For over two years we’ve been concerned about the fall in investment rounds to UK businesses. So we are pleased to see this decline abating in our analysis of equity investment activity in the first half of this year, as well as a record level of cash invested.

But, as usual, beneath the surface there are some interesting undercurrents. The fact that later-stage companies are seeing a drop in deals is still a cause for concern.

Another more recent trend is the rise of the international investor, particularly for funding the largest investment rounds. International appetite for backing UK companies, particularly from China and Japan, is stronger than ever. It is difficult to say whether this is because of or despite Brexit. But either way we should pause to question why these companies had to look so far afield for the investment they needed.

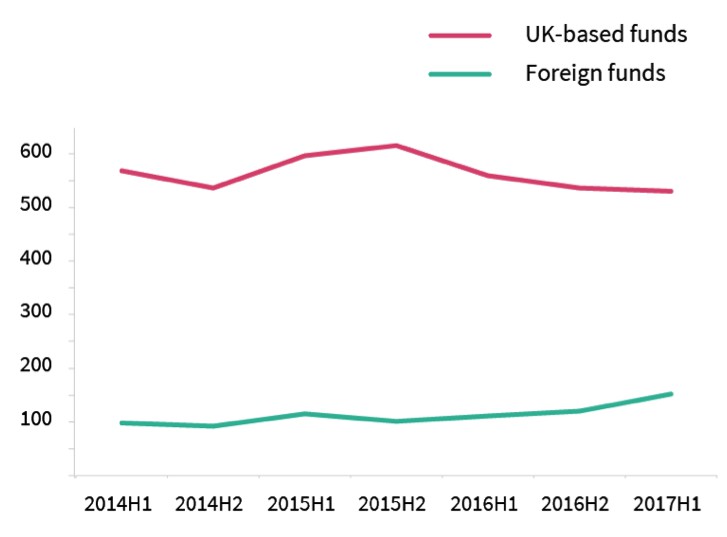

Figure 1. Deal numbers over time: UK-based funds vs foreign funds

Source © Beauhurst (not under a Creative Commons licence)

The graph shows a slow but steady increase of investment from funds headquartered outside of the UK. Are foreign investors dribbling small amounts of capital into high-growth UK firms, or are we instead seeing large swathes of foreign cash feeding UK unicorns, in the absence of sufficient domestic resource?

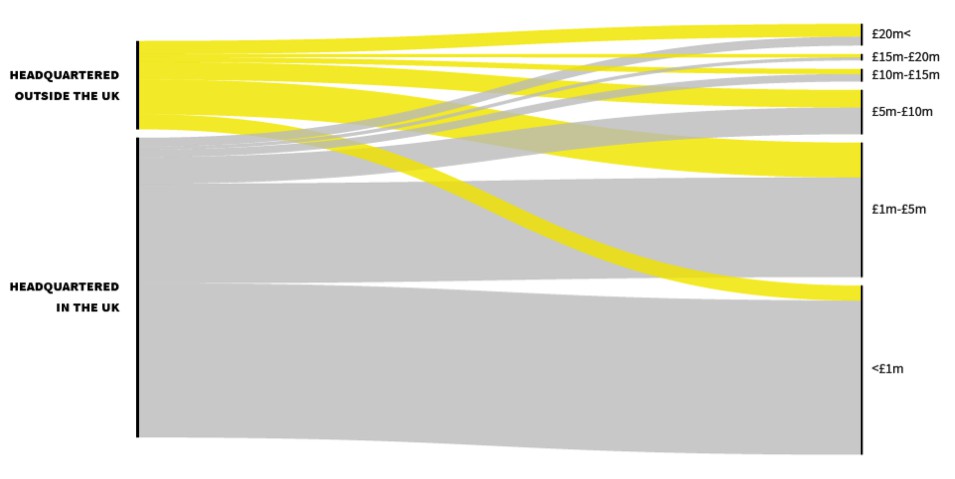

Figure 2. Deal numbers by investment bracket (UK and non-UK headquartered investors, H1 2017)

Source © Beauhurst (not under a Creative Commons licence)

The answer is, broadly, yes to the latter. More deals at the top end of the scale (£20m+) are funded by non-UK investors than by UK funds, which congregate disproportionately at the lower end of the scale (deals between £0-5m).

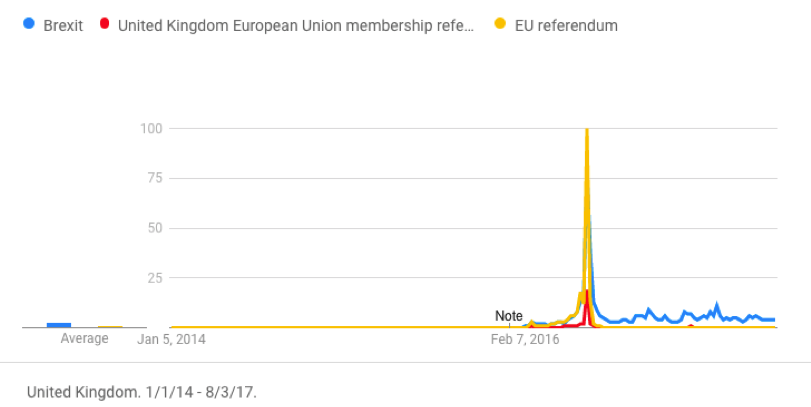

It would be easy (and perhaps natural) to associate this effect with Brexit – either positively or negatively; Brexit could have reduced the capacity/appetite of domestic funds to invest, or it could have made the UK a more attractive place for foreign investors to hold assets. But, as our first graph shows, the increase in foreign investment began in the second half of 2015, at which point Brexit was virtually unheard of:

Figure 3. Interest over time

Source: © Beauhurst (not under a Creative Commons licence) – using Google Trends

This suggests a phenomenon with broader causes than one referendum. Nonetheless, the question of whether the UK’s departure from the EU will affect investment, particularly in rapidly scaling companies, is an important one. Some commentators have queried whether the UK’s unicorn herd will survive in the absence of capital from the European Investment Fund, which invests in many UK funds and as such provides larger pools of cash on which they can draw.

There are nine UK unicorns identified by Beauhurst, and of the 71 funds which backed them, 13 per cent are or have in the past been recipients of EIF funding. The unicorns have raised £1.98 billion between them, of which EIF-backed funds contributed to rounds worth £271.7 million, meaning that EIF-backed funds contributed to 13.7 per cent of the total amount invested in these high-growth companies. This is not an insignificant proportion by any means, though it is not possible to draw firm conclusions from a sample of just nine companies. The relatively small size of the figure may nonetheless provide some reassurance that the future of UK unicorns is not entirely gloomy in the wake of Brexit.

It is not that the cash to create unicorns doesn’t exist in the UK – it’s that asset managers still seem shy of the venture capital asset class. It is our hope that the forthcoming Patient Capital Review, on which we collaborated with HM Treasury, will encourage movement in the right direction.

One of the options put forward by the Patient Capital Review is the establishment of a National Investment Fund, which the Treasury says will help create more British unicorns. If that went ahead, it would be yet another chapter in the periodic anxiety the UK government and banks feel about the long-term capital funding shortfall faced by companies. But is it the best possible solution?

Unicorns require significant – and expensive – nurturing. We looked at our historic (and current) data on any British company that reached unicorn status, and saw that on average they raised over £200 million, across around seven rounds.

New money for growing UK companies is always something to be welcomed, particularly given the current need to compete with extremely well-funded American companies. But, as the government admits, the new fund may end up being sold off to the private sector once it reaches a certain stage. As these anxieties will bubble to the surface every time the economy is going through a rough patch, one can only imagine similar funds would be established in the future – only to be sold off or listed.

A bolder, longer-term idea would be to establish a UK sovereign wealth fund that invested heavily in unlisted companies. The Conservative manifesto promised several infrastructure sovereign wealth funds funded by shale gas and public asset sales. That would be good, but infrastructure investment is not all we need. UK companies need consistent firepower to compete in the world-stage. Firepower that is there when the next economic crisis comes around.

♣♣♣

Notes:

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Searching for the pot of gold at Silicon Roundabout, by Tom de Grunwald, under a CC-BY-NC-SA-2.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy

Pedro Madeira is Head of Research at Beauhurst, overseeing a team tracking investment into high-growth UK companies and monitoring trends around the country. He is an in-demand commentator on equity investment, crowdfunding and the fast-growth landscape. Before joining Beauhurst in 2011, Pedro worked at The Mergermarket Group. He holds a BA and MPhil in Philosophy from King’s College London and the IMC qualification from the CFA Society.

Pedro Madeira is Head of Research at Beauhurst, overseeing a team tracking investment into high-growth UK companies and monitoring trends around the country. He is an in-demand commentator on equity investment, crowdfunding and the fast-growth landscape. Before joining Beauhurst in 2011, Pedro worked at The Mergermarket Group. He holds a BA and MPhil in Philosophy from King’s College London and the IMC qualification from the CFA Society.