Society could save billions of dollars every day if trading in commodities, energy and securities was made more competitive and efficient through a minor rule change. That is the topic of my new research paper.

Every day, auctions and exchanges around the world trade bonds, stocks, currencies, electricity, metals, commodities, securities and financial instruments worth trillions of dollars. Thus even small changes in transaction prices could save a lot of money for society and tax payers.

Most trading platforms apply “precedence rules” that determine in which order instructions from traders should be executed – normally sell orders with a low ask price and buy orders with a high bid price are executed first. Precedence rules also decide how orders should be ranked in case of ties, for example when two traders submit sell orders with identical offer prices. Such a rule is often referred to as a “tie-breaker” or “rationing rule”.

Some exchanges give priority to the order that was submitted first. Other exchanges might prioritise an order with a large volume over a small order with the same offer price, or the other way around. Many multi-unit auctions ration offers with identical offer prices proportionally.

The clearing process can be illustrated with the following example. Assume that Supplier A submits an offer that indicates that he or she wants to sell 3000 securities if the price is £110/unit, 1500 securities if the price is £105 and 1000 securities if the price is £100. At the same time Supplier B indicates that he or she wants to sell 5000 securities if the price is £110/unit, 3500 securities if the price is £105 and 2000 securities if the price is £100. Assume that the procurer, who organises the auction, wants to buy 3500 securities. He or she notes that £105 is the lowest price, at which 3500 units can be bought, so it sets the marginal price at £105/unit.

Initially the securities that the suppliers are willing to sell at £100 (below £105) are allocated. Thus, initially 1000 securities are bought from Supplier A and 2000 securities are bought from Supplier B. This leaves 500 securities to procure, which is 25 per cent of the remaining supply at the marginal price (another 500 units from Supplier A and another 1500 units from Supplier B). Thus, with proportional rationing (pro-rata) the procurer would buy another 125 units (in total 1125 units) from Supplier A and another 375 units (in total 2375 units) from Supplier B.

If the auction uses uniform-pricing, as in many electricity markets and in the security auctions by the US treasury, then the price for each transaction is £105. Treasuries in Europe often use discriminatory pricing, and in that case Supplier A and B are paid a lower price, £100, for the units that they have offered to sell at £100.

My paper presents a new tie-breaker, which is different in that orders with the same offer price are prioritised according to whether the marginal price is high or low. Offers become more competitive if the rationing rule gives higher priority to sell orders with a large volume when ties occur at low offer prices. The pro-competitive effect would be similar in a sales auction when applying pro-competitive rationing to buy orders. Though in those cases the rationing rule should give higher priority to buy orders with a large volume when ties occur at high prices.

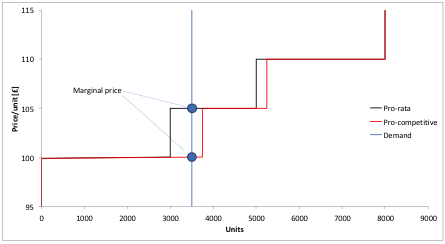

In a market with imperfect competition, it is profitable for suppliers to overstate their costs in their offers in order to boost the transaction price. In such cases the new rationing rule will make bidding more competitive. In the example above, it would increase the supply at £100. How much supply increases depends on the number of suppliers, their costs, uncertainties in the market and how much rationing is needed. Nevertheless, as qualitatively illustrated in the figure below increased supply could reduce the marginal price and thereby the procurement cost of the auctioneer.

Figure 1. Example that qualitatively illustrates how total supply of securities depends on the rationing rule, pro-rata and pro-competitive rationing

In general, pro-competitive rationing would result in less strategic trading orders that better represent the true preferences of traders. This improves the efficiency of the auction, i.e. procured units are to a larger extent supplied by producers that have the lowest cost of providing them, and units are to a larger extent sold to buyers that value them most.

The pro-competitive effect is largest in markets such as security exchanges, where orders are entered at just a few price levels, so that rationing becomes important. The paper shows that if orders are only entered at two price levels, then the new rationing rule could have the same effect as if the number of traders was doubled, thereby increasing the competition and forcing the trade to be conducted more efficiently.

In a procurement auction where sell orders are entered at 10 different price levels with a mark-up of around 10 per cent, the procurement price can be reduced by roughly 1 per cent – leading to huge savings on large contracts. This means that government bodies that carry out procurement auctions or sell emission permits or treasury bills would save billions in tax payers’ money.

I have developed the new trading rule at the Research Institute of Industrial Economics (IFN) in Stockholm with the help of David Newbery and Daniel Ralph at University of Cambridge and Lawrence Ausubel at University of Maryland. The cost to implement the new pro-competitive rule would be negligible compared to the savings, when the turnover is high.

♣♣♣

Notes:

- This blog post is based on the author’s paper Pro-competitive Rationing in Multi-unit Auctions, The Economic Journal, October 2017.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: NYSE trading floor, 26/9/1963, by Thomas J. O’Halloran, via Wikimedia Commons

- When you leave a comment, you’re agreeing to our Comment Policy.

Pär Holmberg is Associate Professor in Economics and has a Ph.D. in Electric Power Engineering. He is a Senior Research Fellow of the Research Institute of Industrial Economics (IFN) in Stockholm and an associate of Energy Policy Research Group (EPRG), University of Cambridge. Pär’s research focuses on electricity markets and market design.

Pär Holmberg is Associate Professor in Economics and has a Ph.D. in Electric Power Engineering. He is a Senior Research Fellow of the Research Institute of Industrial Economics (IFN) in Stockholm and an associate of Energy Policy Research Group (EPRG), University of Cambridge. Pär’s research focuses on electricity markets and market design.