting, not only do sectoral labour shares depend on consumption shares as in a standard value added model, but also on the input- output structure of the economy. For example, employment in the accounting sector depends on household demand for accounting services as well as demand from firms.

Changes in demand for intermediate inputs therefore induce a reallocation of labour across sectors. I find that when final demand is kept constant over time, the evolution of the input-output structure of the economy alone accounts for 33% of the total increase in service employment and 22% of the fall in manufacturing.

What drives the changes in the use of intermediate inputs over time? One of the key forces is outsourcing. The intuition is simple: if a manufacturing firm outsources part of its headquarter services, the intermediate use of services will increase because it is likely that these inputs will be purchased from firms specialising in services.

Given the high share of intermediate production and the high substitutability that characterises professional and business services, previous research usually identifies the rise of this industry as an increase in outsourcing. I take a similar approach and improve on it by controlling for production within the boundaries of the firm.

In principle, input-output data do not clearly distinguish the boundary of the firm. But in the case of professional and business services, most in-house production is classified in auxiliary units (that is, headquarters, which include administrative, accounting, legal services, etc.), which can be excluded. I then quantify how much of the change in intermediate use is due to the outsourcing of professional and business services with a simple counterfactual exercise, which fixes the demand for professional and business services to its 1947 level and keeps it constant over time.

I find that had firms produced all of their professional and business services in-house, the employment share of the service sector would have been 3 percentage points smaller, which is equivalent to 14% of the total increase in the share of services. On the other hand, the share of manufacturing would have been 2.9 percentage points larger, accounting for 16% of its fall.

The focus on professional and business services is justified by their importance and by the fact that I can correctly account for outsourcing. But note that many other services have been outsourced over the period, and these percentages could therefore be a lower bound, especially in more recent years.

A ‘servitisation’ of manufacturing? Evidence from occupational data

A potential concern might be that overall service activity has increased both outside and inside the firm. Yet a deeper analysis of industry data shows that most of the transactions take place across the boundaries of firms, and they are not matched by a parallel increase of services produced inside firms. Table 1 shows that the share of total employment accounted for by auxiliary units is remarkably constant over time, and cannot explain the increase in the share of professional and business services.

Table 1: Professional and business services (PBS) – share of total employment

Moreover, an analysis of data that classify workers by both their occupation and industry shows that, to a first approximation, the overall composition of professional and business services has not changed over time. This result supports the view of organisational change with a reallocation of activities across the boundaries of the firms.

Moreover, an analysis of data that classify workers by both their occupation and industry shows that, to a first approximation, the overall composition of professional and business services has not changed over time. This result supports the view of organisational change with a reallocation of activities across the boundaries of the firms.

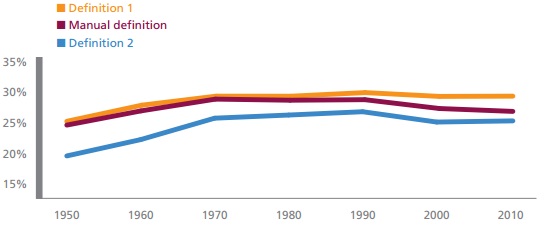

I select a list of occupations employed in the professional and business services industry (‘PBS Occupations’) and plot their share in total employment over time. Figure 3 shows that their share has been almost constant. According to the baseline definition (Definition 1), the share of workers classified within PBS Occupations went from 24.2% of total employment in 1950 to 28.2% in 2010, but it has been essentially flat from 1970 onwards. It is in the second half of the period that outsourcing has played a much more important role, as Table 1 shows.

Figure 3: Share of PBS Occupations in total employment

Notes: Definitions 1 and 2 select the occupations that have at least 9% or 10% of their workers employed in PBS. In the Manual definition, occupations are handpicked on the basis of their job description.

Notes: Definitions 1 and 2 select the occupations that have at least 9% or 10% of their workers employed in PBS. In the Manual definition, occupations are handpicked on the basis of their job description.

So professional and business services increased more sharply in a period when the share of workers classified within PBS Occupations was constant. Given the rising share of the professional and business services industry in total employment, we would expect workers to move to specialised professional and business services firms, or at least for these firms to employ disproportionately more workers over time.

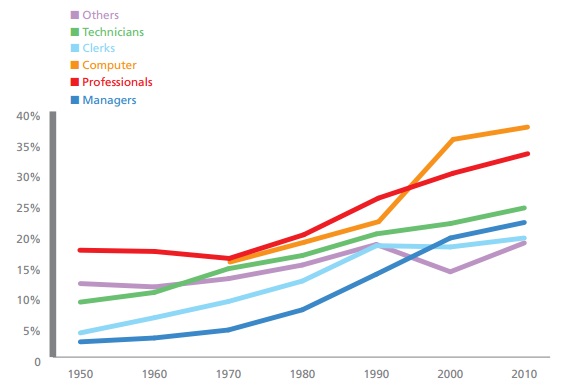

This is precisely what has happened. The share of workers within the selected PBS Occupations employed in manufacturing has fallen over time, while the share employed in the professional and business services industry has risen. Figure 4 shows the latter share for six aggregate categories of PBS Occupations. Despite the fact that the total share of PBS Occupations has been roughly constant over time, there was some heterogeneity across these six main categories.

Figure 4: Main categories of PBS Occupations – share of workers within occupation employed in the PBS industry

Having analysed these patterns in more depth, I find suggestive evidence about other changes. For example, outsourcing might not take place through the mere substitution of the very same task from inside to outside the firm, but it could entail the substitution of an old superseded task with a new, more technologically advanced one. In this sense, outsourcing could be a way of accessing new technologies that would be too costly to produce in-house.

One example would be the substitution of computer specialists employed in specialised services firms for clerks employed internally. At the same time, the share of workers in the PBS occupation of professionals has also risen over time, suggesting an increase in the need for specialised knowledge.

These findings have two significant implications. First, from the demand side, manufacturing is still more important than the simple industry data suggest: thanks to intermediate consumption, the demand for manufacturing goods triggers higher output in many upstream sectors.

Second, services have become much more important from a supply point of view, a point that does not seem to be sufficiently appreciated in policy discussions. Given the intermediate nature of many services, they have a very high influence on the productivity of downstream sectors. Efficient professional and business services are nowadays of paramount importance for most countries. Lamenting the decline of manufacturing misses the fact that future growth and export competitiveness will depend more and more on the service sector. So for example, in the European context, a single market for services cannot wait any longer.

This article originally appeared in the Winter 2013/2014 issue of CentrePiece, the magazine of the Centre for Economic Performance (CEP) at LSE, and summarises ‘Outsourcing and the Rise in Services’, by Giuseppe Berlingieri, CEP Discussion Paper No. 1199.

Featured image credit: arbyreed (Creative Commons BY NC SA)

Please read our comments policy before commenting.

Note: This article gives the views of the authors, and not the position of USApp– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/OyFgy9

_________________________________

Giuseppe Berlingieri – LSE Centre for Economic Performance

Giuseppe Berlingieri is a research associate at CEP. His research focuses on international economics, organizational economics, and macroeconomics

Very insightful. Yet, lamenting the decline of manufacturing has a great deal to due with declining real wages associated with a shift in employment to the retail sector where wages are low and working hours erratic. Yes, the business and professional service sectors are growing; however, many who were once employed in high wage manufacturing are faced with falling real wages and deteriorating working conditions in the retail sector where many are now employed. Consider examining the structure and scope of the retail sector compared to the manufacturing sector.