With the global economy stuck in a low growth trap, it is crucial to understand the factors behind the weak recovery in potential output growth, and particularly the barriers to productivity growth. In our recent research, we show that this dynamic can be partly understood in terms of the increasing survival of zombie firms – i.e. those firms that would typically exit in a competitive market but are being kept alive by creditors or policy weakness.

Today, a key risk is that zombie firms may depress creative destruction, crowd-out growth opportunities for healthy firms and underpin a period of macroeconomic stagnation, just as they did in Japan in the 1990s (Caballero et al., 2008). Indeed, our research suggests that within industries over the period 2003-2013, a higher share of industry capital sunk in zombie firms is associated with lower investment and employment growth of the typical non-zombie firm and less productivity-enhancing capital reallocation. Furthermore, we link the rise of zombie firms to the decline in OECD potential output growth through two key channels: business investment and multi-factor productivity growth.

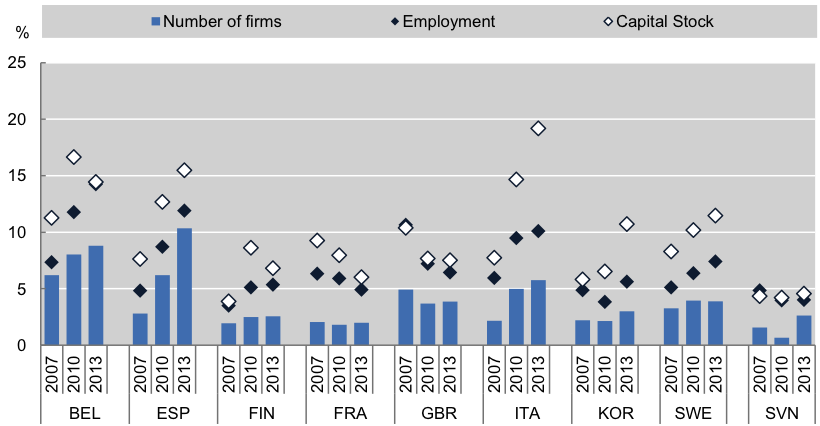

In a number of countries, the prevalence and productive resources sunk in “zombie” firms – defined as old firms that have persistent problems meeting their interest payments – has risen since the mid-2000s (Figure 1). In Italy, for example, the share of the industry capital stock sunk in zombie firms rose from 7 to 19 per cent between 2007 and 2013. This is problematic because zombie firms can congest markets and reduce industry profitability – by inflating wages relative to productivity and depressing market prices – which deters the expansion of healthier firms, especially recent entrants.

Figure 1. The share and resources sunk in zombie firms have risen

Notes: Firms aged ≥10 years and with an interest coverage ratio<1 over three consecutive years. Capital stock and employment refer to the share of capital and labour sunk in zombie firms. The sample excludes firms that are larger than 100 times the 99th percentile of the size distribution in terms of capital stock or number of employees.

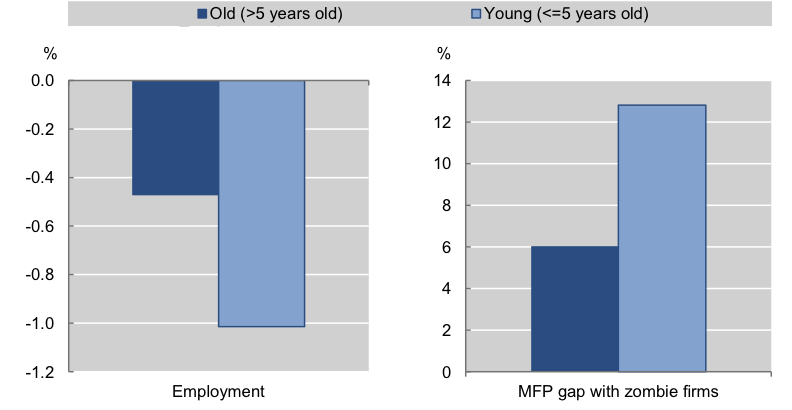

Econometric analysis shows that when more industry capital is sunk in zombie firms, the typical non-zombie firm undertakes less investment compared to a zombie firm, with young firms particularly affected (Fig 2). But the story does not end there because zombie congestion disproportionately crowds-out the growth of more productive firms, thus slowing productivity-enhancing capital reallocation and aggregate multi-factor productivity (MFP) growth.

Figure 2. Zombie congestion particularly penalises young firms

Impact of a one standard deviation increase in the zombie capital share on non-zombie firms according to their age

Note: This figure shows the ceteris paribus impact of an increase of a one standard deviation (15.6%) of the zombie share on employment and MFP of non-zombie firms, differentiating between old and young non-zombies. Zombie shares refer to the share of capital sunk in zombie firms, defined as firms aged >=10 years and with an interest coverage ratio <1 over three consecutive years. The estimates are based on nine OECD countries (BEL, ESP, FIN, FRA, GBR, ITA, KOR, SWE and SVN) over the period 2003-13. The effects on old non-zombie firms and the differential effects on young non-zombie firms are all significant at the 5% level.

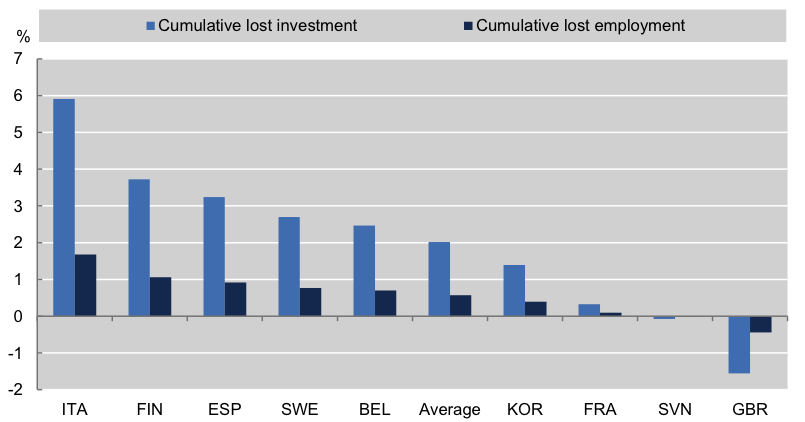

The rise of zombie congestion can be connected to the collapse in OECD potential output via two key channels: weaker business investment and MFP growth. For example, simulations show that had the zombie capital share not risen from its pre-crisis levels:

- Investment of a typical non-zombie firm in Italy could have been around 6 per cent higher in 2013. This can account for one-quarter of the actual decline in aggregate private non-residential business investment in Italy between 2008 and 2013 (Figure 3).

- Aggregate MFP could have been 0.7 to 1 per cent higher in Italy and Spain respectively, owing to more efficient capital reallocation. This is significant given that in both countries, MFP subtracted significantly from potential growth over the past decade.

Figure 3. Impact of zombie firms on the relative performance of non-zombie firms. (Cumulative investment and employment loss of a typical non-zombie firm due to a rise in the zombie share after 2007)

Note: This figure shows the cumulative lost investment and employment between 2008 and 2013 due to the presence of zombie firms. The counterfactual is to keep the zombie shares at their 2007 level for the period 2008 to 2013. The average refers to the unweighted average of the 9 countries in the sample.

In some countries, these problems are likely to be symptomatic of weak insolvency regimes (Adalet McGowan, Andrews and Millot, 2017) and a slowdown in the pace of product market reforms. But zombie firms may also be kept alive by bank forbearance and the persistence of crisis-induced SME support policy initiatives. While reforms in these areas may help revive productivity growth, it is crucial that they are flanked by well-designed active labour market policies, which have been shown to be effective at returning workers displaced by firm exit to work (Andrews and Saia, 2016).

♣♣♣

Notes:

- This blog post appeared also on the Oxford Business Law blog. The authors presented their research findings at the 67th Economic Policy Panel Meeting in Zurich on 13 April 2018. The paper is forthcoming in Economic Policy.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Photo by Jacob Surland, under a CC-BY-NC-2.0 licence OR Photo by geralt, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Müge Adalet McGowan is an economist at the country studies division of the Organisation for Economic Development and Cooperation’ economics department. She holds a PhD in economics from the University of California, Berkeley.

Müge Adalet McGowan is an economist at the country studies division of the Organisation for Economic Development and Cooperation’ economics department. She holds a PhD in economics from the University of California, Berkeley.

Dan Andrews is the deputy head of the structural policy analysis division of the Organisation for Economic Development and Cooperation’ economics department. He holds a master’s in public administration from Harvard University.

Dan Andrews is the deputy head of the structural policy analysis division of the Organisation for Economic Development and Cooperation’ economics department. He holds a master’s in public administration from Harvard University.

Valentine Millot is a junior economist in the structural policy analysis division of the Organisation for Economic Development and Cooperation’ economics department. She holds a PhD in economics from the University of Strasbourg.

Valentine Millot is a junior economist in the structural policy analysis division of the Organisation for Economic Development and Cooperation’ economics department. She holds a PhD in economics from the University of Strasbourg.

What is striking are some of the country differences – a big part of the problem in, say, Italy and Spain, but modest in France, and playing no role at all in the UK. The productivity slowdown in the UK – with the most recent revival looking as if it too might be fizzling out – must have other causes.