Business groups constitute a common way for ultimate owners to exercise control over a large number of companies while containing their risk exposure to different parts of the business through limited liability. In countries with underdeveloped financial infrastructures, these groups overcome difficulties in accessing external finance by reshuffling funds within the corporate structure.

Group bankruptcies tend to be large (e.g., Global Crossing, Maxwell, MG Rover, Parmalat) and to affect a significant number of stakeholders. These bankruptcies can be extremely complex, especially if the group’s assets are spread over multiple jurisdictions. The nature of the group’s structure and operations may affect the parent’s liability in the event of one of its subsidiaries’ insolvency. As a consequence, this affects the likelihood of transfers of resources from other parts of the group to that specific subsidiary as it approaches financial distress. These “internal capital market” transfers will shape the way bankruptcy takes place within the group.

Group bankruptcies tend to be large (e.g., Global Crossing, Maxwell, MG Rover, Parmalat) and to affect a significant number of stakeholders. These bankruptcies can be extremely complex, especially if the group’s assets are spread over multiple jurisdictions. The nature of the group’s structure and operations may affect the parent’s liability in the event of one of its subsidiaries’ insolvency. As a consequence, this affects the likelihood of transfers of resources from other parts of the group to that specific subsidiary as it approaches financial distress. These “internal capital market” transfers will shape the way bankruptcy takes place within the group.

In our research “Bankruptcy in Groups,” we seek to understand how financial distress takes place within a business group. Our analysis is based on a large cross-country sample of (bankrupt and non-bankrupt) group-affiliated firms spanning the years 2005 to 2012. The data come from Orbis, a database published by Bureau van Dijk electronic Publishing (BvDEP).

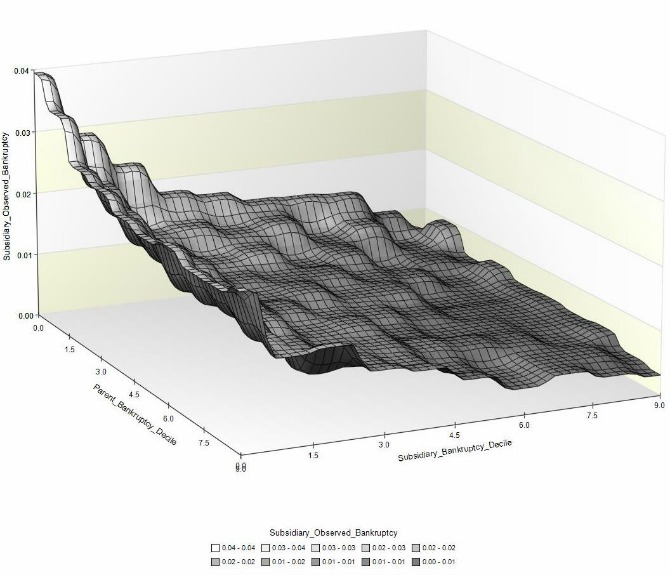

We first show that group structure matters for parent and subsidiary bankruptcy prediction. In line with this finding, the picture below shows how average subsidiary bankruptcy rates change by decile of subsidiary and parent probability of bankruptcy.

The traditional bankruptcy prediction models can be improved by incorporating group structure information. Parents may be required to support financially distressed subsidiaries as a result of explicit or implicit agreements. Absent these agreements, parents might also have an incentive to support financially distressed subsidiaries as the bankruptcy of a subsidiary may impose severe costs, e.g., reputational damage, cross-default, and direct liability under veil piercing (judicially imposed exceptions to the general principle that corporations are legal entities separate from their shareholders, officers and directors, i.e., limited liability.) Intra-group support can also flow in the opposite direction, as distressed parents may seek financial aid from healthy subsidiaries.

We develop predictions regarding the strength of association of intra-group bankruptcy probabilities in settings with higher likelihood of parental support (i.e., propping) or negative intervention (i.e., tunnelling – any wealth transfer from a subsidiary to a high-risk parent to prevent its bankruptcy). We develop these predictions based on the indicators of group integration typically considered in the decision to pierce the veil in bankruptcy proceedings that may affect the likelihood of group contagion effects. In particular, we measure parent-subsidiary integration along five different dimensions: (1) control rights; (2) shared name; (3) board interlock; (4) industry overlap; and (5) geographical proximity.

Our study shows that the association between parent and subsidiary default probabilities varies with the level of subsidiary integration within the group and country-level institutional quality. Propping is more prevalent if the subsidiary is named after its parent and if parent and subsidiary have interlocked boards. Our findings further indicate that parents are less likely to tunnel when subsidiaries are domiciled in countries with stricter anti-self-dealing laws, stronger investor protection regulation, higher director litigation, and tighter approval and disclosure of related party transaction requirements.

We conduct a number of tests to ensure that at least part of the documented association in intra-group bankruptcy probabilities is attributable to transfers between group firms as they approach financial distress:

- First, we run a set of “placebo tests” in which we replace group firms with standalone firms in the same country and industry. These placebo tests mitigate the concern that the association between parent- and subsidiary- bankruptcy probabilities could be purely driven by common country-industry level factors.

- Second, we document increased intra-group loans within the propping and tunneling sub-samples.

- Third, we examine how a sovereign rating downgrade (a shock to the parent’s credit risk that is exogenous to subsidiaries’ bankruptcy risk) propagates to subsidiaries within the group. We find that this shock is less likely to propagate to subsidiaries in countries with strong anti-self-dealing, investor protection, director liability and related-party transaction regulations.

Our findings are relevant for financial reporting regulators, auditors, investors and credit rating agencies, and speak to the regulatory debate on cross-border insolvency.

♣♣♣

Notes:

- This article is based on the authors’ paper Bankruptcy in Groups, a Stanford University Graduate School of Business Research Paper.

- The post gives the views of its authors, and not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Rae Allen CC-BY-2.0 Inside photo:David Merrett CC-BY-2.0

William H. Beaver is the Joan E. Horngren Professor of Accounting, Emeritus at Stanford University Graduate School of Business. He is widely recognized for his innovative research on how accounting information in corporate financial statements affects security prices. He was among the first to investigate financial ratios as predictors of business failure. His recent work has centered on public policy issues connected with government regulation of corporate financial disclosure.

William H. Beaver is the Joan E. Horngren Professor of Accounting, Emeritus at Stanford University Graduate School of Business. He is widely recognized for his innovative research on how accounting information in corporate financial statements affects security prices. He was among the first to investigate financial ratios as predictors of business failure. His recent work has centered on public policy issues connected with government regulation of corporate financial disclosure.

Stefano Cascino is an Assistant Professor of Accounting at the London School of Economics. He received in PhD in Accounting from the University of Naples Federico II. His primary research interests include international disclosure regulation, corporate governance and credit markets. His research appears in major accounting journals such as Review of Accounting Studies and has generated the interests of practitioners and standard setters. He is a member of the editorial board of Accounting and Business Research.

Stefano Cascino is an Assistant Professor of Accounting at the London School of Economics. He received in PhD in Accounting from the University of Naples Federico II. His primary research interests include international disclosure regulation, corporate governance and credit markets. His research appears in major accounting journals such as Review of Accounting Studies and has generated the interests of practitioners and standard setters. He is a member of the editorial board of Accounting and Business Research.

Maria Correia is an Assistant Professor of Accounting at the London Business School. She received her PhD in Accounting from Stanford University. Her research interests are in the area of default prediction and credit markets, and enforcement and securities litigation. She is the recipient of the Best Paper Award at the 2011 Review of Accounting Studies Conference and her papers are published in leading accounting journals such as Journal of Accounting and Economics and Review of Accounting Studies. She is a member of the editorial board of European Accounting Review.

Maria Correia is an Assistant Professor of Accounting at the London Business School. She received her PhD in Accounting from Stanford University. Her research interests are in the area of default prediction and credit markets, and enforcement and securities litigation. She is the recipient of the Best Paper Award at the 2011 Review of Accounting Studies Conference and her papers are published in leading accounting journals such as Journal of Accounting and Economics and Review of Accounting Studies. She is a member of the editorial board of European Accounting Review.

Maureen F. McNichols is the Marriner S. Eccles Professor of Public and Private Management at Stanford University Graduate School of Business. Her leading research in two key areas — on earnings management and its implications for investors; and on analysts’ incentives, forecasts, and investment recommendations — has received considerable attention from academics, investors, and regulators in recent years. Her papers appear in the leading journals in accounting and finance and have garnered several Best Paper awards.

Maureen F. McNichols is the Marriner S. Eccles Professor of Public and Private Management at Stanford University Graduate School of Business. Her leading research in two key areas — on earnings management and its implications for investors; and on analysts’ incentives, forecasts, and investment recommendations — has received considerable attention from academics, investors, and regulators in recent years. Her papers appear in the leading journals in accounting and finance and have garnered several Best Paper awards.