Software is eating the world, goes the quip. So rapid are the developments, in fact, that while the “digitalisation of everything” has become a hallmark of tech’s promise of individual and business empowerment so has it begun to prompt anxiety, including among workers who worry about their future in a world of brilliant machines. And yet, for all the evidence that big changes are underway, surprisingly little data exists to quantify the spread of digital adoption across industries and into local workplaces, labor markets, and regions. In the absence of such information, the digitalisation trend, as all-encompassing as it obviously is, remains diffuse and hard to pin down.

Which is why the Brookings Institution’s Metropolitan Policy Program has just released a new report on the progress of “digitalisation”— the diffusion of digital technology into nearly every business, workplace, and pocket in the U.S. Designed to help address the shortage of data on the topic, the new assessment builds on a detailed analysis of changes in the digital content of 545 occupations covering 90 per cent of the US workforce in all industries since 2001. Using that we provide a fresh look at how technology is remaking both the US economy and the world of work. Specifically, by deploying detailed occupation-specific survey information from the Department of Labor’s Occupational Information Network (O*NET) Brookings has been able to create a 100-point tiered rating of hundreds of jobs’ changing computer content that we then use to analyse what the level and change of those scores says about the speed and extent of digitalisation over the last 15 years.

What have we found? Here are five takeaways (followed by a few notes about what it all means):

1. The US economy is digitalising at hyper speed

The first takeaway from the analysis is that between 2002 to 2016 the shares of US jobs and employment that require substantial digital knowledge rose rapidly, whether because of changes in the digital content of existing occupations (the largest effect, by far) or thanks to shifts in the mix of occupations.

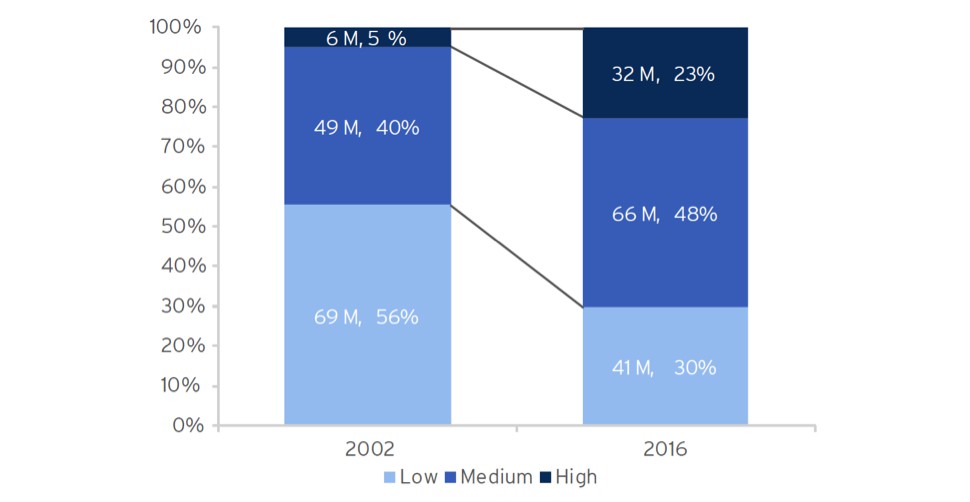

Figure 1. Employment by level of job digitalisation, 2002 and 2016

Source: Brookings analysis of O*NET and OES data

The changes have been striking. Since 2002, the share of all US jobs that require extensive and mid-level digital skills has surged from 45 to 71 per cent of the total. Since 2010, meanwhile, nearly 4 million of the nation’s 13 million new jobs created — 30 per cent of them — have required high-level digital skills.

3. Digitalisation has been ubiquitous but its degree and pace varies widely among occupations and across industries

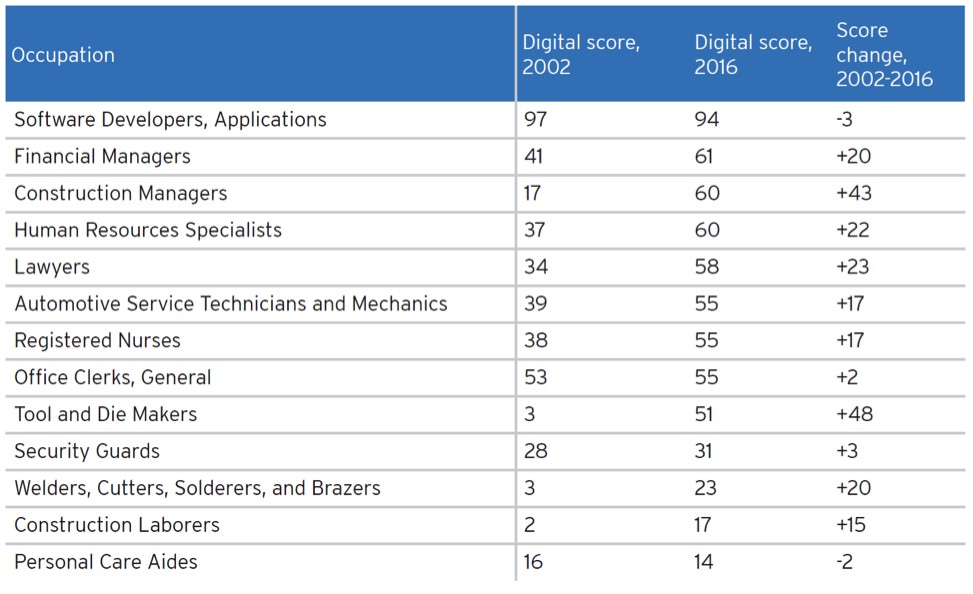

Looking broadly across the job rolls, digitalisation scores rose in 517 of 545 analysed occupations from 2002 to 2016. The average digitalisation score across all occupations rose from 29 in 2002 to 46 in 2016, a 57 per cent increase. Overall, the most significant computerisation occurred around the lower and middle tiers of the scale where the digital scores of many large and accessible occupations underwent radical increases as basic tech was introduced in low-tech industries.

Digital scores rose 50 per cent or more across dozens of mid-digital occupations such as automotive service technicians (39 to 55), registered nurses (38 to 55), and human resources specialists (37 to 60). Likewise, the scores of many lower-score occupations, including home health aides (score rise from 3 to 23), welders (3 to 23), and heavy truck drivers (7 to 30), saw their scores triple or more.

Table 1. Selected occupations by 2016 digital score

Source: Brookings analysis of O*NET and OES data

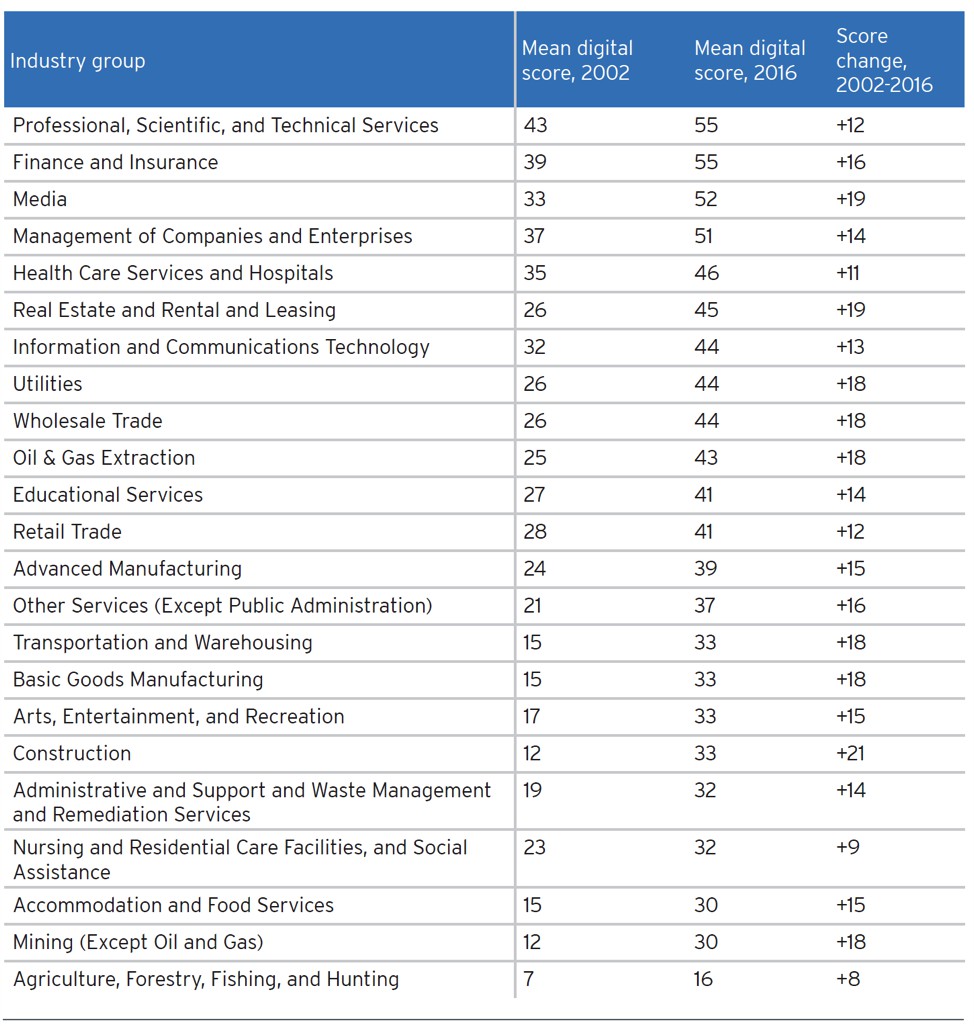

Add these trends up for industries, and it becomes clear that the entire U.S. economy is digitalising rapidly but unevenly. Virtually all industry groups saw their mean digital scores increase between 2002 and 2016, but the level and speed of digital adoption vary significantly, suggesting wide variation in industries’ and firms’ ability to improve their operations, productivity, and results.

Table 2. Industry mean digitalisation scores and change, 2002 and 2016

Source: Brookings analysis of O*NET and OES data

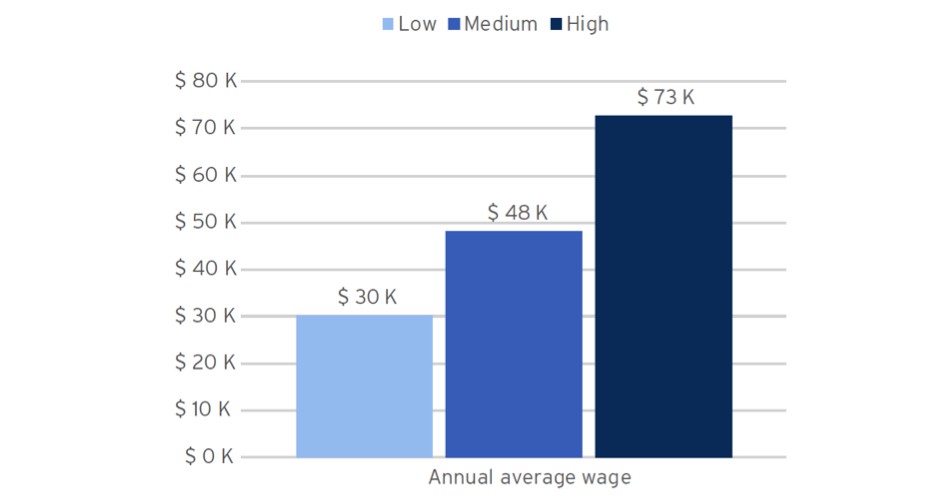

3. Digitalisation, which is a form of automation, is associated with increased pay and job resiliency but also “U-shaped” job creation patterns.

Digitalisation is a key pathway to increased earnings. All across the skills continuum employees are rewarded for the depth and breadth of their digital skills through increased wages. Workers in occupations with medium or high digital skills in 2016 were paid significantly more than those in low-digital occupations.

Figure 2. Mean annual wage by digitalisation level, 2016

Source: Brookings analysis of O*NET and OES data

These pay differentials are important not just in themselves but also because they point to the durability of work in the era of automation. To explore this, we compared occupations’ digital scores to their potential to be superceded, as quantified by the McKinsey Global Institute’s estimates of the share of an occupation’s overall task content that could be done away with by adapting currently demonstrated technology. These comparisons revealed a modestly strong negative correlation between an occupation’s increased digital content and the share of its tasks vulnerable to automation. Digital skills can be a stay against worker displacement.

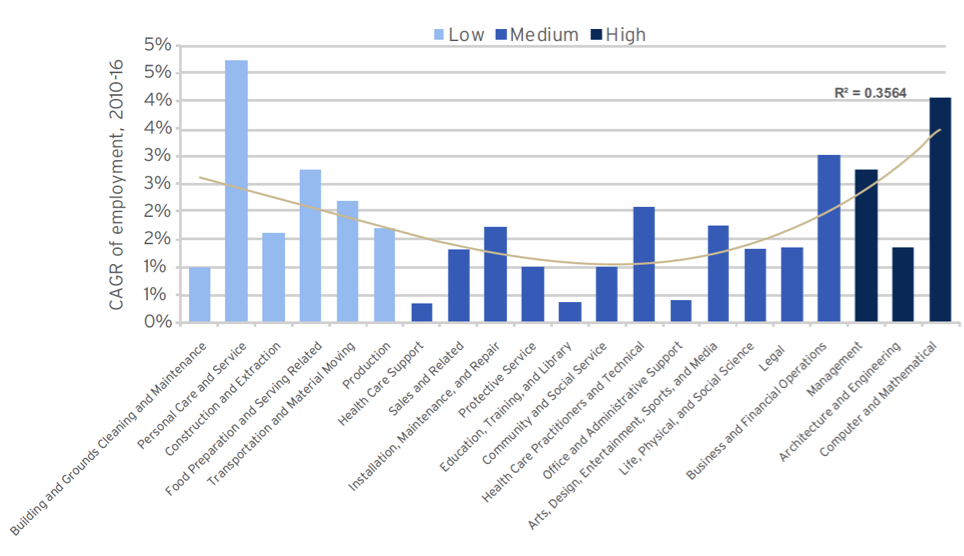

Focusing on patterns of job creation, finally, the digitalisation of the U.S. economy appears to be contributing to the hollowing out and polarisation of employment and wage distributions noted by the MIT economist David Autor and colleagues. These occupational patterns, meanwhile, are also contributing to parallel patterns of industry performance. For the most part, industries’ output, productivity, and wage growth tends to reflect industry-level digitalisation levels. The more digital the industry the better its performance.

Figure 3. Compound annual growth rate of employment by occupation group, 2010-2016. Occupation groups arrayed by 2016 mean digital scores.

Source: Brookings analysis of O*NET and OES data. Note: farming, fishing and forestry occupations are excluded due to small employment size

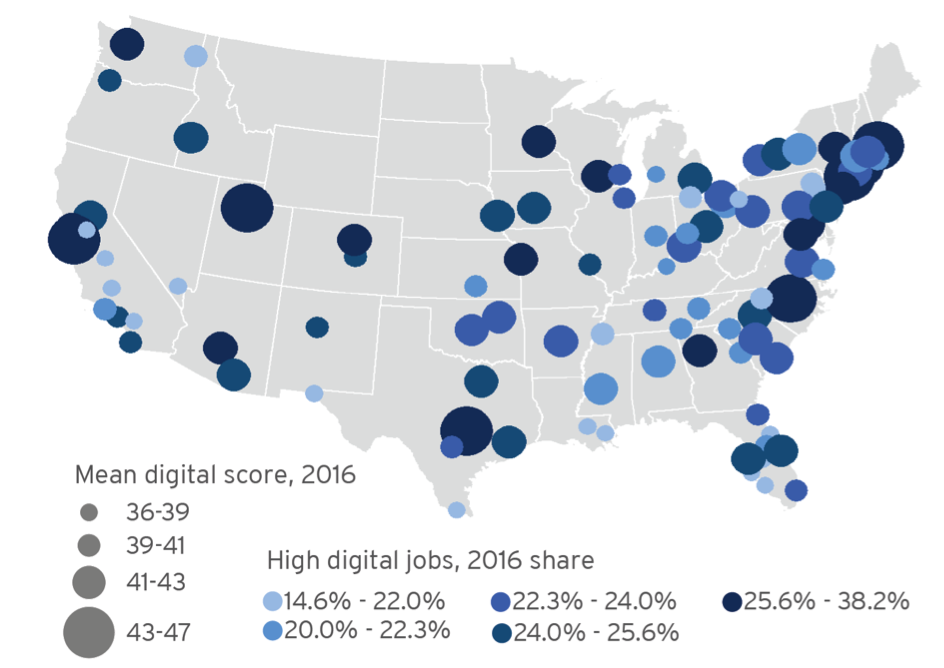

4. The extent of digitalization also varies widely across places and is strongly associated with variations in regional economic performance.

In geographical terms, digitalisation is happening everywhere, but its progress varies widely across the map. Just as the diffusion of digital technology and processes has been uneven across occupations and industries, it is proceeding unevenly across space. (To view the digital status of a state or metro area check out this file).

The data for metropolitan areas, meanwhile, reveals more variation. Large-metro mean digitalisation scores for 2016 range from 47 in San Jose, Calif. to 36 in Las Vegas. Following San Jose at the top of the digitalisation rankings comes a “who’s who” of higher-tech advanced industry centres ranging from Boston; Austin, Texas; Hartford, Conn.; Salt Lake City; Raleigh, N.C.; Seattle; San Francisco; and Madison, Wis.—all with mean 2016 digitalisation scores above 43.

Figure 4. Mean digital score and share of high digital jobs by metropolitan area, 2016

Source: Brookings analysis of O*NET and OES data

In almost all cases, meanwhile, metros saw their mean digitalisation score increase by 12 to 18 points, meaning that for the most part digital laggards among metros were catching up to the digital leaders, allowing for metro digital scores to converge somewhat.

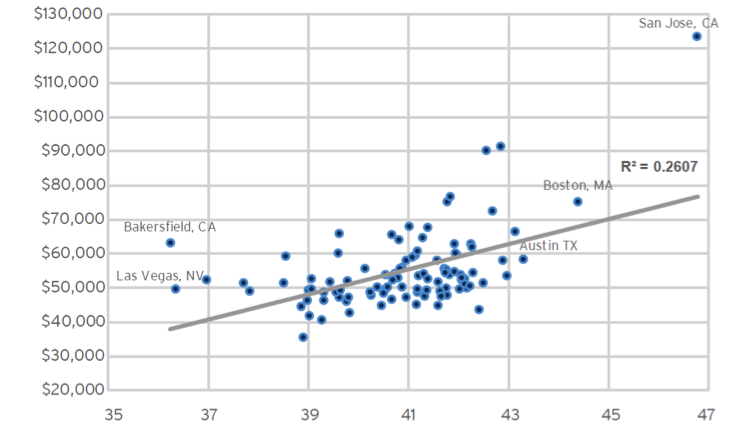

With that said, though, when mapped for their shares of employment in high-digital occupations, metros’ digital skills vary more widely and are diverging. In this regard, the digital rich are getting richer. As to the implications of these variations for regional economies, they follow directly from the strong correlation of digitalisation with worker compensation and industry performance. The more digital a metro the higher its mean annual wage.

Figure 5. Correlation between metros’ mean annual wage and mean digital scores, 2016

Source: Brookings analysis of O*NET, OES and Moody’s data

These trends underscore a key point about the influence of digitalisation on regional prosperity: variations in the digital skills of the local workforce may be contributing to the polarisation of cities’ economic fortunes. Digitalisation, in that vein, appears at once to reflect and reinforce the polarisation of workforce skills across places that is improving pay for many people and places while widening the divide between the leading cities and the laggards.

5. Digitalisation is changing the skills workers need to access economic opportunity while creating new race- and gender-based training challenges.

Digitalisation, finally, is changing the skills less-advantaged workers need to secure good jobs. Given that, the spread of digital tools is underscoring the importance of digital competencies in helping less-educated workers secure basic opportunity even as it throws into relief sharp disparities among particular groups’ digital preparedness.

To see this, look at changes in the nature of what have been called by turns “good jobs” or “middle-skill” jobs — jobs that have the potential to help workers without a four-year college degree earn enough to support themselves and begin to move toward the middle class. That these decent but accessible jobs are digitalising even more rapidly than other jobs suggests that millions of workers could be shut out of decent middle-skill opportunities if they lack the requisite skills.

Table 3. Share of jobs by digital score, 2002 and 2016

Source: Brookings analysis of O*NET and OES data

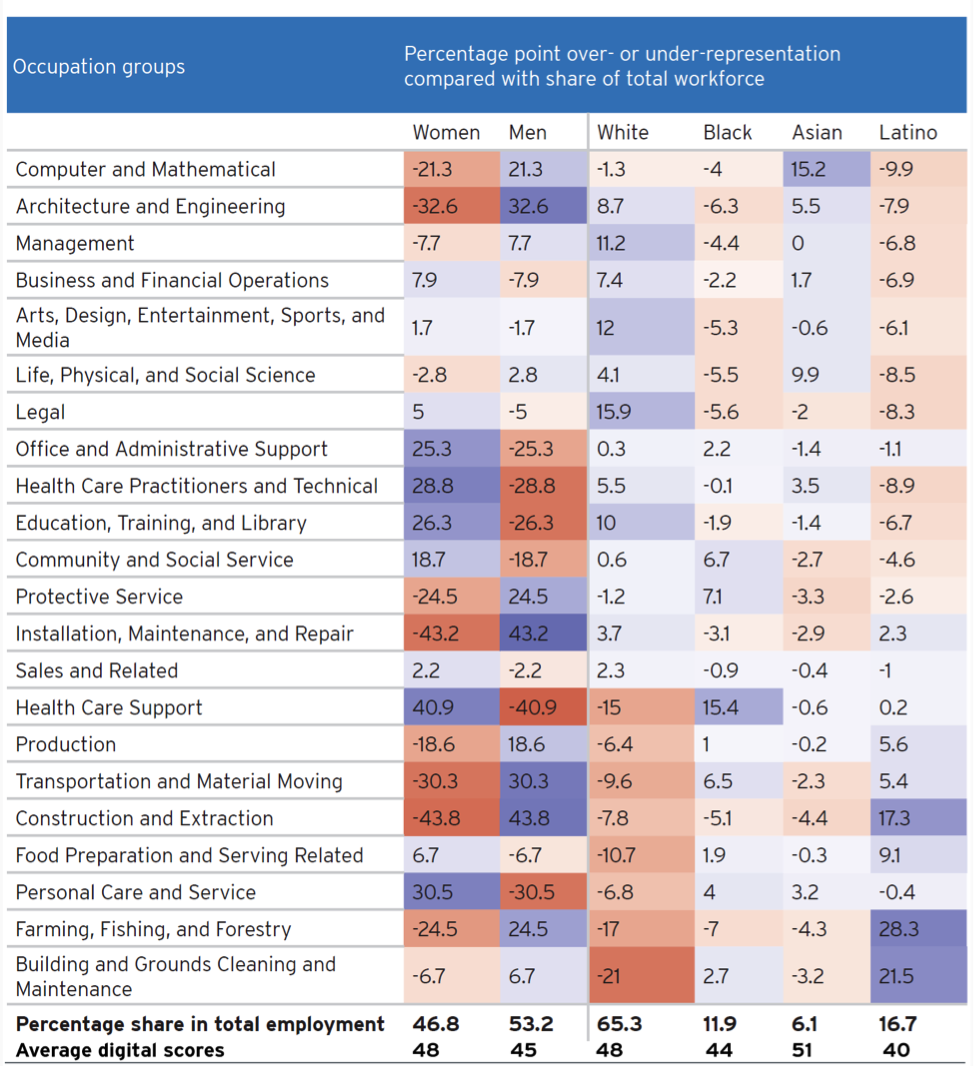

And here is another issue: The mean skills ratings of the jobs occupied by workers in major demographic groups vary in ways that almost certainly contribute to those groups’ uneven access to opportunity. Women, with slightly higher aggregate scores as a group than men, dominate employment in many of the largest medium-digital occupational groups, such as in health professions, but by contrast, remain significantly underrepresented in such highly digital positions as computer and mathematical occupations and engineering. Equally sharp variation characterises the employment profiles of the nation’s racial and ethnic groups.

Table 4. Over- and under-representation of gender and racial groups by occupation group, 2016

Source: Brookings analysis of O*NET and CPS data. Note: Blue and red highlighting represent over- and underrepresentation, respectively, in particular occupational groups.

In this regard, while digitalisation holds out significant opportunities for less-educated or historically marginalised workers or groups to move up the employment ladder, too few of them as yet appear to attaining that progress.

What to do?

Digitalisation, in sum, is transforming the world of work. Workers, firms, and industries as well as entire regional labor markets are all being dramatically affected, with the possibility of new opportunities and the threat of becoming irrelevant. As such, the spread of digitalisation underscores the need for new, widespread, and more creative initiatives to improve workers,’ firms,’ and regions’ access to relevant digital and related “soft” skills. To this end, then, two distinct priorities (and one cross-cutting vision) appear urgent. First, firms, industry associations, educational institutions, and governments must work urgently with workers and students to expand the high-skill IT talent pipeline. And second, governments, businesses, and others need to greatly expand basic digital literacy, especially among underrepresented groups.

To the first priority agenda, the onrushing spread of demand for tech workers in dozens of large “tech-using” industries ranging from health and education to professional services means that cities and businesses will likely experience even sharper demand than they do now for skilled digital workers. They will need to invest urgently in smart competency- and work-based training solutions as well as strengthening the university-level IT talent pipeline. Much more coding will need to be taught, in many more contexts and formats, from online tutorials to accelerated bootcamps to apprenticeships.

To the second end priority, the data here underscore that when it comes to the nation’s broader economic health the larger impact on US prosperity may come from efforts to expose large numbers of less-educated workers to the basics of “everyday” software — spreadsheets and word processing, programs for medical billing and enterprise management. Such efforts are also urgent as even the most accessible decent jobs see their digital content soar. Regions and nations need to make sure this basic degree of entry-level tech skill becomes universal in the next few years.

Otherwise, on both fronts, an effort must be made by education and training programs to cultivate durable human qualities, not just rote skills better done by machines. In this regard, humans — even while learning to work better with computers, whether in the higher-end IT pipeline or in the world of everyday software — need to think much more seriously about what they can do that computers can’t. Computing will soon be virtually everywhere, which prompts jitters, yet that amounts to an incredible opportunity. People will be freed up to give the rote work to the machines and use their uniquely human qualities to solve pressing problems and lead unimagined advances. People of all walks of life should get started with that.

♣♣♣

- This blog post is based on the authors’ Digitalization and the American workforce, a report of the Metro Program at the Brookings Institution, co-authored with Jacob Whiton and Siddharth Kulkarni.

- The post gives the views of the authors, not the position of LSE Business Review or of the London School of Economics and Political Science.

- Featured image credit: Computer city, by ItNeverEnds, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Mark Muro is a senior fellow at the Brookings Institution’s Metropolitan Policy Program and leads its Managing Disruption activities. His work focuses on the advanced technology economy, regional ecosystems, and city variation.

Mark Muro is a senior fellow at the Brookings Institution’s Metropolitan Policy Program and leads its Managing Disruption activities. His work focuses on the advanced technology economy, regional ecosystems, and city variation.

Sifan Liu is a research assistant at the Brookings Institution’s Metropolitan Policy Program. Her research focuses on advanced and inclusive economy activities in cities. Sifan holds a master’s degree in public policy from Georgetown University and a bachelor’s degree in economics from Shanghai Jiao Tong University.

Sifan Liu is a research assistant at the Brookings Institution’s Metropolitan Policy Program. Her research focuses on advanced and inclusive economy activities in cities. Sifan holds a master’s degree in public policy from Georgetown University and a bachelor’s degree in economics from Shanghai Jiao Tong University.