Africa’s growing debt has been increasingly framed as a consequence of China’s alleged aims of unscrupulously lending money to gain political leverage and seize African assets when states default. New research challenges this narrative and examines the continent’s debt position in relation to global institutional frameworks. Harry Verhoeven and Nicolas Lippolis argue that new Western-led initiatives, which mostly ignore Chinese concerns and incentives, leave debt issues unresolved and create zero-sum thinking about Africa’s structural indebtedness.

The inflationary fallout of the Russia-Ukraine war is the latest in a series of shocks that have battered African economies in recent years. In March 2022, the World Bank warned that “60 percent of the poorest countries were already in debt distress or at high risk of it”, with a majority of these countries in Africa and up to a dozen risking default over the next 12 months. In a region reeling from the COVID-19 pandemic and its squeezing of already limited fiscal space, the political and humanitarian consequences of mass defaults could be disastrous. The recent economic meltdown and toppling of the Rajapaksa family regime in Sri Lanka is a case in point.

In new research, published in the journal Survival: Global Politics & Strategy, we provide a critical examination of Africa’s current debt predicament and its main determinants. To challenge how much of the debate is currently framed, we rely both on rarely considered statistical material regarding Africa’s external debt position and on qualitative material drawn from elite interviews with leading actors in the international financial institutions, private sector and in African governments. In particular, we question the dominant institutional prism through which the resurgence of Africa’s debt woes is approached: the G20 Common Framework for Debt Treatments, which is now almost two years old.

The effect of “debt trap” narratives

Conceived during the highpoint of the pandemic, which led to shrinking government revenues and expanding outlays, the Common Framework promised to provide comprehensive debt relief to countries agreeing to treatment through close collaboration with the IMF. But so far, only three states have applied (Chad, Ethiopia and Zambia) and even in these cases, restructuring has been extremely slow. As a result, the IMF itself has called for a revamping of the Common Framework.

We argue that the shortcomings of the Common Framework, and those of the earlier Debt Service Suspension Initiative (DSSI), are very much a product of their entanglement with efforts to check China’s influence over the Global South. Variations of the argument that China seeks to “run up [developing countries’] debt” only to “take their assets” when faced with default have been repeatedly propagated by US officials, as part of their increasing adversarial geopolitical stance. They have also been taken up by other Western leaders, including German Chancellor Olaf Scholz. According to this “debt-trap” narrative, China seeks to intentionally take advantage of Africa’s weak economies to extend unpayable loans through its policy banks, allowing it to secure key commodities and extend its political influence.

Such discourse has real-world policy effects on how debts – and which debts – of African sovereigns are repaid. To undermine China’s lending to Africa, the US government and the World Bank categorised the China Development Bank and the Industrial and Commercial Bank of China as “official creditors”, which are then subject to repayment freezes under the DSSI, even though they have overwhelmingly lent at commercial rates. This is while exempting (mostly Western) private creditors from restrictions on recouping loans from the same African sovereigns.

In a thinly disguised effort to expose supposed Chinese “debt traps”, the Common Framework requires that applicants disclose all extant liabilities. It further proposes a debt resolution procedure mirroring that of the Western-dominated Paris Club, including by assigning the IMF as the arbiter of debt sustainability. As such, the Framework is a clear attempt to force China’s hand on the question of whether it will abide by the rules of the liberal international order. But by imposing initiatives that do not acknowledge – let alone incorporate – China’s incentives or concerns, Western powers are undermining efforts at debt resolution, while failing to address the root causes of Africa’s over-indebtedness.

Debt resolution as geopolitical point-scoring

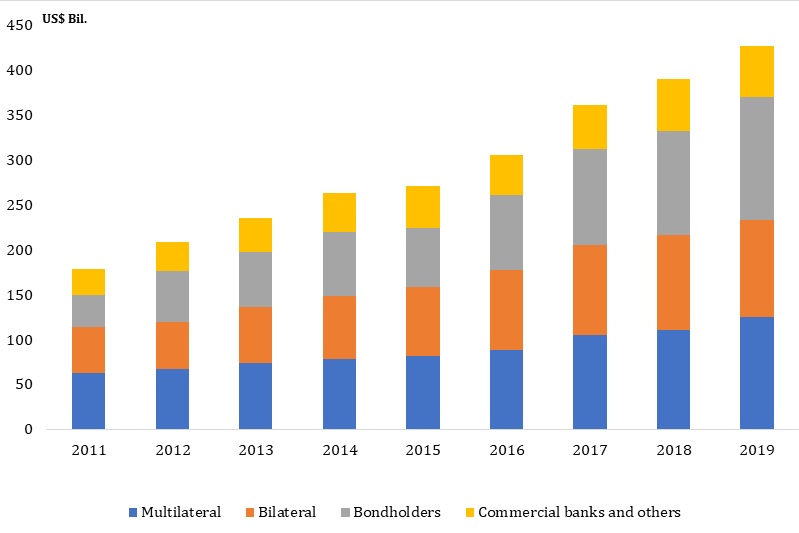

To understand these effects, it is imperative to examine how African governance strategies under “weak sovereignty” interact with imbalances in the global political economy owing to US fiscal and monetary policies. The great untold story of 21st century economics is the momentous climb in global debt, not just in Africa but elsewhere too, especially since the 2007-8 financial crisis. Low or even negative real interest rates have had two key effects. First, by stimulating Western overconsumption, China accumulated abundant foreign exchange reserves, with Beijing lending some of this excess capital to Africa. Second, and much more consequentially from a debt standpoint, African states have issued Eurobonds at an unprecedented pace (Figure 1), as African sovereigns’ desire to diversify financing created demand met by investors in a global “search for yield”.

From an African perspective, both Chinese lending and Eurobond emissions have served to address the shortfall in external funding by Western states and international finance institutions, including their woefully inadequate response to the pandemic. Recourse to the less intrusive lending modalities of Chinese policy banks and international bond markets, relative to traditional Western creditors, have also helped African states preserve their sovereignty. The result, however, has been a rapid expansion in external debt, with Eurobond finance as the chief growth factor. Private holders of debt are treated lightly by both the DSSI and the Common Framework. The latter encourages the private sector to accept comparability of treatment but leaves it free to insist on full repayment. This cannot fail to irritate China, whose perception is that of its lenders being subjected to debt standstills, while watching repayments continuing to flow to creditors based in New York, London or Frankfurt.

This inadequacy of global responses to Africa’s debt predicament speaks to the difficulty of addressing common problems in an era of heightened geopolitical competition, or so our article in Survival argues. Using mechanisms for debt resolution as a means of scoring geopolitical points against China undermines confidence in the IMF and World Bank as institutions of global governance. Leaving debt issues unresolved will over time only lead to their aggravation, potentially throwing many African countries into crisis. The zero-sum thinking current in US and Chinese approaches to global governance therefore risks blinding them to shared interests on the continent. It also prevents them from collaborating in tackling the structural issues behind Africa’s over-indebtedness, such as undiversified economies, exposure to the vagaries of international financial markets and the role of the global offshore system in enabling capital flight from the continent.

Photo: SM17 Press Briefing, Abebe Aemro Selassie, Director of the IMF’s African Department (IMF Photo by Cliff Owen). Licensed under CC BY-NC-ND 2.0.