One of the areas frequently mentioned as ripe for improvement by applications of the broad group of technologies known as blockchain, or distributed ledger technology (DLT), is capital markets. In the “ledger nirvana” of many blockchain proponents, market counterparties use consistent sets of trade data. They also use smart contracts, computer protocols that facilitate, verify, or enforce the negotiation or performance of a contract, or that make a contractual clause unnecessary. These contracts apply consistent business logic to produce the outputs required to operate a business trading securities, currencies or derivatives.

Experiments have shown that the blockhain concept is feasible in capital markets, and blockchain-related companies have made considerable investments. However, major obstacles must be overcome if the technology is to ever be widely adopted by the financial industry. None are completely insurmountable, but all could take considerable time and effort. Time and effort that would need to be balanced against the cost of adopting alternative technological approaches to improving cost and control in investment banking.

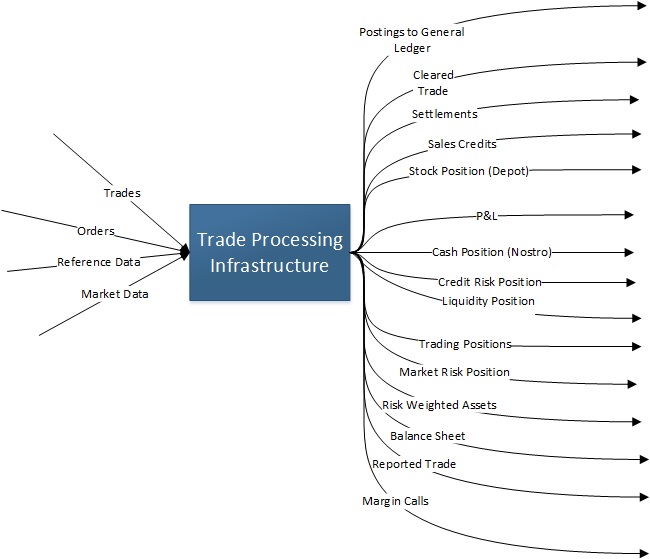

Figure 1. Trade processing infrastructure

A distributed ledger-based solution to trade processing needs to be tangibly better in terms of cost, control, security, and resilience than existing financial market infrastructure, much of which generally works remarkably well. Examples of the infrastructure that keeps markets working includes the systems of the Central Securities Depositories and CLS Bank in the foreign exchange market.

In the “ledger nirvana”, settlement infrastructure is typically based on the assumption of cash and securities “on ledger.” In other words, cash or securities primarily have legal existence as data on a distributed ledger, or they are “tokenised”. Tokenised simply means there is a legally valid representation of assets that can be used for settlement purposes, even though the primary record of the assets may be a bank account or a share registry.

Some progress has been made in this area. Overstock.com, an online outlet store, last year issued shares on its T0 platform, which includes the use of a “private” distributed ledger for trade core processing, with transactions ultimately being recorded on the Bitcoin blockchain. This is a step forward legally and technically, but is still a long way from making a significant impact.

Genuine “cash on ledger” is even more problematic. Fundamentally, real-world fiat currency needs to be a ledger version of central bank reserves, which requires the co-operation of central banks and legal changes, depending on the jurisdiction, or commercial bank-issued money.

Commercial bank-issued money would be the direct economic and legal equivalent of the money that is represented today as positive balances in customers’ bank accounts. Direct equivalence, however, brings the challenges faced in the existing world. Commercial bank money carries credit risk against the issuing bank and needs a mechanism (equivalent to the central bank clearing systems) to control the credit risk that builds up between clearing banks as funds are transferred.

For securities such as government bonds and more liquid equities, mechanisms would need to be built to allow them to not just be bought and sold but to be provided as collateral between banks, to CCPs (Central Counterparty Clearing House), and to central banks through their repo process.

A smart contract that carries out the mechanics of a financial product, such as the work done by blockchain specialist firm Axoni on equity swaps or Barclays and R3, a consortium of financial institutions, on interest rate swaps, represents a step forward in supporting the lifecycle of derivatives trades using the distributed ledger technology.

However, there are many systems within the trading infrastructure of a commercial bank that execute, enrich, process and aggregate trades and trade events. Simply programming this logic in a new technology is not in itself an achievement. A smart contract that performs the basic mechanics of trade processing would still need to interact with credit risk, market risk, liquidity management, position keeping, profit and loss calculation/aggregation, regulatory reporting, derivative clearing, sales credits and many other systems.

What is frequently forgotten is that simply having a ledger of trades does remove the need for what is frequently the most complicated and expensive system in a bank, the general ledger. A typical general ledger system is not just a list of transactions. It also is a list of accounting rules and policies that are applied to the transactions, often requiring the support and judgement of a large finance department.

In many markets such as spot FX, futures, equities and the more liquid bond issues, most trading (including much order processing) takes place at very high speed using very expensive and sophisticated infrastructure. It can be argued that this speed does not add significant value to society or the economy, but that is the way many markets operate. There would be great resistance to any attempt to slow down trading to allow distributed ledger technology, which is inherently slower, to replace the current pre-trade infrastructure. A further obstacle is that the post-trading processing costs of electronically executed trades are considerably lower than for the more traditional (and error-prone) voice trading. This means distributed ledger needs to offer a significantly better post-trade solution for the overall volumes of trades in an asset class.

“Ledger Nirvana” also would position distributed ledgers in markets as “financial market infrastructure” within the scope of the Bank for International Settlements “principles for financial market infrastructures.” These principles are incorporated in law in most developed countries, and are very demanding. They represent a high, but necessary, hurdle for DLT to clear.

Overlapping with the BIS principles are the banks’ own requirements for high-volume processing, resilience and security. Just as the existence of a distributed ledger does not automatically remove the need for a general ledger, the use of cryptographic techniques inherent in DLT does not make a system secure from a bank’s perspective.

In “Ledger Nirvana,” the trade is the settlement. A trade is booked and value is exchanged. However, this creates significant problems for today’s business models, business models that cannot simply be wished away by the DLT enthusiast. Most capital markets work implicitly on time delays. Huge daily volumes are traded and processed, but a market maker only needs to be flat (in most markets) by the end of the day. The settlements teams only need to transfer the net settlement amounts at the end of the settlement cycle. In the world of “trade equals settlement,” a market maker can only create liquidity for the market in one of two logical ways.

- They can “warehouse,” i.e., stockpile what they are buying and selling. Under current regulations this incurs capital charges that would make market making completely uneconomical.

- If they do not warehouse, selling by a market maker would require a mechanism for near instantaneous borrowing of securities and buying. Buying would require either a large credit facility or near instantaneous financing of the bought assets.

Overall, these barriers could delay “Ledger Nirvana” by many years or potentially make it completely unachievable.

♣♣♣

Notes:

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Clouds, by Ana_J, under a CC0 licence

- Before commenting, please read our Comment Policy.

Martin Walker is Banking and Finance Director at the Center for Evidence-Based Management (CEBMa) and produces research for financial consultancy Finadium. He has extensive experience in investment banking IT and operations. His roles included Global Head of Securities Finance IT at Dresdner Kleinwort and Global Head of Prime Brokerage Technology at RBS Markets. He also held roles at Merrill Lynch and HSBC Global Markets, where he was the Blockchain lead in Markets Operation. Additionally, Martin worked for the R3 CEV Blockchain collaborative on product development and has published two papers on the topic: Blockchain And The Nature of Money, and Bridging the Gap Between Investment Banking Architecture and Distributed Ledgers (R3 CEV Research – Mar 2017)

Martin Walker is Banking and Finance Director at the Center for Evidence-Based Management (CEBMa) and produces research for financial consultancy Finadium. He has extensive experience in investment banking IT and operations. His roles included Global Head of Securities Finance IT at Dresdner Kleinwort and Global Head of Prime Brokerage Technology at RBS Markets. He also held roles at Merrill Lynch and HSBC Global Markets, where he was the Blockchain lead in Markets Operation. Additionally, Martin worked for the R3 CEV Blockchain collaborative on product development and has published two papers on the topic: Blockchain And The Nature of Money, and Bridging the Gap Between Investment Banking Architecture and Distributed Ledgers (R3 CEV Research – Mar 2017)