The UK has not yet left the European Union and the long-term economic effects of Brexit remain unknown. However, one of the trends which has attracted attention so far is a drop in real wages for UK workers, which many economists have put down to the immediate depreciation of the pound after the referendum and a subsequent rise in the cost of imports. Simon Wren-Lewis (Oxford University) explains that the picture is more complex than this, and that UK firms are anticipating a decline in the terms of trade following Brexit by not allowing nominal wages to rise to compensate for higher import prices.

The UK has not yet left the European Union and the long-term economic effects of Brexit remain unknown. However, one of the trends which has attracted attention so far is a drop in real wages for UK workers, which many economists have put down to the immediate depreciation of the pound after the referendum and a subsequent rise in the cost of imports. Simon Wren-Lewis (Oxford University) explains that the picture is more complex than this, and that UK firms are anticipating a decline in the terms of trade following Brexit by not allowing nominal wages to rise to compensate for higher import prices.

This might seem easy. The depreciation immediately after Brexit, plus subsequent declines in the number of euros you can buy with a £, are pushing up import prices which feed into consumer prices (with a lag) which reduce real wages. But real wages depend on nominal wages as well as prices. So why are nominal wages staying unchanged in response to this increase in prices?

Image by Charlotte90T, (Flickr), licenced under Attribution-NonCommercial-NoDerivs 2.0 Generic (CC BY-NC-ND 2.0).

Image by Charlotte90T, (Flickr), licenced under Attribution-NonCommercial-NoDerivs 2.0 Generic (CC BY-NC-ND 2.0).

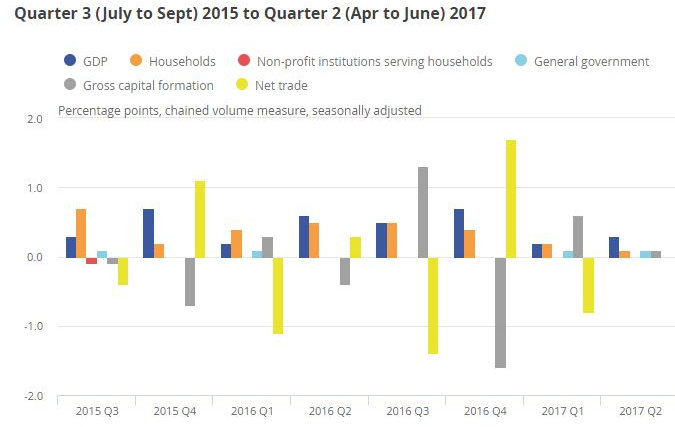

Before answering that, let me ask a second question. Why hasn’t the depreciation led to a fall in the trade deficit? Below are the contributions to UK GDP from the national accounts data. Net exports are very erratic, but averaging this out they have contributed nothing to economic growth since the Brexit depreciation.

Chart: Expenditure components percentage contribution to UK GDP growth, quarter on quarter

Note: Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (Jul to Sep), and Q4 refers to Quarter 4 (Oct to Dec). This chart does not include the statistical discrepancy and components may not sum to the percentage change in average GDP. Source: Office for National Statistics

The belief that the depreciation should benefit UK exports is based partly on the idea that exporters will cut their prices in overseas currency terms, making them more competitive. Yet at the moment, the majority of exporters in the UK seem to be responding to the depreciation not by cutting prices but by taking extra profits. If they keep their prices constant in overseas currency terms (from currency denomination data almost as many exports are priced in overseas currency as imports), sales will stay the same but profits in sterling will rise.

While this helps account for the lack of improvement in net trade, it increases the puzzle over why nominal wages are not responding to higher import prices. If exporting firms’ profits are rising because of the depreciation, why not pass some of that on to their workers?

One perfectly good answer is that the labour market is weak, and what has stopped real wages falling further is that firms do not like to cut nominal wages. In these circumstances, there would be no reason for exporters to share their higher profits with their workforce. So the immediate impact of the depreciation has not been a decline in the terms of trade (export prices/import prices), but instead a shift in the distribution between wages and profits. But many people believe that, with unemployment falling rapidly, the labour market is not weak.

There is another reason why exporters might be increasing profits but not sales, and not passing higher profits on to higher wages, which goes back to a point I have stressed before. We need to ask why the depreciation happened in the first place. To some extent the markets were responding to lower anticipated interest rates set by the Bank of England, but there is more to it than that. Brexit, by making trade with the EU more difficult, will reduce the extent of UK-EU trade. Furthermore, there are two reasons why Brexit is likely to reduce UK exports by more than UK imports.

The first is specialisation. Because countries tend to specialise in what they produce, they may not have firms that produce alternatives to many imports, making substitution more difficult. The EU produces many more varieties of goods than the UK, so they are more likely to be able to substitute their own goods to replace UK exports. The second is the importance for UK exports of services, and the key role that the Single Market has in enabling that. On both counts, to offset exports falling by more than imports after Brexit we need a real depreciation in sterling. Exporters will have to cut their prices in overseas currency terms, and a depreciation allows them to do this.

Of course, Brexit has not happened yet. We still get a depreciation because otherwise holders of sterling currency would make a loss. So firms do not need to cut their prices in overseas currency yet, allowing them to make higher profits. But these higher profits will be temporary, disappearing once Brexit happens. It would therefore be foolish to raise wages now only to have to cut them later when Brexit happens (no one likes nominal wage cuts). To restate this in more technical language, when Brexit does happen, the UK’s terms of trade will deteriorate as a response to export volumes falling by more than import volumes. Firms are in a sense anticipating that decline in the terms of trade by not allowing nominal wages to rise to compensate for higher import prices.

So before Brexit happens we are seeing a distributional shift between wages and profits, but once Brexit happens profits will fall back and we will all be worse off. For Leave voters who think this is all still just ‘Project Fear’, have a look at the national accounts data release that the chart above came from. It shows clearly that UK growth in the first half of this year has been slower than that in the US, Germany, France, Italy and Japan by a wide margin. What Leave campaigners called Project Fear is real and it is happening right now, but do not expect your government or some of your newspapers to tell you that.

This article originally appeared at Simon Wren-Lewis’ Mainly Macro blog and EUROPP. It gives the views of the author, not the position of LSE Brexit or the London School of Economics.

Simon Wren-Lewis is Professor of Economic Policy at the Blavatnik School of Government, Oxford University, and a fellow of Merton College.

The fall in real wages of UK workers is a trend that goes back to, at least, the 2008 banking crisis. The factors involved are varied and some appear to have been more prominent in some years than in others but I see no evidence that the trend has intensified since the 2016 Referendum.

Just a note: Your picture of the fruit and veg aisle is credited to “Public Domain”. But it isn’t PD, it’s in copyright and has a licence requiring you to correctly attribute the photographer. Link here:

https://www.flickr.com/photos/charlotte90t/8665650048/

Thanks for the heads up!

I voted remain but the above is a snapshot and frankly, bull****

I say that because Brexit is what I warned it would be. Brexit, can only slow down our descent, OR (where my money was) SPEED IT UP.

Brexit did not cause this. Its been going on since 1970’s. Here is a slightly wider look than the blink that this article shows.

http://bit.ly/2xOmPiX

Bloody awful work from an Oxford academic.

I’voted remain as well, but what we can do. We’ll lose a lot, especially in the automotive industry.