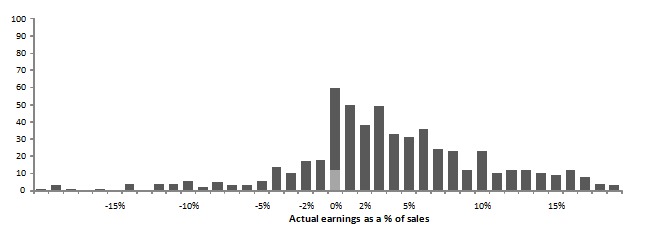

The first picture shows the distribution of actual earnings in our study on target setting (see the study in brief box below) and replicates a well-established finding that reported earnings exhibit a ‘discontinuity at zero’ (meaning that there are disproportionally fewer firms with small losses compared to small profits), which one might surmise perhaps suggests that firms ‘manage’ earnings to avoid small losses, or if that is too strong an inference for your liking, that they have a ‘distaste’ (for whatever reason, and many have been proffered) for slight losses.

Figure 1

Figure 2

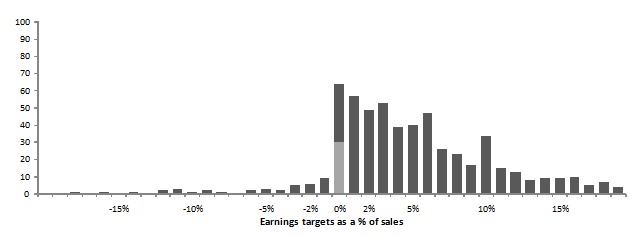

Earnings scaled by sales are plotted in 1% intervals (eg, 0% stands for return on sales equal or greater than 0% and smaller than 1%). The first figure shows 561 entities with 2008 actual earnings between ‑20% and 20% of sales. The lighter bar at 0% represents 12 entities with 2008 actual earnings exactly equal to zero. The second figure shows 568 entities with 2008 earnings targets between ‑20% and 20% of sales. The lighter bar at 0% represents 30 entities with 2008 earnings targets exactly equal to zero.

Be that as it may, what’s new in our study is to present distributions of earnings targets in Figure 2, which shows that the ‘discontinuity at zero’ exists for earnings targets as well; actually, a comparison of the two pictures suggests that the discontinuity at zero is even more pronounced for target earnings than for actual, reported earnings.

Moreover, we find that earnings targets set at zero are abnormally difficult to achieve compared to other targets. For example, our evidence suggests that the perceived likelihood of meeting a zero earnings target is 24 percent lower; that is, targets set at zero are clearly harder to achieve.

Combined, our findings imply that firms are reluctant to set negative targets and that the widely documented discontinuity at zero in distributions of reported earnings also extends to earnings targets. Moreover, we find that zero or slightly positive earnings targets are not only more prevalent than are targets just below zero, they are also more difficult to achieve than all other targets.

What might that mean? It indicates that firms are reluctant to set negative targets and instead prefer to ‘stretch’ earnings targets to zero even if it renders such targets difficult to achieve. This suggests that firms do not want relatively small losses or ‘slight misses’, and that they do this by way of providing bonuses for targets at profit. Managers thus have incentives to work hard to prevent losses. What’s there to lose, then, other than the loss?

| The study in brief |

|---|

| An important element of firms’ management control systems is the practice of establishing targets for future performance. Such practices serve to organize and coordinate firms’ decisions and form the basis for performance evaluation and compensation. We provide novel empirical evidence about firms’ target-setting practices based on a survey of compensation practices at 666 entities. We examine the extent to which firms use past performance as a basis for setting earnings targets in their annual bonus plans and assess the implications of such targets for managerial incentives. Perhaps the key finding is about ‘target ratcheting’ (see blog post), where prior studies find that firms revise performance targets upwards when their managers exceed prior-year targets, yet do not revise targets downward (or revise them less) when managers fail to meet prior-year targets. These target-ratcheting practices are interpreted as evidence of counter-productive incentives because they presumably motivate managers to withhold effort in order to avoid difficult targets in the future. We argue that this interpretation is incomplete and makes inconsistent assumptions about how information about prior-year performance is used when setting future targets. |

♣♣♣

Notes:

- This post is based on the paper Earnings targets and annual bonus incentives, co-authored by Wim A Van der Stede, Raffi J Indjejikian, Michal Matĕjka and Kenneth A Merchant (2014), The Accounting Review, 89(4), 1227-1258 (ISSN 0001-4826). Available also on SSRN.

- This post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image by Bogdan Suditu, under a CC-BY-2.0 licence

Wim A Van der Stede is the CIMA Professor of Accounting and Financial Management, and Head of the LSE’s Department of Accounting. His research interests pertain broadly to the study of management control systems, i.e., the study of performance targets and the budgeting processes used to set them; performance measurement and evaluation; and incentive systems that relate performance evaluations to the provision of rewards. He tweets at @stede_w

Wim A Van der Stede is the CIMA Professor of Accounting and Financial Management, and Head of the LSE’s Department of Accounting. His research interests pertain broadly to the study of management control systems, i.e., the study of performance targets and the budgeting processes used to set them; performance measurement and evaluation; and incentive systems that relate performance evaluations to the provision of rewards. He tweets at @stede_w