In late 2017, we published a blog entry summarising some of the findings of the report Challenges for our home ownership safety net: UK and international perspectives, published by UK Finance and authored by LSE London’s Christine Whitehead and her colleagues, Peter Williams and Steve Wilcox. In this blog post, we report on the findings of the article Reducing the risks of mortgage default and possession in the UK; an international perspective, published in the latest (Summer 2018) issue of Housing Finance International, The Quarterly Journal of the International Union for Housing Finance which reflects further on these issues.

Understanding the sources of risk is important in clarifying the nature and value of different approaches to ‘safety nets’. The authors highlight three types of risk, leading to three distinct potential approaches to risk management:

- first, that relating to changes in individual circumstances—unemployment, sickness, accidents etc – which make it difficult or impossible to pay the mortgage and can be addressed by some form of insurance;

- second, market wide risks which occur when economic circumstances change, and large numbers of households find themselves in default at the same time requiring the government or industry to put in place measures to stabilise the mortgage market and enable adjustment; and

- third, structural changes at a macro-prudential scale which change to scale of potential risks and require longer term regulatory policies to stabilise mortgage and finance markets.

Issues around safety nets in the first two categories came to the fore in the UK at the time of the economic crisis in the early 1990s, when some 2 million households found themselves in negative equity and many became unemployed or saw significantly falling incomes. The Government responded by increasing Income Support for Mortgage Interest (ISMI) to help this group but it also enabled payments to be made directly to lenders in exchange for their developing policies which helped households keep their homes. From these experiments, a partnership emerged between government and lenders which steered policy towards linking mortgage payment protection insurance with ISMI (now called SMI). At the time of the 2008 economic downturn the government increased the value of the mortgage covered (from £100k to £200k) to limit the projected rise in home possessions but also started to put on additional constraints. To this day, SMI remains the most significant government intervention to help individual homeowners having difficulties with their mortgage. But at the same time government both put in place systems to ensure the industry had to take greater responsibility for market wide problems and to incentivise more conservative lending policies.

In April 2018, the government made significant changes to SMI shifting it from a grant to a loan (with interest) that comes with a charge on the recipient’s mortgage. While the Department of Work and Pension has intensified efforts to disseminate information about these changes, the latest figures show that many claimants have lost their support which will inevitably lead to accumulating arrears and likely lender action. Along with other changes to the waiting period before SMI kicks in (from 13 to 39 weeks), these changes make households in difficulty more vulnerable.

This erosion has been made possible in part because arrears and possessions are now at historic lows and continue to decline. The current outlook in the UK also seems relatively benign and may well remain so unless interest rates rise significantly and unemployment grows. One important issue here is that tighter regulations on borrowing to address the third, macro-prudential level of risk have made for a more homogenous and more conservative cohort of borrowers. In this context, while the Bank of England does not use the ‘safety net’ terminology, it does recognise various measures strengthening macro prudential policies as building a safety net into the system.

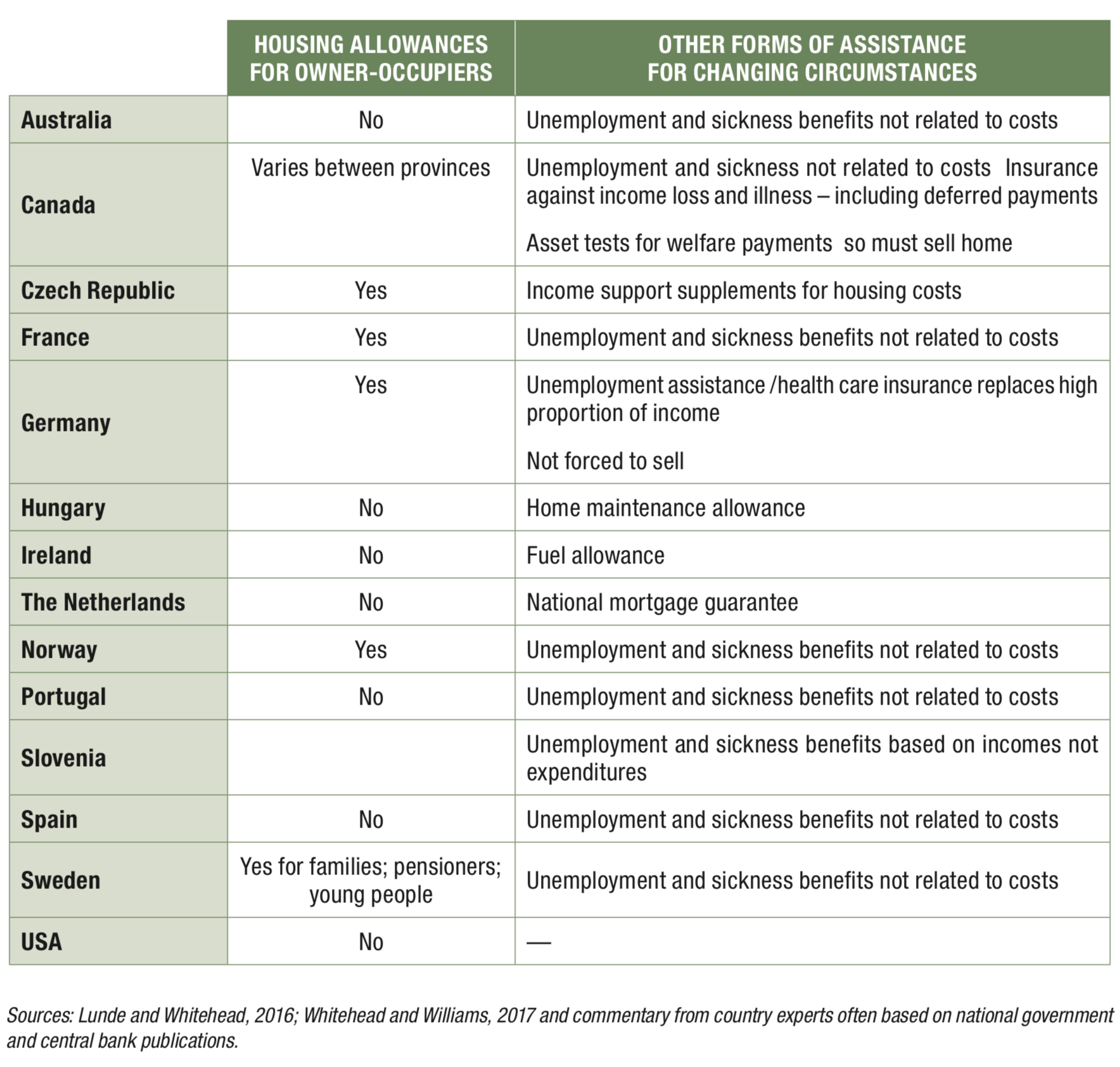

In comparing the UK situation with other countries it is clear that the UK is atypical in having such a structured safety net for individual home owners (see Table 1 for specific comparisons). In part this is because in many European countries social security is much more generous and the UK is more likely to be less generous and less likely to be related to past levels of income – so the problem can be subsumed into the general welfare system.

Where there are far fewer differences is in respect to addressing to market wide and especially macro-prudential risks, where there is considerable international agreement around the need to tighten lending standards – with consequential reductions in access to owner-occupation. In particular, there is also a fairly consistent strand running through policy which requires mortgage providers to take more responsibility and to bear more of the costs through restructuring payments and in some cases even subsidising borrowers.

So, in terms of safety nets the UK differs first by being less generous than other countries with respect to overall social security measures but more generous in providing some form of safety net for those owner-occupiers who do face difficulties. What is concerning for the future is whether the much less generous system that is now in place will need to be strengthened in the face of imminent changing economic circumstances at some point in the future.

Click here to access the article (starts on page 48) as well as other articles from this issue of Housing Finance International.