The New York Times building, by Haxorjoe, under a CC-BY-SA-3.0 licence

The New York Times building, by Haxorjoe, under a CC-BY-SA-3.0 licence

Firms that are more visible in the press are better governed and more profitable. But investors underestimate the value of visibility and could profit from investing into high-visibility firms.

In our study, ‘The Value of Visibility’, we analyse 90 years of The New York Times’ coverage of more than 22,000 publicly listed US firms, to show that managers of firms with high coverage are subsequently less likely to exploit the firm’s shareholders. Compared with firms with no visibility in The New York Times, a firm amongst the 20 per cent most visible corporations experiences 1.98 per cent more profitability growth.

Investors seem to undervalue this positive effect of visibility: An investment strategy seeking to exploit the high profitability growth of visible firms by buying firms with high coverage in The New York Times and selling firms with low coverage is very profitable compared with other well-known investment strategies.

More

‘Sunlight is said to be the best of disinfectants.’ (Louis Brandeis, 1914) The idea that light heals seems to hold true in the corporate world. We analyze the impact of firm-specific newspaper coverage on firms’ governance, value and stock prices. Consistent with Brandeis’ quote, we find that more visible firms are better governed and more profitable. We also show that investors underestimate the value of visibility, so that the stocks of visible firms trade at a discount.

Press coverage creates better managed firms

To measure the visibility of firms, we use newspaper coverage. We extract ninety years of coverage from 1924 to 2013 on more than 22,577 publicly listed US firms from the online archive of The New York Times. Using this large dataset – based on over 9.6 million articles – we show that firms with high newspaper coverage subsequently improve their corporate governance. Their managers become less likely to exploit the firm’s shareholders, e.g. via excessive severance packages (so called ‘golden parachutes’) or anti-takeover measures with the intention of protecting their jobs (‘poison pills’).

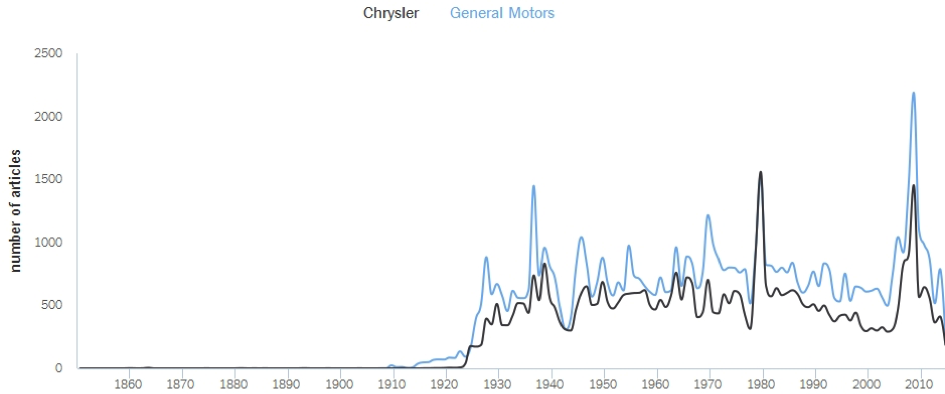

Figure 1: Yearly number of articles in the New York Times about “Chrysler” and “General Motors” from 1851 to 2013. Source: http://chronicle.nytlabs.com/

…and increases profitability

Additionally, highly visible firms exhibit higher profitability growth. Compared to firms with no newspaper coverage, a firm amongst the 20 per cent most visible ones exhibits about 1.98 percentage points more profitability growth looking forward. Hence, the idea that shining light on the activities of managers improves corporate wellbeing seems to hold true.

Investors could exploit the value of visibility

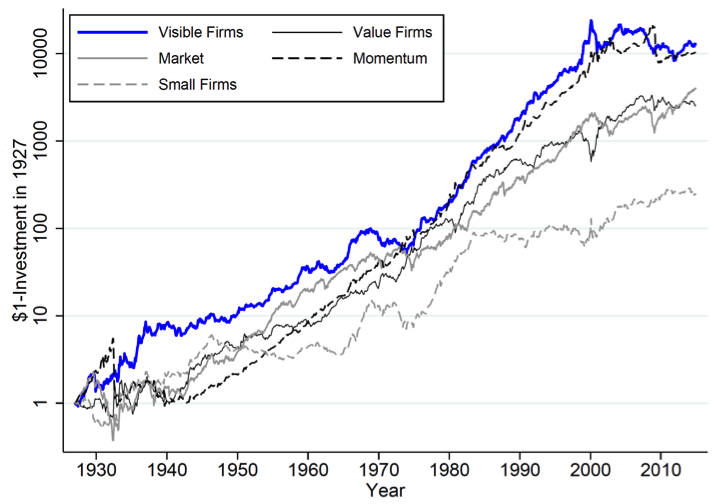

However, in contrast to Louis Brandeis, investors neglect this value of visibility. Future stock returns of highly covered firms are persistently higher than those of firms with little newspaper coverage. An investment strategy seeking to exploit this effect by buying high-visibility firms and selling low-visibility firms is very profitable when compared to other well-known investment strategies on a volatility-adjusted basis:

Figure 2: 1927-2014 value of $1-Investment in 1927 into five investment strategies, adjusted to have the same volatility as the overall US stock market.

Notes: ‘Visible Firms’ is a strategy buying firms with high firm-size-adjusted newspaper coverage and selling low firm-size-adjusted coverage firms; ‘Market’ is a strategy that passively invests in the US stock market; ‘Small Firms’ is a strategy buying low-market-capitalization firms and selling high-market-capitalization firms; ‘Value Firms’ is a strategy that buys firms with high book-to-market-ratios and sells their low book-to-market-ratio counterparts; ‘Momentum’ buys last year’s winner stocks and sells last year’s loser stocks. Source: Hillert/Ungeheuer (2016)

The high stock returns of more visible firms challenge the common view of visibility decreasing a firm’s cost of capital by attracting new investors. However, these high returns of visible firms still imply a positive role for the media specifically, and for firm visibility in general: Visibility creates value through improving managers’ behavior and increasing future profits. An additional channel may be the advertising effect of high visibility. Visibility can make potential customers aware of the firm’s products and services. In line with this idea, visible firms show stronger future sales growth.

So what should we do?

Our findings have two main implications. First, investors should re-evaluate how they incorporate firms’ visibility into pricing stocks. If they take the positive visibility effects properly into account, the historical price discount of visible firms relative to their future profitability should disappear. Second, investors and regulators should exploit the positive impact of visibility on manager behavior and firm values. In the information age, online visibility can be increased at hardly any costs. Disclosure of information by firms, encouraged by self-interested investors or legally prescribed by regulators, can prevent value-destruction by managers. As an illustration, more transparency with respect to emission testing procedures within Volkswagen might have kept managers honest, preventing the ongoing value-destroying emissions scandal.

♣♣♣

Notes:

- This blog post is based on the authors’ paper The Value of Visibility, presented at the 2016 Congress of the European Economic Association in Geneva.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy.

Michael Ungeheuer (michael.ungeheuer@gess.uni-mannheim.de) is a PhD candidate at the University of Mannheim‘s Graduate School of Economics and Social Sciences. He is interested in investor behavior and asset pricing. In particular, Michael specializes on the role of investor attention and firm visibility in financial markets.

Michael Ungeheuer (michael.ungeheuer@gess.uni-mannheim.de) is a PhD candidate at the University of Mannheim‘s Graduate School of Economics and Social Sciences. He is interested in investor behavior and asset pricing. In particular, Michael specializes on the role of investor attention and firm visibility in financial markets.

Alexander Hillert (hillert@safe.uni-frankfurt.de) is an assistant professor at the University of Frankfurt. His research is on empirical asset pricing and empirical corporate finance. Alexander is an expert on textual analysis and specializes on topics in behavioral finance.

Alexander Hillert (hillert@safe.uni-frankfurt.de) is an assistant professor at the University of Frankfurt. His research is on empirical asset pricing and empirical corporate finance. Alexander is an expert on textual analysis and specializes on topics in behavioral finance.