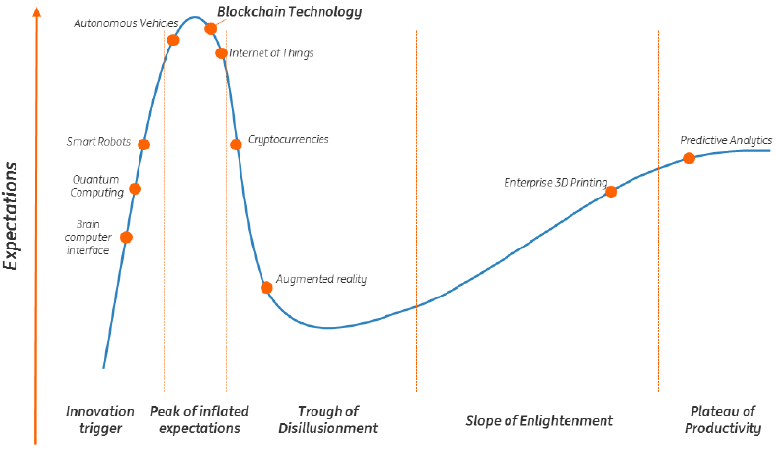

If we look at the Gartner’s “Hype Cycle for Emerging Technologies”, the rapid ascent to peak expectation, before the equally swift fall into the trough of disillusionment, for a lot of hot new technologies is hard and fast. But for blockchain, we are still teetering at the tipping point, as we have been for a while now, as the industry awaits the confirmation that distributed ledger technology is really going to revolutionise financial services.

Figure 1. Gartner’s hype cycle for emerging technologies

Source: Gartner 2015 (not all technologies incorporated in the graph)

We have seen an encouraging amount of testing and innovation, but there has yet to be a big breakthrough moment. That doesn’t mean that the technology doesn’t have the potential to be ‘as big as the buzz’, even if it’s more of a blockchain evolution, rather than revolution.

There is still a huge potential for blockchain applications to have a transformative effect in a variety of areas, including securities and trade settlement, internal transacting, e-identity and also as a backbone for connected devices. Anywhere where there are complicated exchanges, numerous information flows, or a large number of parties involved, it can theoretically simplify the incumbent business model, reduce costs and speed up performance.

However, there must be a very clear business care for employing new technologies. As I mentioned in a research paper, blockchain is not “the thing” – it is “the thing that enables the thing” and we therefore need to see clear value, before we begin overhauling the financial sector’s well established infrastructure. At the moment, we are still very much in the experimental stage and in the near future we expect to see a roll-out of short-term focused solutions, which will evolve into more integrated and complex pieces of technology, where there is clear evidence of value.

One thing that is clear is that industry collaboration will be the driver behind any blockchain success. The proverbial arms race for the best product or process to give one institution a leg-up over rivals will not be how the blockchain story plays out. Instead, co-operation, collaboration and the sharing of information between market players and other relevant bodies will be pivotal to success.

Industry collaboration is key: the more players there are at the table, the greater the noise and ultimately, this will amplify industry impact. But (and perhaps more importantly) collaboration will lead to standardisation. This will be significant when it comes to cost reduction and quality improvement as the shared technology and standards will provide a stronger platform for scalable transformation and adoption.

It is for this reason that ING joined the R3 Consortium, which is ‘focused on building and empowering the next generation of global financial services technology’. The group (which consists of around 40 banks), has trialled a number of successful blockchain technologies across different areas, including a platform powered by Intel Corp technology for bond transactions. The Consortium believed the trial “marked an unprecedented scale of institutional collaboration between the financial and technology communities exploring how distributed ledgers can be applied to global financial markets”.

There are also a wide number of use cases being explored in the payments sector, where an industry-wide payments and settlement infrastructure that is based on trust, cryptography and transparency would help solve a number of the current market problems. Here, the technology could be the catalyst for a number of much needed improvements: lower transaction and operational costs, increased processing speed, risk reduction, transparency, and traceability.

However, the ability of blockchain to disrupt the payments landscape does not automatically change the requirements for banks – much of the current infrastructure is in place because it complies with current regulation. For blockchain to have an impact, it will need to meet the many differing needs and requirements of the regulators, banks, other market participants and consumers.

Looking to the future, ING will remain committed to the international efforts driving innovation and collaboration with industry partners. We have already seen success this year in the commodities trade finance industry, where we worked with Société Générale to develop a blockchain-based prototype platform to execute a real-time oil trade. The experiment was a success, reducing the overall trade time from approximately three hours to 25 minutes. Moving forward, not only do we see this technology transforming a largely manual process into a far quicker and more efficient procedure, but we also see scalability and the capacity for adaption across other sectors.

As explained in my paper, blockchain technology is not the solution for everything, but simply is a technology that enables. The question is where we will find the greatest value. It has the capacity to have an impact across many different layers of the financial services sector and as long as we continue to work together as an industry, I am confident that blockchain will be able to live up to the buzz.

♣♣♣

Notes:

- This blog post is based on the author’s paper Blockchain is not the thing. It’s the thing that enables the thing, Journal of Digital Banking, Volume 1 Number 2 (Autumn/Fall 2016)

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Internet, by geralt, under a CC0 licence

- Before commenting, please read our Comment Policy.

Mark Buitenhek, Global Head of Transaction Services, ING Bank

Mark Buitenhek, Global Head of Transaction Services, ING Bank