It has been an eventful week with the government introducing the “UK Internal Market Bill” and the EU reacting by threatening legal action against the UK unless it rewrites the bill to avoid a serious violation of the withdrawal agreement and international law. This is something that could have implications for the Brexit negotiations. On the pandemic front, with UK cases increasing, the government has announced a change in the rules for social gatherings. From Monday 14 September, households will not be able to meet in groups of more than six.

With Brexit negotiations looking gloomy, the pandemic increasing in a worrisome way and the job-retention scheme (furloughs) close to its end by the end of October, it is useful to take a look at the monthly recovery of sectors related to the food and drink industry using the latest figures.

Exploring the situation within the agri-food industry

The Office for National Statistics (ONS) announced that in July 2020 gross domestic product (GDP) grew 6.6% relative to June (the agricultural sector had a modest 1.1% growth in the same period). However, it is important to put this in context so as not to be complacent. GDP growth in July is 12% lower than the average for January-February 2020 as well as from July 2019 (agriculture only decreased by 2% with respect to January-February 2020 and from July 2019).

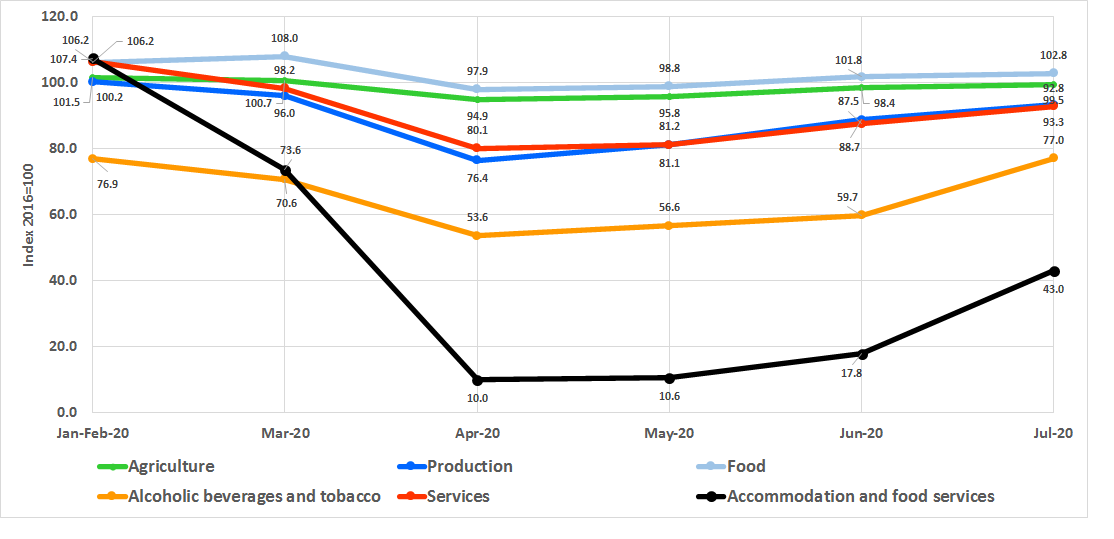

Figure 1 shows the evolution of selected sectors since the pre-COVID-19 months of January and February. Whilst all the portrayed sectors seem to be on the road to recovery, the chart also shows the important diversity among them, with the service sectors returning at a slower pace than the production sectors due to the difficulty of reactivating demand and regaining confidence.

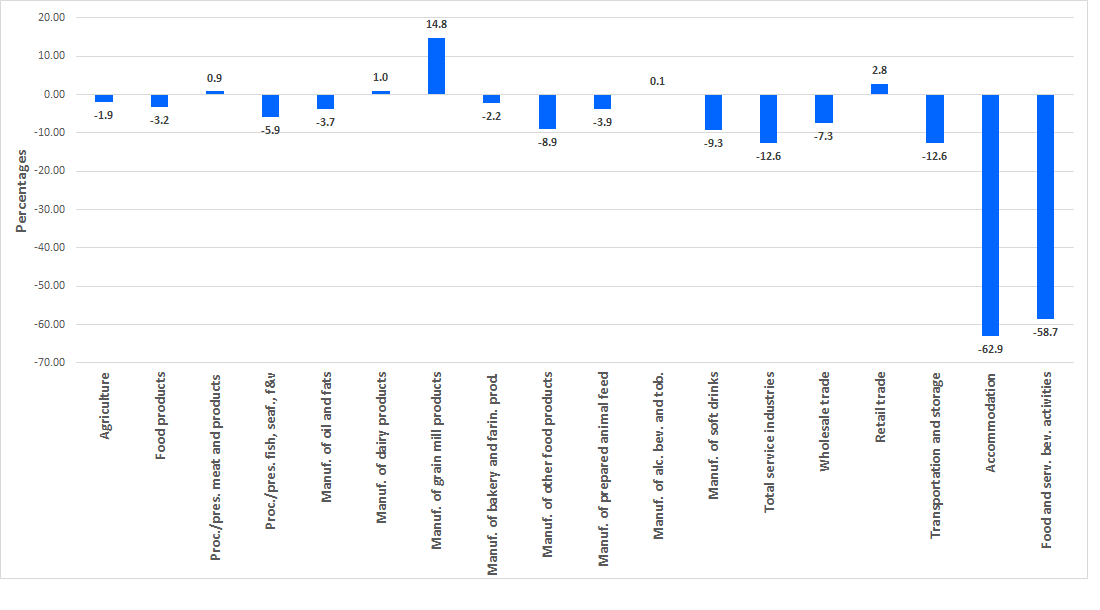

Figure 2 offers a more detailed picture of the recovery and also highlights its diversity. Not surprisingly, sectors such as ‘meat products’, ‘dairy’ and ‘grain milling’ grew above the pre-COVID-19 levels, helped by an unprecedented growth in the demand for cooking and baking, despite the contraction in food services.

All the other food sectors are still below the pre-COVID levels. Moreover, figures show that the recovery has not been steady for all sectors. For instance, ‘manufacturing of vegetables and animal oil and fats’ started to recover in April, but decreased by 6.3% in July; the ‘manufacture of prepared animal feed’ decreased 1.2% in July.

The service sectors, as expected given the massive contraction in demand, are still at significantly lower levels than before the pandemic with ‘accommodation’ dropping 63% and ‘food services’ 59%.

Figure 1. COVID-19 timeline: selected production indices, January – July 2020

Source: ONS. Seasonally adjusted indices.

Figure 2. Percentage change in July 2020 relative to pre-COVID levels (January-February 2020)

Source: ONS.

The current production figures are for July and therefore there are still three months to the end of the furlough scheme. As an illustrative exercise, considering the observed growth rates from the minimum levels achieved in April (in most cases) during the lockdown, the food sector could return to pre-COVID levels by September and the services sector by October. These, of course, are very optimistic scenarios since they are calculated based on the very low levels achieved during the lockdown. Nevertheless, this indicates that the pace of recovery is very important to assess the impact that eliminating the furlough scheme may have on the industry.

The furlough scheme by sector

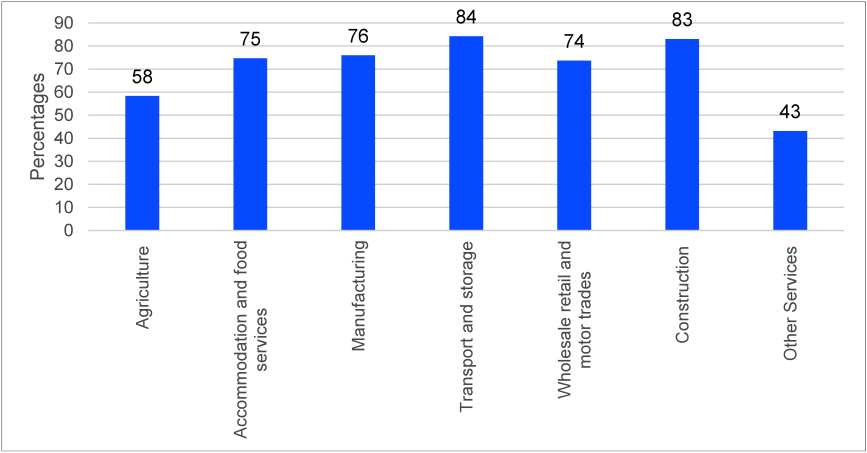

The furlough scheme was launched on 20 April 2020 to help companies maintain their workforce if workers’ performance was affected by COVID-19. In June and July, government contribution covered 80% of wages up to a cap of £2,500, plus employer National Insurance Contributions (ER NICS) and pension contributions for the hours the employees were on furlough. As shown in figure 3, the percentage of furloughed employees differed by sector according to the latest data (July).

Figure 3. Percentage of furloughed employees by sector (by 31 July 2020)

Source: HMRC.

In August, the government asked employers to pay ER NICS contributions. Up to 16 August, a total of 9.6 million employees were furloughed in the UK, accounting for a total value of claims of £35.4 billion.

In September, the government contribution was reduced to 70% of wages with a cap of £2,187.5. Moreover, employers must pay ER NICs and pension contributions and top up employees’ wages to ensure they receive 80% of their salaries with a cap of £2,500. It is expected that the gradual reduction of the furlough scheme (to be reduced to 60% of wages covered by the government in October), the slow recovery of production, and the overall uncertainty brought by the deadly combined effects of COVID-19 and Brexit may increase the number of redundancies in the workforce.

In addition to the government support for companies, the government approved the self-employment income support scheme. Self-employment represents 15.3% of employment in the UK. This scheme consists of two grants calculated considering the average trading profit over three tax years. The first grant was closed 13 July. It was based on 80% of the trading profits and capped at £7,500 in total. The second grant will close on 19 October, amounting to three months’ worth of profits, at 70% of the average monthly trading profits and capped at £6,570 in total. Figure 4 shows a less different picture between sectors than for the case of companies, the agriculture sector being the less affected.

Figure 4 shows that the percentage of the self-employed claiming government support had less variation by sector than the percentage of furloughed employees (figure 3), agriculture being the less affected sector.

Figure 4. Percentage of claims for self-employment income support by sector (by 31 July 2020)

Source: HMRC.

It is not difficult to anticipate that when the furlough and self-employment support schemes reach their end, we should expect a sharp rise in the unemployment rate, particularly in sectors related to services and construction.

Still in muddled waters

The pandemic is still with us and although consumer demand is recovering it is still far from pre-COVID levels. A spike in the levels of infection will inevitably slow the recovery.

It is crucial to maintain a quick pace of recovery to reduce the effects of ending the support schemes. However, given the diversity of the situation, probably a targeted scheme for those sectors most in peril is the way to go.

Before COVID-19, the situation of the economy for a Brexit negotiation was different than what it is now. Different sectors have been substantively affected and are less fit to recover from new shocks. The prospects for reaching a smooth trade agreement with the EU are unclear despite the end of the transition period being so close. This only increases the climate of uncertainty that surrounds the UK economy.

The EU has been the UK’s main trading partner and UK firms are highly integrated through bidirectional trade of final, in-process and raw materials. Severing this relationship in an abrupt manner should not be taken lightly.

♣♣♣

Notes:

- This blog post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by stephriddell, under a Pixabay licence

- When you leave a comment, you’re agreeing to our Comment Policy

Cesar Revoredo-Giha is a senior economist and food marketing research team leader, and a reader in food supply chain economics at Scotland’s Rural College (SRUC).

Cesar Revoredo-Giha is a senior economist and food marketing research team leader, and a reader in food supply chain economics at Scotland’s Rural College (SRUC).

Montserrat Costa-Font is the programme director for the MSc in food security at the University of Edinburgh, and a food supply chain economist at Scotland’s Rural College (SRUC).

Montserrat Costa-Font is the programme director for the MSc in food security at the University of Edinburgh, and a food supply chain economist at Scotland’s Rural College (SRUC).

Buen articulo con una gran dosis de actualidad. Es muy oportuno que, además de refenciar los importantes aspectos económicos globales de UK afectados, se profundice en los efectos directos y en las consecuencias en el ámbito alimentario que pueden provocar ciertas discrepancias en la aplicación del Brexit.