Following on from our piece on WealthTech – we look at the rise and rise of RegTech (previously known as regulatory technology.) RegTech is a subclass of FinTech, and concerns the use of technology to create efficiencies in financial services for issues regarding regulatory reporting and compliance.

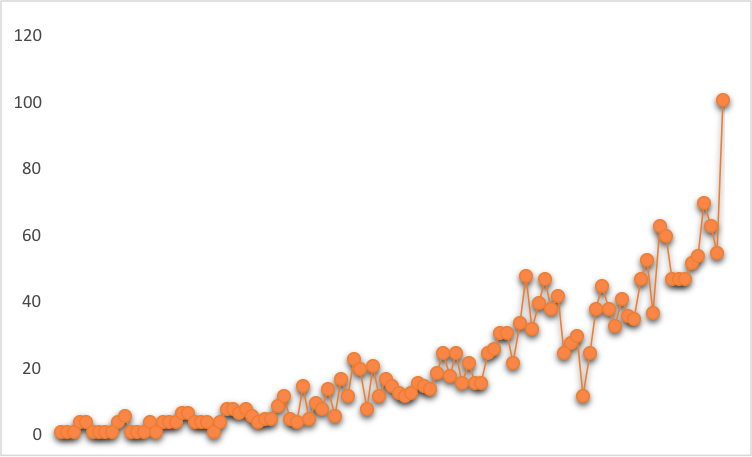

The graph below shows that, if nothing else, the term has exploded in popularity. A look into the data generated on defined FinTech sectors shows the fastest rise in sectoral relevance, and anecdotally our conversations within the FinTech ecosystem show that interest is likely i) to continue and ii) to grow.

Figure 1. Two years of the word ‘RegTech’

RegTech shows the FinTech’s sector’s love of a buzzword, but we ask, ‘is there substance behind the interest?’ We would give an emphatic yes, but possibly best positioned to answer our question is the regulator. In London, the UK regulator, the Financial Conduct Authority, has become known for its propensity to innovate and embrace technology. The FCA has demonstrated its approval of RegTech with Project Innovate and the Innovation Sandbox. The FCA has helpfully defined RegTech for us as the “adoption of new technologies to facilitate the delivery of regulatory requirements.” and has been seen to welcome technology-based solutions. In fact, regulators worldwide have reached out to technology firms and the FinTech ecosystem to improve their processes and stakeholder outcomes through the use of RegTech.

Since the Global Financial Crisis (GFC) the financial services industry has faced a growing volume of regulatory change, as both international and domestic legislators have sought to improve the functioning of the industry and reduce systemic risk. Financial institutions, particularly the banks, have entered a new world of heavy regulations with heavy fines and penalties for non-compliance. Due to this, senior executives and board members have been forced to spend more time in their back offices and spend more on compliance and risk management strategies than ever before, whilst at the same time coping with diminishing revenue streams.

A brief survey of our contacts in both asset management and FinTech show that, at best, regulatory pressure is a constant. The vast majority expect increased regulatory reporting and significantly more compliance-related activities in the next year. No respondent expected a decrease!

MiFiD II being by far the largest concern for Asset Managers. With the directive implemented in January 2018, many smaller asset managers are still struggling with the complexity of its demands. For FinTech institutions, particularly consumer-facing firms, the General Data Protection Regulation (GDPR) is increasing the workload not just of compliance officers but senior management and UX designers.

Due to the ever encroaching regulatory and compliance burden, financial services firms are naturally seeking ways to defray the costs of implementation and monitoring. This environment has naturally created the birth of RegTech, which we are defining as digital processes and tools that leverage technology to improve the compliance process. An ideal RegTech product could provide modular support integrated in day-to-day operations and create not only cost savings and efficiencies, but improve functionality and reduce regulatory risk. Financial institutions who embrace this innovation and seek to re-assess, and preferably automate, current approaches to regulatory compliance, should benefit in the short-term from noticeable cost reduction and in the long term from greater operational stability.

We see the two main social benefits of these developments as better analysis and dialogue between the regulator and the regulated and improvements to business performance due to superior understanding of risk. This process of risk reduction can happen not just at the individual firm level but at a macro-level reducing systemic risk and ideally ensuring financial stability.

The union of regulation and technology to address more complex legislation is in many ways overdue. The advent of MiFID II and similar legislation globally with a much more complex reporting structure is putting a great deal of focus on streamlining processes across financial services. RegTech players will be looking to add value in multiple areas from regulatory reporting to anti-money laundering, payment screening, and Know Your Customer (KYC). Even capital management, traditionally an investment function, has RegTech implications these days.

Interesting firms to watch in the space are Onfido, for global KYC solutions, and FundApps and RiskSave, the company I founded, for asset management compliance technology.

Also by Dan Tammas-Hastings:

‘WealthTech’: The challenges facing the wealth management industry

♣♣♣

Notes:

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: London, by Joe D (Steinsky), under GNU Free Documentation or a CC-BY-SA-3.0 licence

- Before commenting, please read our Comment Policy.

Dan Tammas-Hastings is Managing Director and founder at digital asset management firm RiskSave. He founded the company in response to inadequate risk measures and a lack of transparency dominating the financial services industry. After a successful career as a fixed income trader specialising in GBP derivatives at Merrill Lynch and as a hedge fund manager, managing multi-billion £ portfolios across credit and rates, he is now a leader in risk management and is in charge of strategy and investment at RiskSave. Dan has been awarded both the CFA and FRM charters and is a graduate of the LSE and the University of Cambridge.

Dan Tammas-Hastings is Managing Director and founder at digital asset management firm RiskSave. He founded the company in response to inadequate risk measures and a lack of transparency dominating the financial services industry. After a successful career as a fixed income trader specialising in GBP derivatives at Merrill Lynch and as a hedge fund manager, managing multi-billion £ portfolios across credit and rates, he is now a leader in risk management and is in charge of strategy and investment at RiskSave. Dan has been awarded both the CFA and FRM charters and is a graduate of the LSE and the University of Cambridge.