When you meet someone at a cocktail party who learns you are an economist, the inevitable question follows, “What’s the stock market going to do?” That’s an excellent question. If, on the day I was born, my parents had invested $100 for me in Altria, the top-performing stock since then, I would be a millionaire.

Of course, most of us economists do not spend our time thinking about the stock market.

The press has its own view of what we do, not always positive, whether criticising our inability to predict the future (Harford 2014), our lack of engagement with the real world (The Guardian 2017), or our preference for mathematics over people (Smith 2015). How do we, as economists, combat these negative stereotypes? Perhaps by explaining better the broader set of issues economists think about and how we think about them. I recently attempted this in a chapter (Snyder 2017) published in What Are the Arts and Sciences? A Guide for the Curious.

In a nutshell

One short answer is that economics is the social science focusing on people’s material well-being, the ‘business side’ of life. How do people earn a living? What do they buy with the money they earn? What spurs the overall economy to grow?

While a starting point, the domain of economics has continued to expand, blurring any distinctions between it and other social sciences. For example, crime was once exclusively a matter for sociologists and corruption for political scientists. But economists realised that these social problems might respond to economic incentives, and left untreated could destroy a productive economy. In this way, the issues have become part of mainstream economics.

Art auctions

One might think nothing could be further from the ‘business side’ of life than art, but even this has become the subject of economists’ study. In 2015, Picasso’s painting Women of Algiers broke the record for the highest price paid at an art auction. While economists may have few insights about the quality of the brushstrokes, they have deeper insights about the outcome of the auction, held at the international auction house, Christie’s.

Bidding was intense. The opening price was $100 million. Bidders drove the price up to $180 million, its sale price, in ten minutes. Though they were allowed to bid in $1 million increments, at several points in the auction bidders jumped over the previous offer by $10 million.

To many people, this jump-bidding strategy is puzzling. It wastes the chance of winning the painting for less if the other bidders would have dropped out before the price rose the full $10 million. Some economists suggest that jump bidding may be a strategic attempt to scare off other bidders. They reason that rivals may consider it foolhardy to stay in an auction with someone who values the item so highly that he or she would be willing to waste money to prove it (Avery 1998).

Jump bidding is not the only interesting feature of this auction. Why did Christie’s pick $100 million for the opening price instead of $80 million or $120 million? Why not have each bidder submit a single, secret bid instead of ascending series of open outcries?

Theoretical principles

Although economists study topics ranging from jobs to corruption to art, some core concepts underlie their thinking. Perhaps the most important is scarcity. Devoting resources to one project—say, preventing diabetes—means some other worthy project—curing cancer—goes unserved. So, in determining whether a choice should be undertaken, one of the functions of economics is to argue that its benefits should not be considered in isolation but weighed against its costs. Costs put a dollar value on what has to be given up when one choice is made over another.

How is value determined? Scholars puzzled over this for a long time. Why are diamonds, mere decorations, so prized, while water, essential for human life, flows freely from public fountains? In the Middle Ages, philosophers advanced the just-price theory. This argues that value is an inherent property of an object. On this view, diamonds are expensive because of their inherent quality, and water is not. But this theory is unsatisfactory. It does not explain where this inherent value comes from, nor is it consistent with price variation across cultures and time. Karl Marx contributed the labour theory of value, arguing that the value of an object is the effort workers put into its production. The labour theory has its own drawbacks, leading to the awkward conclusion that an hour-long tooth extraction would be sixty times more valuable than one that had taken a minute.

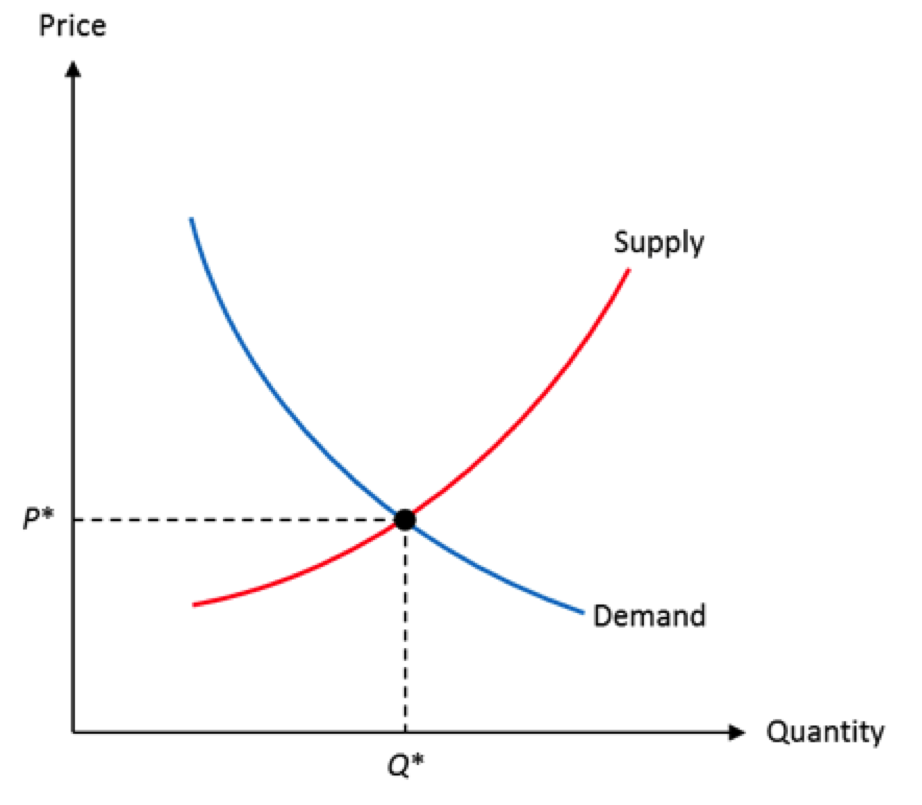

Today, economists generally believe that value is neither inherent, nor determined by a single factor, but is the result of the interaction of several impersonal market forces. We can explain the water-diamond paradox simply by drawing curves of supply and demand, as depicted in Figure 1. Seller behaviour is represented by the red supply curve. Its upward slope indicates that at higher prices, more is supplied as existing suppliers expand their operations and new suppliers are drawn into the market. Buyer behaviour is represented by the blue demand curve. Its downward slope indicates buyers are willing to purchase more at lower prices.

Figure 1. Market supply and demand

An equilibrium is reached where supply and demand intersect. At other points, either supply exceeds demand, leading price to fall as sellers accepted lower prices to offload their excess inventory, or demand exceeds supply, leading price to rise as buyers would still line up to buy at higher prices rather than do without the good. Equilibrium price P* determines the object’s value.

Using this model, one can easily resolve the water-diamond paradox. Water is in abundant supply, intersecting demand at a price near zero. At this price water is used not just to prevent people from dying of thirst, but also to water lawns. Diamonds, by contrast, are mined in only a few places in the world. The restricted supply intersects demand at such a high price that diamonds are reserved for extraordinarily high-value uses, such as marriage commitments.

Causality in empirical economics

From its earliest days, economics has been theoretical. It originated as a branch of philosophy. More recently, economic research has shifted in an empirical direction, spurred by the availability of rich data and powerful computers.

One of the great advances of modern empirical economic research is causal identification—uncovering true causal relationships rather than overinterpreting apparent correlations as causation. Uncovering causal relationships is difficult in economics. Opportunities to run experiments are limited by the expense and ethics involved in controlled interventions in markets (although these opportunities are growing, owing to an explosion of interest in laboratory and field experiments).

Economists have to devise clever ways to establish causation in nonexperimental data. Pick one of your favourites. A microeconomist might choose Dale and Krueger’s (2002) study of whether a more prestigious college causes higher earnings after graduation, explaining the problem that positive correlation may be wholly due to the higher ability of students admitted to better colleges. A macroeconomist might pick Romer’s (1992) study of whether fiscal or monetary policy deserved more credit for the US recovery from the Great Depression. The problem: a bad economy can feed back to make beneficial policies look damaging.

Back to the stock market

Having patiently listened to your description of what you do, your audience may still expect an answer to the million-dollar question, “What’s the stock market going to do?” Recall the stock that could have made me a millionaire by now, Altria, the top-performer over the last several decades according to Siegel (2005). Are you curious what Altria makes? A good guess might be something high-tech, perhaps computers or pharmaceuticals.

Altria makes cigarettes. Until a recent spinoff, Altria was the parent company of Phillip Morris, manufacturer of Marlboro and other cigarette brands. With smoking on the decline in rich countries due to high taxes and restrictions, it is hard to believe cigarette manufacturing would be a good investment.

The surprising performance of cigarettes provides a useful economic insight into stock prices. It is tempting for average investors to think they can beat the market, but study after study shows this is generally not true. They are better off diversifying across many stocks and holding these stocks over the long term.

♣♣♣

Notes:

- This blog post appeared originally at Vox. It discusses some of the author’s ideas in What is Economics?, his chapter in the book What Are the Arts and Sciences?, edited by Dan Rockmore, Dartmouth College Press, July 2017.

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Symbol, by geralt, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Christopher Snyder is the Joel Z. and Susan Hyatt Professor in the Department of Economics at Dartmouth College, specialising in the fields of industrial organisation, microeconomic theory, and law and economics, a coauthor on several graduate and undergraduate textbooks. He is a Research Associate in the National Bureau of Economic Research and Treasurer of the Industrial Organization Society. He received his Ph.D. in Economics from the Massachusetts Institute of Technology in 1994.

Christopher Snyder is the Joel Z. and Susan Hyatt Professor in the Department of Economics at Dartmouth College, specialising in the fields of industrial organisation, microeconomic theory, and law and economics, a coauthor on several graduate and undergraduate textbooks. He is a Research Associate in the National Bureau of Economic Research and Treasurer of the Industrial Organization Society. He received his Ph.D. in Economics from the Massachusetts Institute of Technology in 1994.