As large investors in the UK become more willing to inject capital in less liquid assets, the investment in the UK’s fast-growth company sector has been growing at increasing speed. It has now become obsolete to talk about recovery – we should now be talking about growth in unqualified terms.

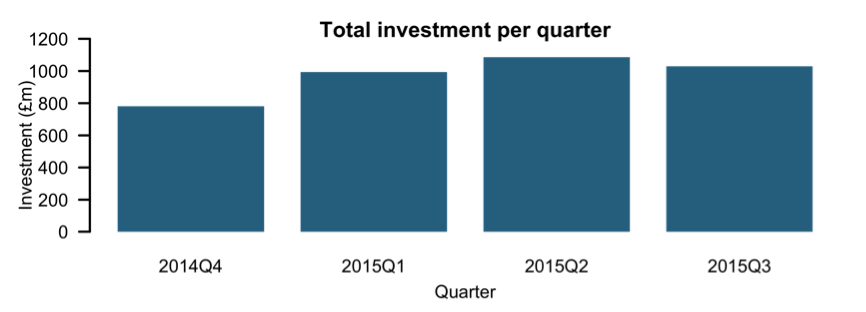

In our study of the UK equity investment market, we found that fast-growth businesses have managed to secure over £1 billion of equity investment in the third quarter of 2015, making it the best third quarter for equity fundraising activity since 2011. The total figure for the year has climbed to £3.1 billion, compared with £2.7 billion for the whole of 2014. With a full quarter still to be computed, the annual record has already been smashed.

A few, very large deals in the Life Sciences sector have contributed to the third quarter’s bumper figure, and it is evident that larger institutional investors are becoming more willing to invest in less liquid assets. Neil Woodford, well known for his investments in the sector, has invested through his funds into Mereo Biopharma, Immunocore and Oxford Nanopore — the latter two being the second and third largest holdings in his much-publicised Patient Capital Trust. Between Patient Capital and the Equity Income Fund, Woodford invested over £77m into Mereo and Immunocore this quarter. If we include Patient Capital’s smaller investment into Seedrs, the Woodford funds were responsible for over eight percent of total UK investment in the third quarter of 2015.

The case of Oxford Nanopore

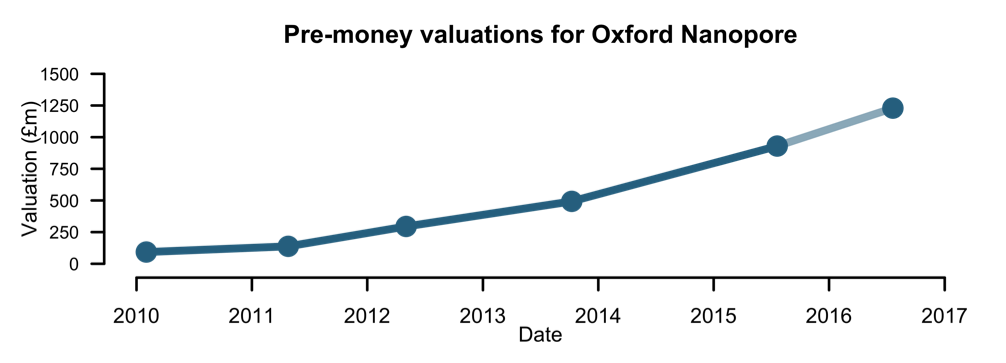

Oxford Nanopore, which is developing an electronic, single-molecule sensing system based on nanopore science, received an investment of £70 million in July and came close to reaching a £1 billion post-money valuation (£999,795,280). By American standards, the company is already comfortably a unicorn (a start-up whose market value reaches US$1 billion). At its current rate, the venture should be worth £1.23 billion by July 2016. Given such organisations are reticent about publicly sharing their valuations, our analysis gives a rare insight on an extraordinary growth trajectory.

Oxford Nanopore’s journey to this valuation has not been conventional. As the company says itself, “[we do] not have traditional venture capital investment; instead the investor profile more closely mirrors that seen of publicly listed companies.” The company has a number of investors who don’t normally commit themselves to such an illiquid investment class. Odey Asset Management invested when Nanopore’s filed accounts showed revenues of £149,000 but at a pre-money valuation of almost £500 million. The company’s most recently filed accounts show a loss of £37 million, but Woodford Patient Capital and others invested £70 million in July 2015. These investors are breaking away from their usual model because of their confidence in the game-changing proposition the company’s product presents.

Nanopore’s small and portable DNA sequencing device, called minION, is now being used by a community of scientists and researchers paying for access to it. The company is getting closer and closer to commercial viability. With numerous applications – including in personalised medicine – this product could soon start bringing in serious revenue.

Among other Oxford spinouts, First Light Fusion is pioneering new techniques for achieving the colossal temperatures and pressures required to produce energy from nuclear fusion. Investors have noticed: Parkwalk, IP Group, Invesco Perpetual and SandAire contributed £14 million in the first tranche of a £22.7 million round in August, valuing the company at nearly £26 million (pre-money). Given that the International Thermonuclear Experimental Reactor (ITER) project is expected to cost at least €13 billion, First Light’s round may seem small beer. But if they contribute to successful fusion reactors, the exit multiples (the return on the capital invested upon exit) could be stellar.

Another spinout from the University, Oxford BioDynamics received $7 million at a pre-money valuation just shy of £100m in July, for its technology that identifies biomarkers in patients. Biomarkers can be used to predict how a patient will react to certain treatments. It is not known at this time who participated in this round but the company’s previous backers include Odey Asset Management and the Vulpes Life Science Fund, a fund run by hedge fund billionaire Stephen Diggle’s family office.

There is no sign of funds running out. Oxford Sciences Innovation (OSI) is setting up a £320 million fund to support spinouts from the University. OSI made their first investment into Oxford Flow in September.

Given the large amounts of investment these companies are receiving, their prominent backers and their change-the-world propositions, we will be keeping an eye out in the coming years to see just what kind of returns they can net.

♣♣♣

Notes:

- This post is based on the author’s report The Deal Q3 2015: Making Sense of UK Equity Investment, for Beauhurst, a provider of data on fast-growth companies in the UK.

- This post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: DNA nanopore (in blue), a tube formed of folded strands of DNA UCL Mathematical and Physical Sciences CC-BY-2.0 All graphs provided by Beauhurst.

Henry Whorwood is a Research Analyst at Beauhurst. He is the lead author of The Deal, Beauhurst’s quarterly review of the fast-growth company landscape. When he isn’t busy with report writing, he splits his time with the Sales team, where he liaises with the technology transfer arms of UK universities. He has a Bachelor’s degree in Classics from the University of Oxford.

Henry Whorwood is a Research Analyst at Beauhurst. He is the lead author of The Deal, Beauhurst’s quarterly review of the fast-growth company landscape. When he isn’t busy with report writing, he splits his time with the Sales team, where he liaises with the technology transfer arms of UK universities. He has a Bachelor’s degree in Classics from the University of Oxford.