Portland cab drivers protest, by Aaron Parecki, under a CC-BY-2.0 licence

Portland cab drivers protest, by Aaron Parecki, under a CC-BY-2.0 licence

Amazon, Airbnb, Uber, Facebook have been hogging the news. The headline figures are arresting. Amazingly, Uber has already surpassed BMW’s market capitalization. A seven-year old upstart company with a mere 6,700 employees is valued more highly than a hundred-year old company with one of the world’s best known automotive brands and 122,000 employees.

What links Uber and the others is that their success is not built on an exciting new product or service. No, their success is about their platforms. Look around. Platforms are taking over the world. In fact, of the publicly traded companies by market capitalization, the top five are based on platform business models.

Platform models are, per se, nothing new. For example, newspapers and commercial malls have been operating a platform model for decades. They connect users and providers while facilitating their value exchanges. What makes these emerging business models dominant and pervasive is the digital element. The internet and the cloud enable a company to start a platform at minimal cost, while scaling it globally at incredible speed. Airbnb can add new listings, which for its hotel competitors translates to “building new hotel rooms”, almost instantaneously. Airbnb can do so because it does not carry the resources constraint of traditional business models.

Platform companies have already disrupted some industries and will inevitably disrupt more. The platform revolution is a reality in industries such as media (YouTube), telecom (WhatsApp), hospitality (Airbnb), mobility and taxi services (Uber) and others. In his book Platform Revolution, Marshall Van Alstyne, a Professor at Boston University, identified the next wave of industries which might be disrupted by platform business models as: automotive, banking, education, health care and energy.

This clamour of dynamic growth and excited commentary has had an impact on many large incumbent companies. But hearing does not necessarily equate to understanding. Consider one of the world’s largest global energy companies, which for this article’s sake, we shall call “UtilityCo”. The company started to feel the competitive heat from platform models and wanted to respond. However, UtilityCo was suffering from three problems we have seen at many incumbents.

First, it jumped in. Inspired or frightened by the hype UtilityCo set about creating its own platform without analysing if a platform model suited the company or not. The initiative quickly lost power. Incumbents need to articulate their broad competitive game. Platform models might be partially applicable to their industry or not at all. For instance, it is questionable at best, whether a mining company would be suitable for a platform model.

Second, UtilityCo was familiar with supply-side economies of scale, but less so with demand-side economies of scale, also known as network effects. Network effects occur when the platform’s value to any given user largely depends on the number of users connected or using the platform. For example, the more apps are available at the Apple Store, the more value is generated for the users, which in turn makes it more attractive for app developers to develop new apps, which again attracts more users. The platform’s value grows exponentially with the increase in the number of users, providers and their interactions.

The third problem was an etymological one. Platform achieved buzzword status at UtilityCo and was frequently misused and mixed up. One business unit launched an online e-commerce service leveraging its existing customer base, incorrectly calling it a new “platform model”. At the same time, various C-suite executives were using platform terminology with reference to an internal technology/IT layer on which to build multiple services. Clarity on what a platform model is and how it works is the minimal requirement towards building one and responding properly to an external threat.

So, how can incumbents lift the cloud of misunderstanding and restore clarity to their platform strategies? Based on our consulting experience, there are five things to know to get started in the platform game:

- Don’t mix up “platform business model” and “technology platform”. While the digital disruption certainly created digital/cloud platforms and enabled service platforms, these should not be mistaken for platform business models. Here is why. IT and service platforms, such as HSBC’s online banking or Walmart’s online shopping, lack the crucial network effects. Platform business models have the potential to significantly disrupt industries by leveraging the network effects.

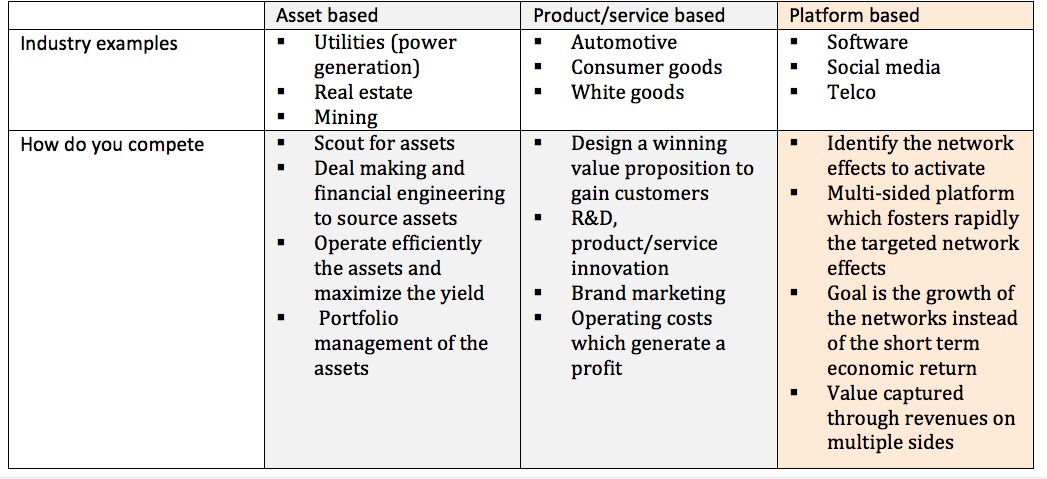

- Understand which is your broad competitive game. We identified three broad categories: asset-based, product/service-based and platform-based. The goal is not for every company to shift to a platform-based model but rather to understand how you should compete in your own game while reacting to platform threats. In today’s digital world, disruptors are likely attacking you with a platform model, so at minimum you need to know their way of thinking and analyse their plots with a very good understanding of the platform-based game.

- Strategise your hybrid model. Incumbent companies, while exploiting the strengths and assets of their original competitive game, can fight back against platform disruptors by developing hybrid models (i.e. some platform elements on top of their existing products and services). Apple might be the poster child of the hybrid platform company. It retains its lucrative handset business while also being successful in orchestrating its App Store platform. Incumbents such as Nike, John Deere and GE are rapidly incorporating platform elements into their business models.

- Strategically choose the sides of your platform. Start by identifying the two starting sides of the platform, usually the user and the core provider. Then, think about adding new sides to the platform. A “multi-sided” platform has a number of different user groups interacting on the platform. For example, Intuit’s QuickBooks evolved from a product to a full multi-sided platform. Small and medium-sized enterprises (SMEs) interact with the platform to input and monitor their expenses. On the other side accountants seamless integrate their professional QuickBooks with raw accounting data to elaborate financial reports and tax filings. On another side, banks interact with the platform to enable a seamless connection to their customers’ bank accounts, improving their customers’ experience as well as their service offering. Recently, QuickBooks opened its platforms to developers interested in creating and selling their add-on software and apps to their SMEs’ customer base.

- Understand the types of network effects. Platform models increase their value for users and providers and as consequence increase their competitive advantage because of the network effect they leverage. There are three types of network effect, each requiring a different way of exploitation. We like to classify network effects into these categories:

- Communication: Increase in the users of the product/service lead to direct increases in value for the user (Facebook)

- Complementarities: A product or service whose value increases thanks to the development of complementary products and applications developed by other parties (Apple’s iPhone with its App Store)

- Data advantage: Increase in users of the product/service generate better data which makes the service performing better and better vs. the competition (Google search).

Incumbents need to identify the type of network effects they want to exploit on their platforms and strategise a virtuous cycle attracting users and providers.

Incumbents’ business models are more at risk than ever. A recent survey indicated that about half of the S&P 500 will be replaced over the next 10 years. Platform models are an integral part of the ongoing and future disruption. Incumbents should move now from “share of voice” to “share of understanding”. Time is critical. Unfortunately, the hotel and taxi industries are learning the lesson the hard way.

♣♣♣

Notes:

- The post gives the views of the author, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy.

Alessandro Di Fiore is the Founder and CEO of the European Centre for Strategic Innovation (ECSI) and ECSI Consulting, based in London. He is a consultant, author and media commentator on strategy and innovation. Email: adifiore@ecsi-consulting.com

Alessandro Di Fiore is the Founder and CEO of the European Centre for Strategic Innovation (ECSI) and ECSI Consulting, based in London. He is a consultant, author and media commentator on strategy and innovation. Email: adifiore@ecsi-consulting.com