Business/cash, by PublicDomainPictures, under a CC0 licence

Business/cash, by PublicDomainPictures, under a CC0 licence

Christopher Hood and Rozana Himaz’s retrospective on UK austerity argues that the current ‘period of public spending restraint’ fits into a pattern of longer but less deep government actions. But their account contains a logical error that leads to underestimating both the severity of the present action and the damaging effects on the economy as a whole.

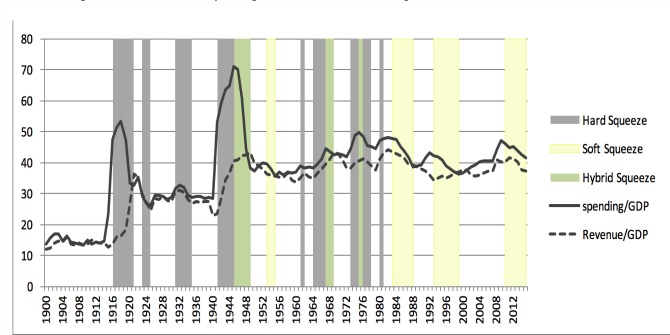

Hood and Himaz argue that the ‘recent fiscal squeeze’ is ‘soft’ compared to 16 earlier squeezes throughout the 20th century. Their definition of ‘soft’ and ‘hard’ is based on whether government spending falls and/or government revenue rises as a share of GDP or (soft)/and (hard) in volume terms (chart reproduced below).

Figure 1: UK Government Spending and Revenue as a Percentage of GDP, 1900-2015

Source: Hood & Himaz, 2016

The main difficulty with this approach is that it ignores the macroeconomic relations in the system. Given government expenditure has an impact on the economy in aggregate, then all three of the variables – revenues, expenditure, and GDP – will reflect this impact as well as any policy action. Conversely, wider economic conditions also distort outcomes: for example, government spending growth was relatively robust over the ‘soft squeeze’ of the late 1980s, but was outstripped by stronger GDP growth.

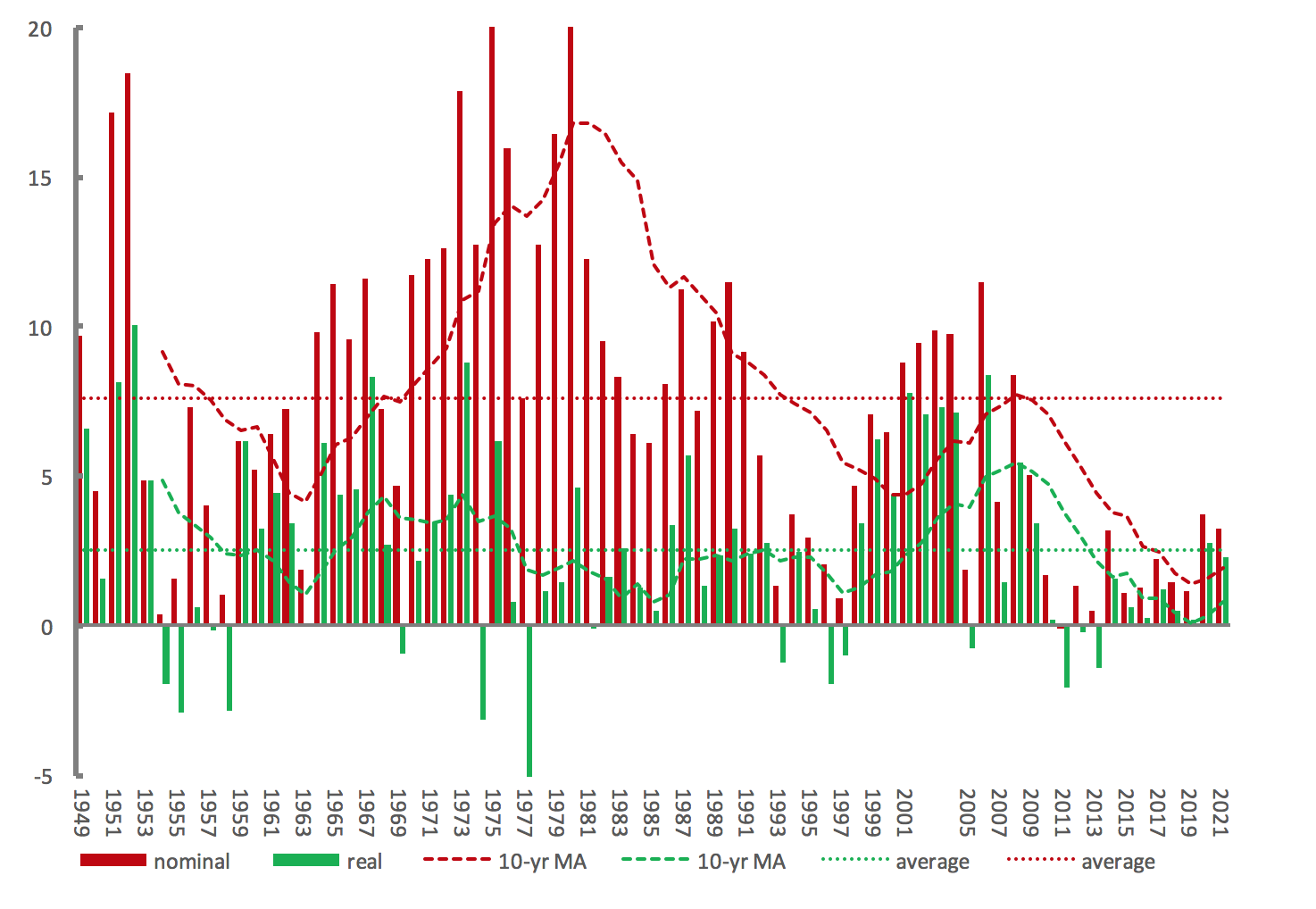

The most direct way to assess fiscal policy is on the basis of government consumption and investment expenditure, because they are most directly under the control of government policy and not greatly affected by any feedback from changed economic conditions. The chart below shows that in both nominal and real terms, the scale and duration of the current programme of cuts is clearly without precedent in the post-war period. In the decade to 2019, the average annual growth of government spending is projected to be 1.4 per cent in nominal terms and 0.1 per cent in real terms.

Figure 2: Annual growth in general government final consumption and fixed capital expenditures, 1949-2021

Note: Real terms figures have been derived on the basis of the aggregate GDP deflator, given complexities associated with the ‘output approach’ to volume estimates of government expenditure. For example, outputs are measured on the basis of various performance indicators, which may distort behaviour and hence outputs in other areas that are not measured.

Hood and Himaz are right that, in general, it is the rate of growth that has been reduced, rather than the level of spending. However, looked at in real terms there were cuts in the level of spending for three consecutive years over 2011 to 2013 – an unprecedented result.

Equally on a macroeconomic view, cuts to the growth of expenditure are still greatly problematic. Cuts have meant no less unprecedented weakness in GDP growth over the post-2010 period, with the associated impact on real wages, the wider dis-inflationary environment and the obvious repercussions on the public sector finances (see for example the TUC submission on the 2016 Autumn Statement). Hood and Himaz observe that “further austerity looks like a distinct possibility on the next parliament”. Certainly that would be so on the present course: indeed on the basis of that analysis, it is hard to see why austerity should ever come to an end.

The only comparable peacetime episode to the current period of austerity is the dark years from the Geddes Axe (of 1922-23) through gold standard membership into the 1932-33 cuts as the great depression intensified (set out in the report of the May Committee that was commissioned by the Labour government). In real terms, the spending cuts were in fact less severe than the current cuts, as a result of the outright deflationary conditions that then prevailed – though my sense is that nominal figures are probably the better guide. The cuts finally came to an end in 1934 after twelve years and spending materially expanded. The parallel political and economic trauma throughout was probably without precedent.

Figure 3: Annual growth in general government final consumption and fixed capital expenditures, 1949-2021

Inevitably, the demobilisations after each of the world wars involved very large spending cuts, but these are outside of the scope of this discussion (obviously the y-axis of the chart has been cut off). Overall, the cuts over the 1920s/30s were more severe in size and effect – but it is a chilling thought that this episode is the only relevant precedent.

Lessons from history can be easily ignored if brutal policy action is nullified through neglecting macroeconomic relations.

♣♣♣

Notes:

- This blog post appeared first on LSE British Politics and Policy.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy.

Geoff Tily is a Senior Economist at the TUC (Trade Union Congress). For 25 years he was a member of the government statistical and then economic services, most recently as a macroeconomic adviser in HM Treasury. He’s the author of the book Keynes Betrayed,

Geoff Tily is a Senior Economist at the TUC (Trade Union Congress). For 25 years he was a member of the government statistical and then economic services, most recently as a macroeconomic adviser in HM Treasury. He’s the author of the book Keynes Betrayed,