The Italian government has outlined a number of policies aimed at reforming Italy’s labour market, with the proposals receiving final approval in the Italian Senate on 3 December. Andrea Lorenzo Capussela and Vito Intini assess whether the reforms, which have proved controversial, will actually have the desired effect in generating economic growth and employment. They write that while increasing the flexibility of the Italian labour market may be desirable, the rigidity of the labour market is not the biggest obstacle to growth in the country. They argue instead that the quality of Italy’s political institutions and governance standards should be the key focus of reform efforts.

The Italian government has outlined a number of policies aimed at reforming Italy’s labour market, with the proposals receiving final approval in the Italian Senate on 3 December. Andrea Lorenzo Capussela and Vito Intini assess whether the reforms, which have proved controversial, will actually have the desired effect in generating economic growth and employment. They write that while increasing the flexibility of the Italian labour market may be desirable, the rigidity of the labour market is not the biggest obstacle to growth in the country. They argue instead that the quality of Italy’s political institutions and governance standards should be the key focus of reform efforts.

On 24 September, Italy’s Prime Minister, Matteo Renzi, outlined his government’s priorities to the Council on Foreign Relations in New York. The following passages are taken from the transcript of the speech:

“So what is the goal of our government?… I think the first thing is to change the labour market in Italy… First of all, labour market… Second, [improving] civil justice… Third, a big cut of politicians… Four, a fight against corruption.” – Matteo Renzi, 24 September 2014

Labour market reform was not part of the programme on which this government – which relies on a left-right political alliance dominated by Italy’s main progressive party, the Partito Democratico (PD) – received a vote of confidence in the Italian Parliament in March. Nevertheless, the government’s reform proposals, unveiled shortly before Renzi’s speech in New York, were approved by one chamber of parliament in October, and were thereafter presented to Italy’s European partners as the centrepiece – next to a reform of the bicameral legislative system and of local administration (the ‘big cut of politicians’) – of the government’s programme of structural reforms.

Renzi’s labour market reforms: the ‘flexicurity’ model

The reference model is what is generally known as ‘flexicurity’. In essence, the reform has four distinct goals. First, it seeks to weaken employment protection, so as to reduce unemployment and raise the employment rate. Second, it has the goal of reducing the marked ‘dualism’ of the labour market, now divided between employees on standard indefinite-term contracts and employees on any of over 40 other different categories of labour contracts, or working under informal arrangements. Third, it aims to strengthen social security through a wide, albeit not generalised, unemployment benefits programme (up to €1,000 euros per month for up to two years). Finally, the reform is intended to improve training and job-finding services.

Few would doubt that Italy’s labour market is relatively inefficient, or that regulatory rigidities are part of the explanation for the high unemployment rate – the seasonally adjusted rate observed in October is 13.2 per cent, and 43.3 per cent among the youth: the corresponding Eurozone averages are about 1.7 and 20 percentage points lower, respectively. Few would also doubt that this is part of the reason for the equally low labour market participation rate, which stood at 55.6 per cent in the second quarter of 2014, and 46.5 per cent among women: respectively about 8 and 12 points below the corresponding Eurozone averages.

Moreover, improving social security, training and job-finding services, curbing informality, and remedying the unfair and inefficient dualism of the labour market – EUROPP just published two articles (here and here) on the stance of the trade unions in this respect – are all widely shared objectives. The most distinctive trait of the government’s plans, however, is the most controversial one: reducing employment protection.

Since 1970, wrongfully dismissed standard-contract employees are entitled to be reinstated in their workplace if they work for a firm employing more than 15 employees. In 2012 this rule was partially relaxed by the technocratic cabinet led by Mario Monti; the proposal now is effectively to abolish it: in most cases, the only remedy would be monetary compensation.

Thus far, public debate has proceeded along rails that were laid down over a decade ago, when a centre-right government attempted a similar reform. Critics – the unions and one set of progressives – predominantly invoke arguments of fairness and social justice, whereas supporters – most conservatives and another set of progressives – chiefly invoke the equally classic microeconomic argument that if firing is easier, firms shall be more inclined to hire.

However the macroeconomic rationale of this proposal, and of the whole reform, has received little attention, far less than it deserves. For this, we would argue, is the central question: whether the proposed reforms have the capacity to actually stimulate employment and economic growth.

Will the reforms actually generate growth and employment?

Plainly, the question is answered neither by the fairness and social-justice objections – which we shall not address, important though they are (including for their repercussions on social cohesion) – nor by the government’s main argument. Although relaxing employment protection can be assumed to make hiring easier, it does not necessarily follow that this reform will translate into faster growth or greater employment.

The question we have posed lends itself to several complementary lines of reasoning. For reasons of space we shall neglect both the demand-side analysis and one supply-side question, namely whether there may be a trade-off between labour market flexibility and employee productivity. We shall simply assume that significantly reducing employment protection could, all things being equal, achieve a non-negligible reduction of unit labour costs; and we shall not question whether the direction towards which this reform nudges the development of Italy’s economy – focusing less on productivity growth than on wage containment or compression – is desirable or even sustainable in the long term. Although these questions impinge on the core rationale of the government’s proposals, we shall assume both away.

We follow two lines of argument, approaching them in a medium-term perspective. First, we ask whether other constraints than the current employment protection rules exercise significant influence over firms’ employment choices. Second, we assess whether the proposed ‘flexicurity-like’ model is compatible with the existing institutional framework, or shall entail non-negligible adjustment costs.

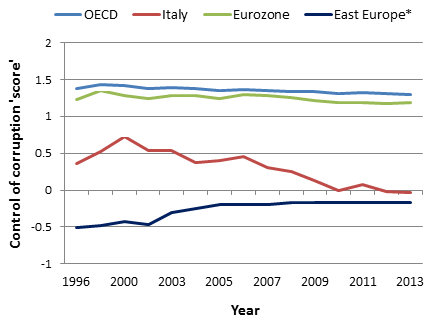

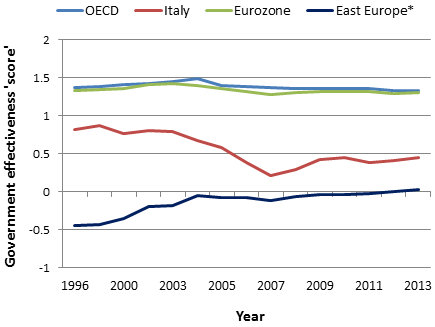

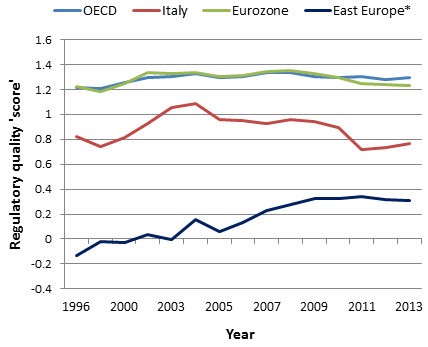

A notable peculiarity of the Italian economy is the weakness of its institutions, in fact. This pronounced, idiosyncratic trait emerges clearly from Figures 1-5. They show Italy’s position relative to both its peers and other economies according to the World Bank Institute’sWorldwide Governance Indicators, which synthesise all available indictors of the quality of institutions – elaborated by specialised sources ranging from Transparency International, for instance, to the World Economic Forum – into six ‘meta-indicators’ (we have excluded those which measures political stability and violence, which seems less relevant).

Figure 1: Comparison between Italy and averages for the OECD, the Eurozone and Eastern Europe on five of the World Bank’s ‘Worldwide Governance Indicators’ (1996-2013)

[fusion_tabs layout=”vertical” backgroundcolor=”” inactivecolor=””]

[fusion_tab title=”Rule of Law”]

[/fusion_tab]

[fusion_tab title=”Control of Corruption”]

[/fusion_tab]

[fusion_tab title=”Government Effectiveness”]

[/fusion_tab]

[fusion_tab title=”Regulatory Quality”]

[/fusion_tab]

[fusion_tab title=”Voice and Accountability”]

[/fusion_tab]

[/fusion_tabs]

Note: The charts show an index score for each of the five indicators (the higher the score, the more positive the assessment is). The Eastern Europe* group contains Albania, Bosnia, Bulgaria, Hungary, Macedonia, Montenegro, Romania, Serbia and Turkey. Source: World Bank

The gap between Italy and its OECD and Eurozone peers is both significant and widening. Equally striking is its gradual convergence with the states of Eastern Europe: Italy seems to be the only large industrialised economy that is regressing to governance standards that are generally observed among upper middle-income countries. Indeed, Transparency International’s latest Corruption Perceptions Index – published just last week, and therefore not included in the indicator shown in the chart above – places Italy on par with Bulgaria and Romania (and below Malaysia, Rwanda and Ghana, for example). These negative trends are corroborated by opinion surveys, such as those conducted by Eurobarometer on corruption and the social climate, which rank Italy at the bottom of most indicators (including, ominously, those dealing with trust in public institutions).

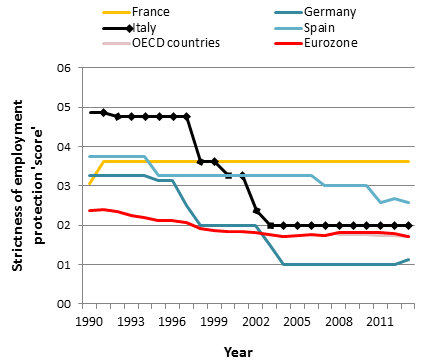

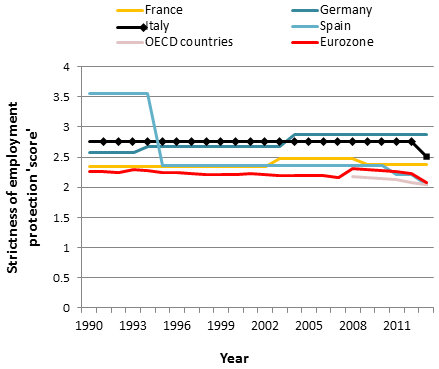

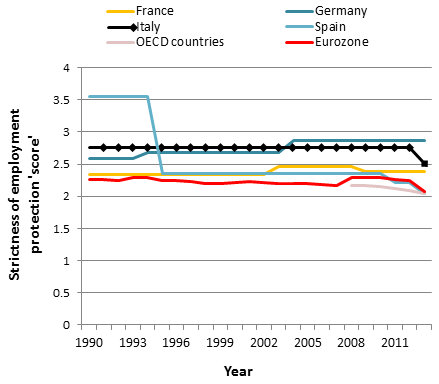

These observations can now usefully be contrasted with the country’s relative position according to indicators of labour market rigidity, shown in Figure 2 below. The picture here is markedly different: Italy is significantly closer to its peers, and the gap seems to be narrowing.

Figure 2: Strictness of employment protection in Italy and selected countries (1990-2012)

[fusion_tabs layout=”vertical” backgroundcolor=”” inactivecolor=””]

[fusion_tab title=”Temporary Contracts”]

[/fusion_tab]

[fusion_tab title=”Regular Contracts – Individual Dismissals”]

[/fusion_tab]

[fusion_tab title=”Regular Contracts – Individual and Collective Dismissals”]

[/fusion_tab]

[/fusion_tabs]

Note: The charts indicate scores for the strictness of employment protection (based on OECD calculations), with a higher score indicating stricter protection. Source: OECD

It is therefore legitimate to question whether the most binding constraint to growth and employment is labour market rigidities, as the government’s declared (and observable) economic policy programme would seem to imply. The Table below instead hints at a high correlation between growth – measured by its total factor productivity (TFP) component – and Italy’s institutional inefficiencies (as reflected by the ‘Government Effectiveness’, ‘Control of Corruption’ and ‘Rule of Law’ indicators used in the first three charts in Figure 1).

Table: Correlation between economic growth in Italy and measures of government effectiveness, control of corruption and rule of law

Note: The table shows correlation values between total factor productivity (an element of economic growth) in Italy and measures of government effectiveness, control of corruption and rule of law. The closer the figure is to 1 the greater the correlation: for instance an increase in government effectiveness is correlated strongly with an increase in total factor productivity (growth). All of the figures shown are statistically significant at 1%.

A similar pattern emerges from the correlation shown in Figure 3, which uses the competitiveness and quality of institutions indexes elaborated by the World Economic Forum.

Figure 3: Correlation between economic competitiveness and quality of institutions in selected European countries

Note: The figure plots countries on a chart based on a score of their overall competitiveness (vertical axis) and the quality of their institutions (horizontal axis) using measures provided by the World Economic Forum. As can be seen, those states with higher quality institutions also appear more competitive overall.

Much of the explanation for Italy’s relatively weak TFP and growth performance thus presumably lies in factors such as those addressed by the government’s other priorities: public administration and civil justice reform, and the fight against corruption. Indeed, the governor of the Italian central bank has recently – and persuasively – argued that fighting illegality and criminality is a ‘precondition for economic growth’.

None of this implies – under the assumptions we have made – that making the labour market more flexible is inadvisable, because this reform might conceivably produce its (assumed) beneficial effects over a shorter time frame than attempts to remedy such institutional inefficiencies, which are inherently long-term concerns. Yet our second line of argument becomes relevant at this point: namely, what effects, and what adjustment costs, would the transposition of the ‘flexicurity’ model into the Italian regulatory framework have?

Without going into the question of the possible unintended effects of institutional transplants, it can nonetheless be noted that Italian firms have long relied on price competitiveness (including currency devaluation) rather than on TFP growth, and often seem to have achieved cost efficiency precisely thanks to the dualism of the labour market: so although remedying it is, in principle, a welcome move, it might entail significant adjustment costs for those businesses that contain employment costs through the extensive use of atypical employment contracts.

So what macroeconomic effects is the proposed reform likely to have? If, as our figures above strongly suggest, labour market rigidities are not the most binding constraint to firm growth and private investment, reducing employment protection is unlikely per se to appreciably stimulate employment. This is all the more so if the adjustment costs entailed by the proposed reform more or less off-set its beneficial effects.

The considerable political capital invested by the government in pushing this policy is therefore unlikely to produce any appreciable acceleration in growth, which the country urgently needs instead (GDP has fallen for thirteen consecutive quarters, and the risk of a debt-deflation spiral is not far-fetched). Paradoxically, given Italy’s very unfavourable current macroeconomic conditions, if the new rules shall apply also to existing workers then the most likely short-term effect might be an increase in redundancies, which in turn may further depress consumption and therefore also growth.

Some commentators have argued that this reform also had an eminently political objective, as the confrontation it opened could both subdue the left-wing minority of the ruling party and weaken the trade unions’ ability to constrain the executive’s choices. Yet the government has already won the political battle: parliament has just passed the bill before it, which authorises the government to transform its proposals into detailed legislation. It is now up to the government to decide exactly how far the reform should go, within the limits set by the parliament’s delegation.

Labour market reform is now effectively a pledge, however, which the government has offered to its European partners. Yet not even this seems a sufficient reason to proceed without further reflection. As Italy’s sovereign debt arguably remains the single biggest threat to the monetary union, it would seem counterproductive for its partners to demand the implementation of this reform – which is likely to generate further social tensions – without reasonable assurances that it shall have positive macroeconomic effects.

A pause for reflection could stimulate more careful scrutiny of the issues we have assumed away, which do not seem settled, and would especially allow the government to devote more energy and political capital to its other priorities, which target some of the acute institutional problems highlighted by Figure 1. The government’s initial proposals on the repression of corruption, tax evasion and money laundering, for example, have partly been watered down in negotiations with the coalition parties, and now proceed rather slowly.

A more determined political effort to overcome these – largely indefensible – perplexities would seem advisable: not just because these reforms hold considerable promise for Italy’s economy, long-term though they are, but also because they could rely on broad support and strengthen much-needed social cohesion.

Please read our comments policy before commenting.

Note: This article gives the views of the authors, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics. Featured image credit: Città Di Modena (CC-BY-SA-3.0)

Shortened URL for this post: http://bit.ly/1InhT20

_________________________________

Andrea Lorenzo Capussela

Andrea Lorenzo Capussela has a PhD in competition policy. He served as the head of the economics unit of Kosovo’s international supervisor, the International Civilian Office, in 2008–11, and as the adviser to Moldova’s economy minister and deputy prime minister, on behalf of the EU. He is the author of State-building in Kosovo: Democracy, EU Interests and US Influence in the Balkans (I.B. Tauris: London, forthcoming) and is currently working on another book (with Vito Intini), while also conducting some voluntary work on the development of a district in Calabria, Italy’s most depressed region.

Vito Intini

Vito Intini has conducted post-graduate studies in several economic fields and has worked for different research and development institutions, in Italy and abroad.

1 Comments