International investment has gained popularity in the past two decades. Both the number of international mutual funds and assets under management have increased dramatically. These funds enable households to enjoy the diversification benefits and return opportunities provided by international markets. However, despite their increasing popularity, little is known about their investment behaviours in international financial markets: How do they allocate assets across country/region and industry? What are the performance implications of their investment in different regions and industries? What drives their investment decisions?

A natural option for mutual fund managers is to diversify the portfolio. Based on classical finance theory, investors should hold diversified portfolios to achieve the best return-risk profile. However, in practice, mutual fund managers, as professional money managers, may choose to hold concentrated portfolios for a couple of reasons. First, they may invest heavily in stocks that they have private information about (or, information advantage over other investors). Second, they may take high risks by betting on the future performance of (hence concentrating on) a small number of stocks, probably because of competition pressure from other fund managers to outperform. Finally, they may concentrate their portfolios on some stocks because of familiarity – a behavioural bias. Among these three alternative explanations, only the private information explanation predicts a positive relation between portfolio concentration and fund performance. Previous studies on domestic investment have found more evidence in favour of the private information story than the other two.

Investment in international markets adds an additional layer of complexity to the diversification versus concentration debate, with two dimensions to diversify (or concentrate in): country (region) and industry. When allocating assets in international markets, investors may have two different approaches: first diversify across countries and then select stocks within each country; or first diversify across industries then select stocks within each industry. On the other hand, if private information breeds portfolio concentration, fund managers may concentrate on either countries or industries, depending on their private information set.

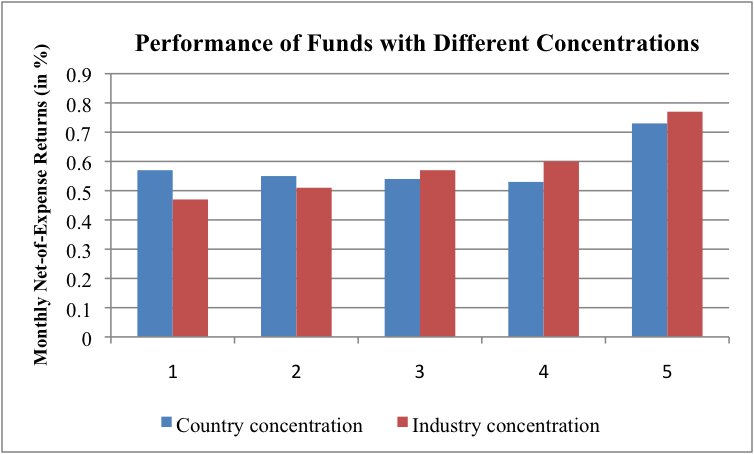

In our research, we study how international mutual funds invest in country and industry dimensions and the performance implications of their investment decision. Our sample includes international equity mutual funds domiciled in the U.S. We sort funds into five groups based on their concentration levels in country and industry respectively. Group one includes funds with the most diversified portfolios while group five with the most concentrated ones. The figure below shows the average performance of the five fund groups when they are sorted by country concentrations (blue bars) or industry concentrations (red bars). In both country and industry dimensions, the most concentrated funds (group five) outperform their diversified counterparts (group one). If anything, the differing performances in industry-concentration groups are monotonic and more evident. This finding supports the private information story in international equity mutual funds.

Funds’ concentrations on country and industry can be positively correlated. This is not surprising given the various industry structures of each country. Next we differentiate country versus industry concentration as the main driver of the outperformance of the concentrated funds. This test is specific to international markets and is our more significant finding. We find that among country-concentrated funds, those that are also industry-concentrated still outperform the industry-diversified ones. In contrast, among industry-concentrated funds, those that are also country-concentrated do not outperform country-diversified ones. In other words, we show that industry concentration (rather than country concentration) is the main driver of the outperformance of concentrated funds. The observed portfolio concentration on country seems an artefact of its concentration on industry.

Furthermore, we find that industry-concentrated funds show good predicting ability of future industry returns. The industries they buy outperform the industries they sell in the one-year period following the trade. Finally, we find that industry-concentrated funds rotate industries less frequently than diversified funds. The evidence supports the notion that some fund managers have information advantage on certain industries in international markets and they try to maximize their superior information by holding industry-concentrated portfolios.

Out paper investigates the investment decisions of U.S. international equity mutual funds and finds that some fund managers have private information on industries. They profit from their information advantage. The questions left for future studies may be whether the findings can apply to fund managers in other countries and more importantly, what are the sources of the information advantage of the fund managers.

♣♣♣

Notes:

- This article is based on the authors’ paper Country and industry concentration and the performance of international mutual funds, in the Journal of Banking & Finance, Volume 59, October 2015, Pages 297–310.

- This post gives the views of the authors, and not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Andreas Poike CC-BY-2.0

Takato Hiraki is Professor of Finance at Tokyo University of Science. His research interests include global risk premia analysis; investment management (Japanese mutual funds; market efficiency); fixed income; asset pricing and market microstructure; corporate finance (governance; restructuring and M&A, real options and IPOs); behavioural finance (home and local bias); and international art.

Ming Liu is Professor of Finance at the International University of Japan. His current research interests include market efficiency, international investment and mutual funds.

Xue Wang – is an Assistant Professor of Finance at the Renmin University of China. Her research interests centre on market anomalies, market frictions, and international finance.

1 Comments