Google driverless car at intersection, by Grendelkhan, own work, under a CC BY-SA 4.0, via Wikimedia Commons

Google driverless car at intersection, by Grendelkhan, own work, under a CC BY-SA 4.0, via Wikimedia Commons

| The authors of this blog post are members of the LSE's Student Union Economics Society and wrote this as a contribution to the LSE Growth Commission. Please see Investing in the future of the UK: LSE relaunches its Growth Commission for an overview and a video of the panel debate with Vince Cable, George Osborne, Lord Alistair Darling, Stephanie Flanders and Lord Nicholas Stern. For a list of the commission's evidence sessions, click here. |

Introduction

Following the financial crisis in 2008, central banks in the UK and other developed countries have attempted to inject extra liquidity into the market through asset purchases and low interest rates. Economic theory predicts inevitable hyperinflation, overheating, and currency crashes. Today, inflation rates are floating just above if not below zero; there remains a significant output gap, and currencies have remained more stable than expected.

One reason these economies are suffering is the lack of demand for domestic products. For example, the EU’s trade in goods deficit with China hit a record €180 billion for 2015. The US recorded a deficit of $367 billion for the same year. Developed countries are struggling to compete with the low cost manufacturing of the developing world, and will continue to do so unless there is a significant pick-up in productivity.

A standard framework in the economics literature for thinking about growth is the Solow model.

| The Solow model: Y = AF(K,L) |

|---|

| Y is output, A is a measure of productivity, K is capital, and L is labour. F (.) has the properties of a neoclassical production function: diminishing but positive marginal returns, constant returns to scale and Inada conditions |

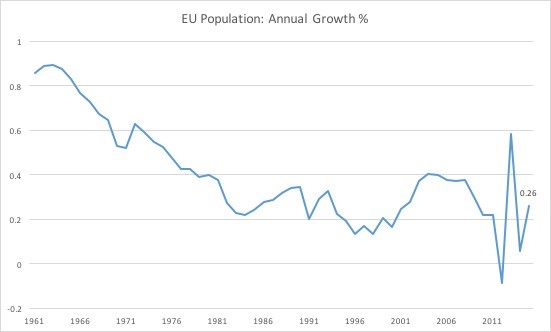

Owing to better education, higher income, and changing religious and cultural beliefs, the labour force (“L”) of developed countries in recent years has been stable, if not falling. The population of the EU grew by just 0.26 per cent, and that of the US by 0.78 per cent in 2015. This is seen as an exogenous change in the trend rate, and one we expect to be in place for the foreseeable future.

Figure 1: The EU population grew by just 0.26% in 2015

Source: World Bank

Growth Fixed Capital Formation (GFCF) [1], which accounts for net capital accumulation and is a good measure for capital (“K” in the Solow model), grew at 3.6 per cent in the EU and 3.7 per cent for the US in 2015, compared to China’s 7.2 per cent. Business investment is driven by confidence, and with current monetary policy having little to no effect on investment decisions, other policies are required to boost growth. Furthermore, with the growth of the services sector, spending on machinery and factories may never reach the heights of the 20th century. What is needed therefore, is innovation to boost “A”, the measure of productivity.

A productivity paradox?

In the era of self-driving cars and machine learning, the “productivity paradox” (the counter intuitive realisation that technological advance has led to a drop in worker productivity) is one we are yet to solve.

Robert Gordon puts forward the theory that today’s innovations are nowhere near as revolutionary as those of the previous century, and suggests a levelling off of the marginal benefits of innovation. Whilst this makes intuitive sense, we remain more optimistic about the future of productivity. Today’s global economy is stuck in a limbo between providing jobs for unskilled workers and implementing new technologies that, whilst boosting efficiency, will undoubtedly limit opportunities for the unskilled. Simply put, increases in productivity will come not only from the invention of new technologies, but also from their implementation.

Another contributor to the problem is rising inequality. Of course soaring inequality is problematic in and of itself: creating unstable social structures, a malfunctioning trickle-down effect and reduced aspirations for new innovations. But consider one of the key factors that determines labour productivity: education. As Edward Lazear and Daron Acemoglu indicate, in recent years technological change has been “skill-biased” . Mainly due to rapid technological advancement, the overall structure of advanced economies has changed, such that skilled labour enjoys significantly higher demand than unskilled labour. Under these circumstances, wage disparity has increased further, and purchasing power and the affordability of higher education for low and middle income households has not kept up with the demand for higher skills.

It may, however, be time to change the way we think about productivity in general. It is currently measured as a simple ratio of economic output to economic input. Today, a significant resources are devoted to increasing the convenience of day-to-day human life, which in economic terms adds little to no “value”. As a result, we fail to account for technological advancements where their benefits do not directly contribute to GDP.

Why Y?

The World Bank, the Office of National Statistics (ONS), and the Federal Reserve Economic Data (FRED) identify growth in terms of GDP, which can be traced to the universal consistency and acclaim in adopting GDP as a measure over the years. However, it can be argued that GDP alone is insufficient to encompass all the elements of growth within an economy. Economic growth extends beyond just goods and services to factors such as health, sustainability, technological expansion and income distribution.

There have been multiple attempts to refine economic growth measures, including a multi-dimensional approach by OECD and an Inclusive Growth Report by the World Economic Forum (WEF). While all of them suggest taking extensive complements into account when measuring GDP, none of them have stuck permanently. Only when one of these becomes a universal standard will it be possible to make the measures comparable. GDP therefore remains the only consistent measure across the world despite its limitations. It is essential to define a more accurate and standard method so as to get a clearer and a more authentic perspective on global economic growth.

So what can be done?

The issues raised above require immediate attention and support from government. To increase productivity, more sophisticated and affordable higher education systems are necessary. Such policies will also play an integral role in reducing inequality caused by “Skill-biased Technical Change”. Moreover, a boost in government spending will contribute to aggregate demand, which could possibly have a knock-on effect on business confidence.

Efforts to realize new technologies in business will also go a long way towards solving the problem. A 2014 survey of 551 small businesses conducted by IPSOS showed that 35 per cent are concerned about the costs of upgrading and maintaining new technologies. A further 38 per cent were concerned about security, accessibility, and server management, suggesting the need for increasing awareness and understanding of the abilities of such advancements. Initiatives to educate small businesses about the capabilities, (and perhaps even subsidised implementation) of new technologies will also have a significant impact on productivity. Furthermore, tax breaks linked to increased technological efficiency encourages both innovation, and the implementation of productivity enhancing infrastructure.

All these changes, however, must be captured by accurate measurements. The current focus on GDP in measuring development has served its purpose, but is still insufficient in many respects. New methods for assessing economic performance should focus more on identifying how much our standard of living changes with technological advancement, and how a change in the nature of business activity affects economic output.

[1] GFCF includes expenditure on industrial factory and equipment purchases, as well as on infrastructure such as roads, railways, etc.

♣♣♣

Notes:

- The post gives the views of the author, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy.

Ritush Dalmia is a final year undergraduate studying mathematics and economics at the LSE. He was Director of Speaker Events for the LSESU Economics Society in the academic year 2015/16, and spent summer working as a research intern at GFC Economics. His interests include the application of networks and complexity to economics, central banking and development.

Jiin Baek is a first-year BSc Government and Economics student from Seoul, South Korea. He graduated from Daewon Foreign Language High School in 2016. He is currently a member of LSESU Economics Society and is one of the editors of Rationale Magazine, a biannual magazine published by the society. His main interests are macroeconomic policy, central bankings, and international economics.

Jiin Baek is a first-year BSc Government and Economics student from Seoul, South Korea. He graduated from Daewon Foreign Language High School in 2016. He is currently a member of LSESU Economics Society and is one of the editors of Rationale Magazine, a biannual magazine published by the society. His main interests are macroeconomic policy, central bankings, and international economics.

Siddhi Doshi is in her third year of attaining a B.Sc in Economics and Math. She is a University Scholar at Northeastern University, Boston and is currently studying abroad, pursuing the General Course at LSE. Her interests lie in emerging markets, alternative finance and alleviating economic inequality.

Siddhi Doshi is in her third year of attaining a B.Sc in Economics and Math. She is a University Scholar at Northeastern University, Boston and is currently studying abroad, pursuing the General Course at LSE. Her interests lie in emerging markets, alternative finance and alleviating economic inequality.