João Paulo Pessoa analyses the impact of China’s share in world trade on other countries’ jobs and wages.

João Paulo Pessoa analyses the impact of China’s share in world trade on other countries’ jobs and wages.

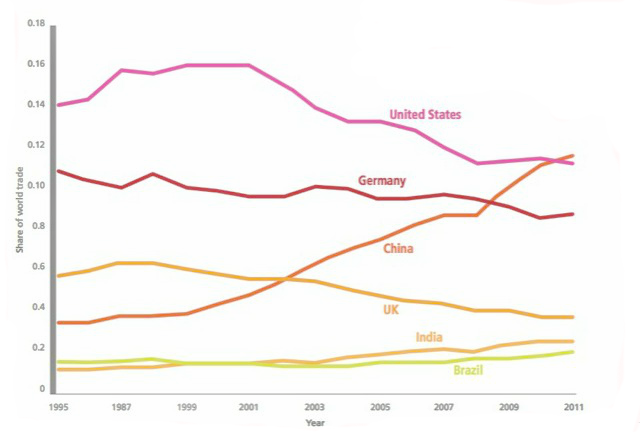

China recently surpassed the United States as the country with the largest share of world trade in goods – see Figure 1. This boom in trade with China has led to much concern about the losers from rising import competition in manufacturing. In Donald Trump’s US presidential campaign, for example, he has continuously complained about the Chinese: ‘They’re stealing our jobs; they’re beating us in everything; they’re winning, we’re losing.’

So how do the people of high-wage countries fare when integrating with low-wage economies like China? Is Trump’s statement correct? Is China harming all British and American citizens? Well, not really.

Figure 1 – Share of world trade by country

Note: The figure shows the share of world trade by country over time. Share of world trade is define as exports plus imports by country divided by total imports plus total exports in the world. Source: World Input Output Database.

Winners and losers

Economists have long known that greater openness to trade is likely to be beneficial over the longer run – by reducing prices and allowing countries to expand their production to new markets. But there are also important changes in the labour market that take place during the process of adjustment to increased trade, such as the displacement of workers in sectors harmed by imports, and workers not immediately moving to growing exporting sectors.

To assess the effect of more trade with China on developed economies, I use a state-of-the-art quantitative model of the global economy. The model incorporates important channels through which trade affects individuals in a country, providing a mapping from trade data to the benefits for society as a whole.

In the model, consumers benefit from more trade integration by getting access to imported goods at lower costs. But at the same time, a rise in import competition in a sector can lead to lower wages and higher unemployment. Moreover, it is going to be costly for displaced workers to move across sectors: they may prefer to work in their old industry as it is located in a place where they own a property or their family members are settled.

To analyse how all these effects interact following a ‘trade shock’, I use numerical simulations, together with several data sources. I look at six countries/regions in the World Input Output Database: China, the United States, the UK, the European Union, the ‘rest of the world developed’ (Australia, Japan, Canada, South Korea and Taiwan) and the ‘rest of the world developing’ (Brazil, India, Indonesia, Mexico, Turkey and Russia). I also aggregate the economy into five sectors: services, low-tech, mid- tech and high-tech manufacturing, and energy and others.

The ‘China shock’ used in my analysis consists of a decrease in trade barriers between China and the rest of the world and an increase in Chinese productivity in all sectors except services. These changes correspond to a growth of 64 per cent in China’s share of world exports, a magnitude not very different from the figure of 65 per cent reported in the World Input Output Database for the four-year period from 2000 (the year before China joined the World Trade Organization).

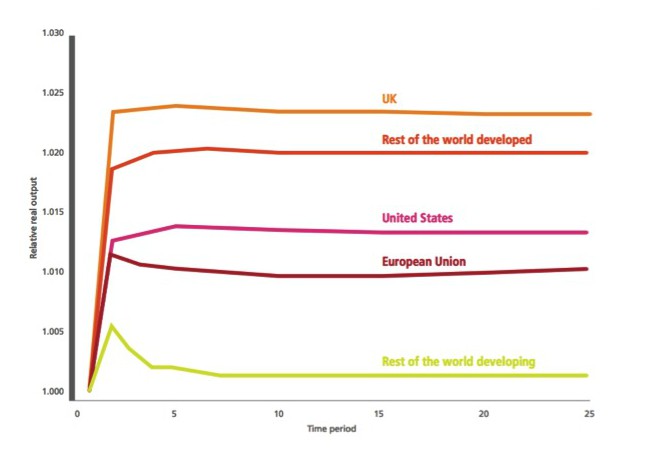

Figure 2 shows the evolution of real income per capita (or real consumption per capita) for countries or regions over the years following the fall in trade costs and productivity gains in China, which take place in period 1. Income instantly increases in all countries, either because they are able to export more to China or because consumers in these countries have access to cheaper goods.

Figure 2 – World real income

Note: Transition path following an unanticipated fall in trade costs between China and the rest of the world and a rise in Chinese productivity in all sectors apart from services. Real income relative to the income in period 1. Source: Author’s calculations from several data sources.

Moreover, these gains are sustained over time. For example, real consumption in the United States and the UK increases by approximately 1.3 per cent and 2.3 per cent respectively, in the long run. Naturally, Chinese citizens experience large income gains: more than 23 per cent (not shown in Figure 2).

Does this mean that all individuals gain in all countries? Not necessarily. The effects of the China shock on wages and unemployment vary substantially across sectors within countries. In low-tech manufacturing industries in the United States and the UK, which face severe import competition from China, workers’ real wages fall and unemployment rises.

The fall in the real average wage in this sector is approximately 1.6 per cent in the United States and 0.7 per cent in the UK five years after the shock.

But at the same time, workers in the services sector experience a rise in the real average wage and no significant change in the unemployment rate: the real average wage in services increases by approximately 1.9 per cent in the United States and 2.5 per cent in the UK.

The dynamics associated with the rise of China are particularly striking. Immediately after the shock, wages rise in exporting sectors and fall in industries facing competition from China. As workers move from sectors hit badly by China in search of better-paid jobs in other industries, wages in exporting sectors start to fall due to the arrival of new workers searching for jobs. This implies that wages are lower in the long run than in the short run in these industries. In some import-competing sectors, however, the effects go in the opposite direction: wages fall immediately after the shock and recover over time.

I also test some predictions from the model using UK data at a much more disaggregated industry level. By analysing the period between 2000 and 2007 (the year before the Great Recession), I find that UK workers initially employed in industries that suffered from high levels of import exposure to Chinese products earned less and spent more time out of employment compared with individuals that were in industries less affected by imports from China.

I also find that low-skilled workers experienced higher employment losses than high-skilled ones. Of course, these are only negative relative effects (across sectors) of Chinese imports on UK workers and do not imply that China harmed UK citizens overall. Indeed, the results from the model suggest that China is far away from being this sort of villain.

Policy implications

The results raise important policy questions. The first point is that even when developed economies face a fierce competitor like China, they also receive many benefits. This implies that any policy aiming to restrict trade in the name of more protection for workers should be reconsidered.

At the same time, the trade shock does generate winners and losers in the labour market. Hence, it may be beneficial to find a way to compensate the people who lose out, and let the adjustment take place without any type of intervention that hinders trade.

It is important to bear in mind that the gains from trade are likely to be greater in reality than the ones presented in my study, which does not include several channels associated with trade that could lead to additional improvements in incomes. These include access to cheaper inputs, immigration, greater intensity of research and development, and vertical production chains.

This post appeared originally at LSE Business Review, and is based on an article which appeared originally on CentrePiece, the magazine of LSE’s Centre for Economic Performance (CEP), based on International Competition and Labor Market Adjustment, CEP Discussion Paper No. 1411

Featured image credit: Trey Ratcliff (Flickr, CC-BY-NC-SA-2.0)

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of USAPP– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/29FVQsE

_______________________________

João Paulo Pessoa – São Paulo School of Economics

João Paulo Pessoa is an assistant professor at the São Paulo School of Economics at Fundação Getulio Vargas and a research associate in CEP’s growth programme.